The Philosopher-Investor: Josh Tarasoff & The Self-Driving Way

On Endgames, Quality with a Capital Q, and an Investor Who Bought Amazon in 2011

"Duration — the force multiplier of all that compounds — is underrated."

In today’s edition:

🕴️ The Guru: Josh Tarasoff — Founder of Greenlea Lane Capital

📈 The Playbook: The Greenlea Lane Way — Permanence, Quality and the Indirect Path

💎 The Gems: A Tour of Greenlea Lane’s top holdings

🔄 The Confirmation: Why Tarasoff’s portfolio validates several of our existing positions

Today’s Guru deep-dive is a bit longer, so here is a 2-minute AI audio version if you are short on time (bonus point if you can find the error)

Start here if you are new to Guru Gems.

Welcome to Year 2 of Guru Gems

Last week I published newsletter #52, the one-year anniversary edition of Guru Gems

In the ‘What’s Next for Year 2?’ section I wrote:

“In my first year I have covered mostly well-known names, so going forward I will try to also cover some lesser-known Gurus.”

Well here I am, making good on that promise already :)

Josh Tarasoff is probably one of the lesser-known investors I have covered until now, but a very interesting Guru nonetheless. He has no public profile, no media presence, and no marketing operation of any kind. He runs a fund of just 8-10 stocks out of his home in Connecticut, entirely on his own.

There isn’t much available in terms of interviews or investor letters, especially from the past couple of years, but after some research I still managed to find a few very interesting interviews and materials published on his website that allow me to understand his investment framework.

Let’s dig in.

Guru in the spotlight: Josh Tarasoff

Josh Tarasoff is not a household name. He does not appear on CNBC or Bloomberg TV, does not publish on X (at least not anymore), and has never run a marketing campaign. He operates out of Weston, Connecticut, with no employees, no formal office, and no analyst team.

He launched Greenlea Lane Capital in 2006 with about $2 million raised from himself, friends and family and has compounded at 17.3% net of all fees from inception through 2021 (this is based on an interview from 2021, I couldn’t find any more recent performance data)

Tarasoff is a Duke University philosophy graduate (2001), had an earlier career at Goldman Sachs and later attended Columbia Business School.

He started Greenlea Lane immediately after graduating from Columbia, moving into a cheap place with friends, working out of his bedroom, investing his own capital plus a small sum from his network.

The fund's first real test arrived almost immediately. In 2008, Greenlea Lane was down 51%, something Tarasoff had prepared himself to accept before he ever launched. Rather than retreating, he used the crisis to buy quality businesses when they finally got cheap.

It was also when he crystallised what he actually wanted: not mature businesses bought at a discount and sold at fair value, but genuine compounders, companies growing intrinsic value at 15–20% or more that you could simply hold. By 2012 this conviction led him to Amazon, a stock he has now held for 14 years, made it nearly a 25-bagger, and which is still his largest position today.

If you enjoy this newsletter, please help others discover it by clicking 🤍

And if you learned something useful, consider buying me a virtual coffee ☕

The Greenlea Lane Way

Tarasoff is an unusual figure in money management because he is not just a practitioner, he is also a great thinker.

Over the past five years he has published four essays that form the basis of his intellectual framework. I highly recommend reading these for everyone serious about investing.

Here are the four ideas that define how Tarasoff invests.

1. 🚗 The Self-Driving Portfolio

The most distinctive concept in Tarasoff’s framework is what he calls the “self-driving portfolio.”

Most investment firms operate under implicit time pressure: a portfolio of two dozen stocks with a two-year average holding period requires one new market-beating idea every single month, without end.

The necessity to be continuously on the verge of some great new idea sows an endemic hurriedness that can be seen on people’s faces and heard in their voices. This struck me as unhealthy for decision making (and perhaps even unhealthy, period).

His solution is radical in its simplicity: approach every investment with a permanent attitude. Not a five-year time horizon. Not a long-term view. A permanent view: the expectation that the company will compound itself indefinitely.

“I call this approach self-driving because — though it might not be achievable in practice — the ideal is for the portfolio to take over all the work.”

The benefits compound on themselves: less time pressure leads to better decisions, which strengthens the portfolio, which further reduces time pressure. Most importantly, it enables him to be calm and ready to act when exceptional opportunities arise.

A self-driving portfolio is antifragile by design, and Tarasoff notes that it is probably also more sustainable over a long career than investing under constant pressure.

This connects directly to what I wrote about Chris Hohn: that long-termism in a great company is a free lunch. Tarasoff would no doubt 100% agree with Hohn’s statement, as Tarasoff sees long-termism as “a way of being”.

2. 🔁 Feedback Loops & The Endgame

These two concepts come from the same 2021 essay and belong together. They are both about understanding a company’s long-term system rather than its near-term events.

On feedback loops: Tarasoff believes sustainable long-term growth is impossible without them. Growth that is not self-reinforcing is, by definition, fragile. He looks for loops everywhere, not just in the classical categories like network effects.

The deeper implication is that feedback loops guide you toward dynamics rather than events. A price cut may be scale economies shared at work, not competitive pressure. Rising expenses may reflect investment in a loop, not deteriorating fundamentals.

On endgames: An endgame is a long-term state of affairs, typically 10+ years out, grounded in what Tarasoff calls overwhelming logic: forces that make too much sense not to prevail in the fullness of time.

The key insight is that while the path to the endgame is almost always unpredictable, the destination can be foreseen because feedback loops and quality will eventually play out.

“Long-term investing means letting go of the path’s false comfort and embracing deeper currents.”

One of his favourite situations is when a company’s best decade won’t even begin for five years or more: the endgame is clear, but there is near-term murkiness as the pieces fall into place. Most investors focus on the noise. Tarasoff waits for the endgame.

3. ✨ Quality, Conviction & The Implicit

This idea is developed across his 2024 and 2026 essays. It starts with a distinction between two kinds of conviction.

Explicit conviction can be written down and modelled in Excel: forecasts, margins, intrinsic value ranges.

Implicit conviction is different: it is felt rather than calculated. It is the deep qualitative knowing that a company will do what it needs to and ought to do, even when the numbers are temporarily disappointing.

Both are necessary, but the investment industry systematically underweights the implicit, because it cannot be transmitted from analyst to portfolio manager to client, and cannot be turned into a “repeatable process”. That gap is precisely where the opportunity lies.

The deeper-something that underlies implicit conviction, Tarasoff calls ‘Quality’, in homage to the philosopher Robert Pirsig. A company with Quality has a soul. It is mission-driven. It thinks holistically in time horizons long enough that any distinction between mission and value creation dissolves.

“Some companies have a soul, and others are just going through the motions.”

In his February 2026 essay he argues that AI and technology make more investors increasingly reliant on quantification, and that the ability to perceive what cannot be measured will become rarer and more valuable, not less.

“To the extent that market participants become increasingly immersed in and reliant upon technology, it is possible that the capacity to incorporate what lies beyond the reach of technology will become even rarer and more valuable.”

4. 🌳 The Indirect Path

Tarasoff’s July 2024 essay, “Direct and Indirect,” starts with a simple distinction: some activities are simple and can be approached directly (assembling a Lego set: just follow the instructions). Others are complex, and their outcomes cannot be aimed at directly. Growing a tree is the example: you cannot coax a seed to germinate or pull on a sapling’s branches. You plant it in fertile soil, ensure water and sunlight, and let it grow itself.

Investing is a complex activity. The appropriate approach is therefore indirect.

For Tarasoff, this means starting from a foundation of studying companies and industries he finds genuinely interesting, something pursued for its own sake, as a default mode.

“Occasionally investment conviction falls into place, which feels as much like good fortune as the fruit of hard work.”

The same principle applies to how he thinks about the future. Rather than building forecasts and working backward to a price target (which is the industry’s standard direct approach) he concentrates on the past and present of companies until a strong view of the future comes into focus.

This emphasizing of ‘Potential over prediction’ as he calls it, is the indirect approach applied to investment thesis-building.

The Greenlea Lane Portfolio

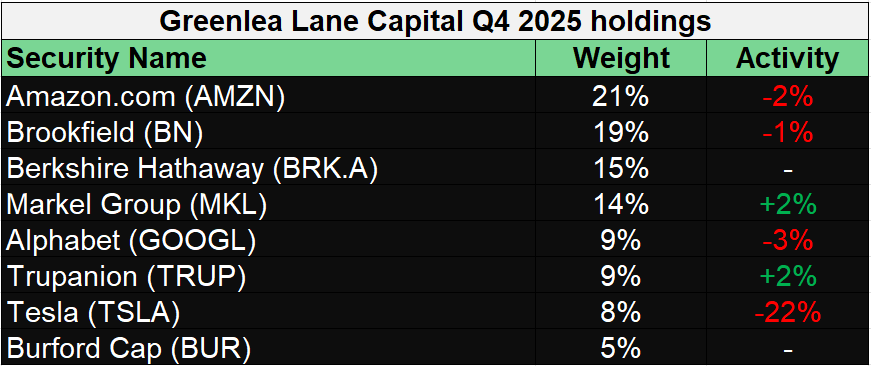

Here is Josh Tarasoff's portfolio at end of Q4 2025. Just 8 positions, $343 million in US equities holdings:

Eight stocks. That’s it. The top 4 positions alone represent nearly 70% of all assets. This is a level of concentration similar to Bryan Lawrence or Dev Kantesaria.

This level of simplicity also echoes what I admire most about François Rochon: both men have structured their professional lives to think clearly, over the longest possible horizon, free from the business pressures that corrupt so much of the industry. The difference is that Rochon runs 20-30 positions; Tarasoff runs 8. Same philosophy, taken one step further.

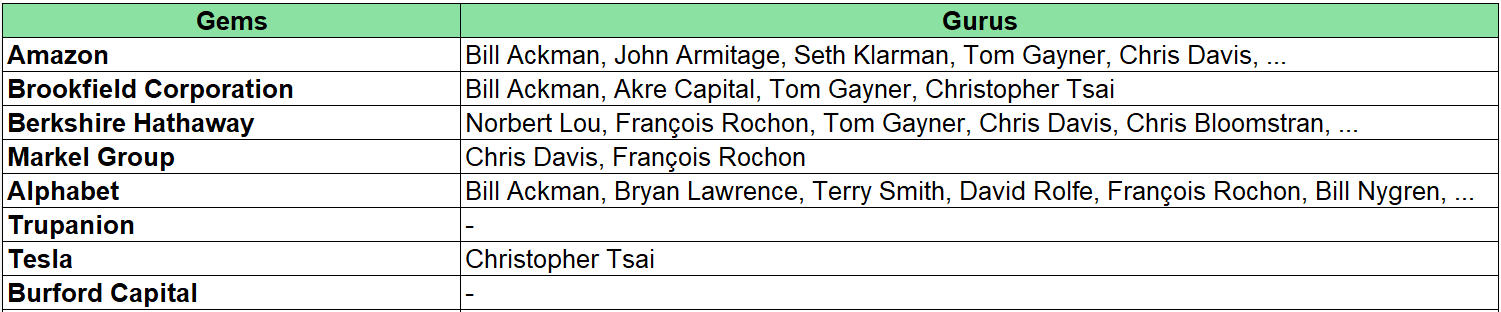

What strikes me immediately when looking at this portfolio is how many of these names I have already encountered on my Guru Gems journey.

Let’s take a closer look.

💎 The Gems: A Tour of Greenlea Lane’s Top Holdings

Rather than deep-diving a single name (as I normally do), given that Tarasoff’s largest Gem Amazon has already featured before, I want to walk briefly through each of Tarasoff's positions using the lens of his own framework.

🥇 #1: Amazon (21%)

Amazon is a core holding of Bill Ackman, John Armitage, Seth Klarman and quite a few other Gurus. I added it to the Guru Gems portfolio about a month ago, and with the stock already up 22% since then, that seems to have been a good decision.

Seeing it as Tarasoff’s #1 position at 21% of a fund he has managed since 2006 is a powerful confirmation.

In June 2012, Tarasoff pitched Amazon at VALUEx Vail when the shares were trading at approximately $11 (split adjusted). His verdict at the time:

“AMZN is the finest business of which I am aware, and I believe it is (very) cheap.”

In his pitch, he laid out five structural advantages: cost structure, selection, convenience, personalization, and habit formation, and showed that each one compounds further with scale. He called them “advantages that widen every single day.”

Here is his pitch, it’s really cool to see his thinking process and how he was already thinking about the next decade for Amazon:

Amazon today trades at around $250. From the split-adjusted 2011 entry, that is roughly 23 times his money in 14 years.

His decision to hold through every bit of market skepticism about Amazon’s margins is itself the self-driving portfolio in action, a textbook illustration of feedback loops, endgame thinking, and Quality all converging in a single position.

🥈 #2: Brookfield Corporation (19%)

Brookfield Corporation, an alternative asset management powerhouse, is another Gem held by many Gurus: Bill Ackman, Akre Capital, Tom Gayner.

Brookfield is almost certainly the unnamed company in Tarasoff’s “Direct and Indirect” essay:

“Whereas its peers started life knocking on doors to raise capital for dealmaking (direct), what might be surprising is that this company existed for decades before hanging out its shingle as an asset manager (indirect). During that period, it was solely a principal investor whose goal was to compound its capital at attractive rates with a generational time horizon.”

Beginning as a Brazilian utility in the 19th century and evolving into a global owner-operator of real assets, Brookfield built its competitive position over generations. This is the indirect path Tarasoff talks about: the $1 trillion AUM franchise was never engineered from day one; it emerged from decades of mastery.

🥉 #3: Berkshire Hathaway (15%) & #4: Markel (14%)

Berkshire Hathaway and Markel I covered previously. Tarasoff holding both at a combined 29% of his portfolio is consistent with the principles he writes about: Quality culture, long time horizons, and compounding capital through ownership.

“Reading Buffett was a moment of clarity, and I knew value investing was what I wanted to do.”

#5: Alphabet (9%)

As regular readers know by now, Alphabet is the ultimate Guru Gem and it’s great to see Tarasoff holding it as well.

#6: Trupanion (8%)

Trupanion is a pet insurer provider and seems a bit of an unusual name in the portfolio. But as Tarasoff explained in a 2017 interview, it is his clearest public example of "certain change": a situation where a new way of doing something is a genuine win-win with no losers.

As he put it in 2017: if a pet owner can't afford $5,000 to save their pet's life but can pay $40 a month in insurance, then the pet benefits, the owner benefits, and the veterinarian gets to perform the highest-level procedure.

"There's literally no loser in pet medical insurance."

It is also almost certainly the unnamed pet insurer from his "Direct and Indirect" essay, with a veterinary distribution model that is nearly impossible to replicate.

#7: Tesla (8%)

Tesla is the position that will raise the most eyebrows. It was ~10% of the portfolio in Q3 2025 before being trimmed. Tarasoff has not written publicly about why he holds it, so any explanation is just me guessing.

Through his own framework, one could see it as a company with strong positive feedback loops in its technology and manufacturing, a founder with unlimited ambition, and a long-term endgame.

Tesla's endgame, articulated in their Master Plan Part 4, is achieving "sustainable abundance" through AI, robotics, and energy dominance.

I also see parallels with Christopher Tsai, an investor I covered before who has Tesla as his largest position, but also holds significant positions in Brookfield, Amazon, Markel and Berkshire.

#8: Burford Capital (5%)

Burford Capital is equally unusual. Burford is a leading litigation finance company, providing capital to plaintiffs or law firms in exchange for a share of legal proceeds.

Again, Tarasoff has not publicly commented on this position, but its inclusion is consistent with his endgame framework: a genuinely differentiated business model in a market still in its early innings, with a long-duration return profile and high barriers to replication at scale.

🔄 The Confirmation: What Tarasoff's Portfolio Tells Us

One of the most valuable exercises when studying a new Guru is to check how their portfolio overlaps with previous Gurus I have studied, and with the Guru Gems portfolio itself.

The convergence across Gurus is striking. Amazon, Brookfield, Berkshire, Markel and Alphabet show up across multiple portfolios of investors with entirely different styles and processes. That kind of multi-Guru overlap remains one of the strongest signals this newsletter tracks.

Final Thought: The Philisopher-Investor

Most people in money management see investing as a profession with defined best practices. Tarasoff sees it as something closer to an art: something that must be cultivated from within, tailored to your unique personality and interests, and pursued for its own sake rather than for the validation of others.

His north star has always been the same: to be the best investor he can be, in his own way, for partners who want exactly that from him.

I really enjoyed the research for this deep-dive as so much of it resonates with how I think about investing.

“I came to think of true long termism as a way of being.”

— Josh Tarasoff

That’s it for this week’s edition!

Thank you for reading and following along.

Until next week!

A manager who truly embodies the fact that investing really is an “infinite game” where spirit and vision can often outdo precision

Great profile. Josh Tarasoff is exactly the type of public equity manager I’m most drawn to where the portfolio is a unique work of art for the investor.