Timeless Lessons from François Rochon

On HEICO, LVMH, Alphabet & The Art of Patience

It is better to be roughly right than precisely wrong

In today’s edition:

🕴️ The Guru: François Rochon

📈 The Playbook: The Giverny Way - 32 years of compounding with patience, humility and rationality

💎 The Gem: HEICO Corporation (NYSE: HEI.A) — The Quiet Aerospace Compounder

🔄 BONUS: The Full Circle: LVMH — How a 14-year mistake finally became a position

2-minute AI version:

Start here if you are new to Guru Gems.

A word on Guru Gems Edition #50

Fifty weeks ago, I published the first Guru Gems newsletter

The idea was simple: study the world’s best long-term investors, understand how they think, find the high-quality companies hiding in their portfolios, and build a real-money portfolio based on their collective wisdom.

One year later, I have covered more than a dozen of the world’s greatest investors — from Terry Smith to Chuck Akre, Chris Hohn to Bill Ackman, Dev Kantesaria to Bryan Lawrence and I have added twelve positions to the Guru Gems portfolio.

For this fiftieth edition, I wanted to dedicate the newsletter to an investor who embodies everything Guru Gems stands for.

A man who has been running the same portfolio, guided by the same principles, for over 32 years. A man who awards himself annual medals for his biggest mistakes. A man who writes to his partners the way he would want to be written to if their roles were reversed.

This is François Rochon. And this is his story.

Guru in the spotlight: François Rochon

François Rochon is the founder and president of Giverny Capital, a Montreal-based investment firm he launched in 1998 after managing his family portfolio for five years.

He is an engineer by training and a self-taught investor who discovered the writings of Warren Buffett, Benjamin Graham, John Templeton, Philip Fisher, and Peter Lynch in the early 1990s and never looked back.

Since July 1, 1993, the Rochon Global Portfolio has compounded at 14.7% annually, versus 9.9% for its benchmark — an annualized outperformance of 4.8% over 32 years. In practical terms, $100,000 invested with Rochon in 1993 would be worth approximately $8.7 million today. The benchmark produced $2.2 million over the same period.

What makes this record remarkable is not just the magnitude, but how it was built. There were no black box strategies and no leverage. Just a portfolio of exceptional businesses, owned patiently and with conviction, managed by someone who treats every partner as he would want to be treated if their roles were reversed.

Rochon’s annual letters (all publicly available at givernycapital.com ) are masterclasses in long-term thinking, intellectual honesty and the art of learning from mistakes. They are essential reading for any serious investor.

“Our goal is to explain in detail the long-term investment philosophy behind the selection process for the companies in our portfolio. Our wish is for our partners to fully understand the nature of our investment process since long-term portfolio returns are the fruits of this philosophy. Over the short term, the stock market is irrational and unpredictable (though some may think otherwise). Over the long term, however, the market adequately reflects the intrinsic value of companies. If the stock selection process is sound and rational, investment returns will eventually follow.”

In a recent post, I shared my favorite investor letters, and it’s probably not surprising that François Rochon was my #1 pick.

If you enjoy this newsletter, please help others discover it by clicking 🤍

And if you learned something useful, consider buying me a virtual coffee ☕

The Giverny Way

There are many good interviews available with François Rochon, but I believe the best way to learn and study Rochon is to read all his annual letters, and so that is what I did.

Here are the 5 pillars that define how Rochon invests.

1. 🤝 The Alignment Principle

From the very first days of Giverny, Rochon established one non-negotiable rule: he invests his own money in exactly the same securities as his clients.

The Rochon Global Portfolio — his personal family portfolio — serves as the direct model for all client accounts.

“I buy for you what I buy for myself. This doesn’t guarantee results, but it does ensure our interests are aligned.”

He calls his clients “partners” for precisely this reason. When the portfolio does poorly — as it did in 2025, with a 2.7% return against a 13.7% benchmark — Rochon does not hide. He writes “Explanations, Not Excuses” at the top of the relevant section and dissects every mistake in detail.

This level of transparency is quite rare in the fund management industry.

2. 🏰 The Moat Framework

Rochon does not use the word “moat” as frequently as some investors, but his stock selection criteria point to exactly the same thing.

He calls the businesses he likes “self-determined” companies: companies that control their own destiny because of durable competitive advantages. You can read more on this in his 2022 Annual Letter.

In every annual letter, Rochon shares his investment philosophy in an Appendix, aimed for new ‘partners’, and his criteria have not changed:

High and sustainable margins and high returns on equity

Good long-term prospects

Managed by brilliant, honest, dedicated and altruistic people

Avoid: non-profitable businesses, excessive debt, high cyclicality, ego-driven management

“There can be quite some time before the market recognizes the true value of our companies. But if we’re right on the business, we will eventually be right on the stock.”

3. 📊 The True Scorecard: Owner’s Earnings

Since 1996, Rochon has published a chart showing the growth in the intrinsic value of his portfolio companies.

He arrives at an estimate of the increase in intrinsic value of the companies by adding the growth in earnings per share (EPS) and the average dividend yield of the portfolio. He calls this “owner’s earnings”, borrowed from Buffett.

The lesson from 30 years of data is striking: over the long run, the stock market return of his portfolio has tracked the underlying intrinsic value growth almost perfectly.

“The stock market is irrational in the short term. Over the long term, it always ends up reflecting the intrinsic value of companies.”

In 2025, his companies grew their intrinsic value by approximately 13%, while the stock portfolio returned only 2.7% (7% without currency effects). He takes this calmly. He has seen it many times before. He knows the eventual convergence is inevitable.

4. 🏆 Intellectual Honesty: The Podium of Errors

Perhaps the most distinctive element of the Giverny tradition is the annual ‘Podium of Errors’ (‘Mistake du jour’ in his earlier letters), where Rochon awards Bronze, Silver and Gold medals to his biggest investment mistakes of the year or recent past.

“It is with a constructive attitude, to always improve as investors, that we provide this detailed analysis.”

What’s particularly instructive is how often the Medal goes not to a bad investment that cost money, but to a great investment never made. A company he studied, admired, and then failed to buy.

Netflix (2025 Silver), O’Reilly Auto Parts (2022 Silver), Copart (2019 Gold), Amazon (2015 Bronze), Google (2010 Silver)

Errors from omission (non-purchases), according to Rochon, are often more costly than errors from commission (purchase).

What’s really interesting to see is that when Mr. Market offers him an opportunity to buy these companies at depressed prices, Rochon will not hesitate.

Google (2010 Silver medal) is a great example of this. Rochon knew it was a fantastic business but he was waiting for a good entry price.

In 2011, the opportunity came and Rochon bought Google at a PE of ~15x when Wall Street was worried that Google would not be able to dominate in mobile as they did on desktop. Today, 15 years later, it is one of his largest positions.

LVMH (2022 Gold) is another great example, and I will cover this later in more detail.

5. 🎲 The Three Essential Qualities

In his 2025 annual letter and his recent interview on We Study Billionaires, Rochon named the three qualities he believes are essential for long-term investing success.

Rationality. The ability to look at reality as it is, not as you wish it to be. To leave emotion aside and focus on facts. In a market dominated by hope and fear, this gives a quiet but decisive advantage.

Humility. The recognition that mistakes are inevitable, and that improvement requires the willingness to admit them. His ‘Rule of 3’ is a brilliant example of this:

“One year out of three, the market will go down (by more than 10%). On stock out of three that we will buy will be somewhat disappointing. And one year out of three, we will under perform the indexes.”

Patience. Perhaps the rarest quality of all. In the interview, Rochon recalled asking Philip Carret — who invested for 75 years and died at 101 — what his greatest lesson was. Carret thought about it, then said: “Patience.”

This connects really well with what I learned from Chris Hohn, another investing master, who said that “long-termism in a great company is a free lunch”

The Giverny Capital Portfolio

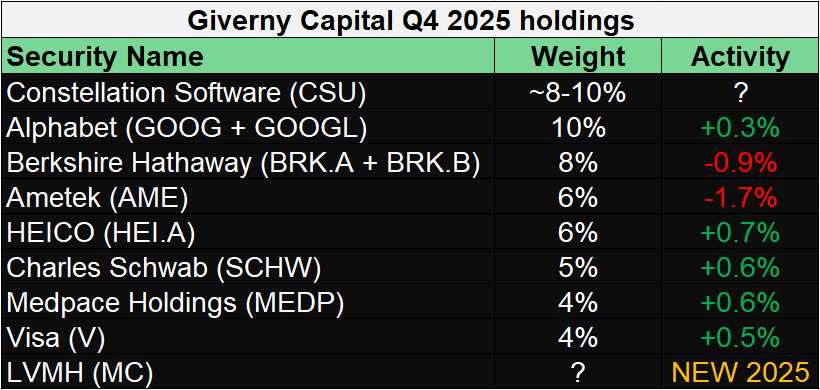

Here is Giverny Capital’s stock portfolio at the end of Q4 2025:

Note that for non-US positions (Constellation Software, LVMH), these are estimates as they are not reported in 13F filings.

3 companies worth highlighting from this $3+ billion portfolio:

Constellation Software: His largest holding at the beginning of 2025 has fallen significantly due to AI-related fears and the CEO's health-related departure. Despite a 26% decline in its stock price during 2025, Rochon notes in his 2025 letter that the business itself remains strong, having grown its earnings per share (EPS) at an annualized rate of 20% since his first purchase

Alphabet - As discussed in the previous section, Rochon has held Alphabet for about 15 years. He says the idea to invest in Google came thanks to Charlie Munger

“Mr. Munger explained at a conference that many companies that historically had wide competitive moats had seen their moats "filled up with sand" (an analogy meaning that their competitive advantage was deteriorating). I then asked him if he saw new companies with a wide moat and, after reflection, he replied Google. His comments did not fall on deaf ears and Jean-Philippe and I started looking at the company from a whole new perspective.”

HEICO: Our Gem for this edition has been in Rochon’s portfolio for nearly 10 years and has climbed to become a top-5 position.

💎 The Gem: HEICO Corporation (HEI/HEI.A)

“The difficulty in obtaining approval from the Federal Aviation Administration (FAA) for these aircraft parts, along with extensive catalog of parts available from the company that was built over several years, provide a very significant competitive advantage for Heico.”

— François Rochon, 2016 Annual Letter (the first time he introduced HEICO to his partners)

How Rochon Found HEICO

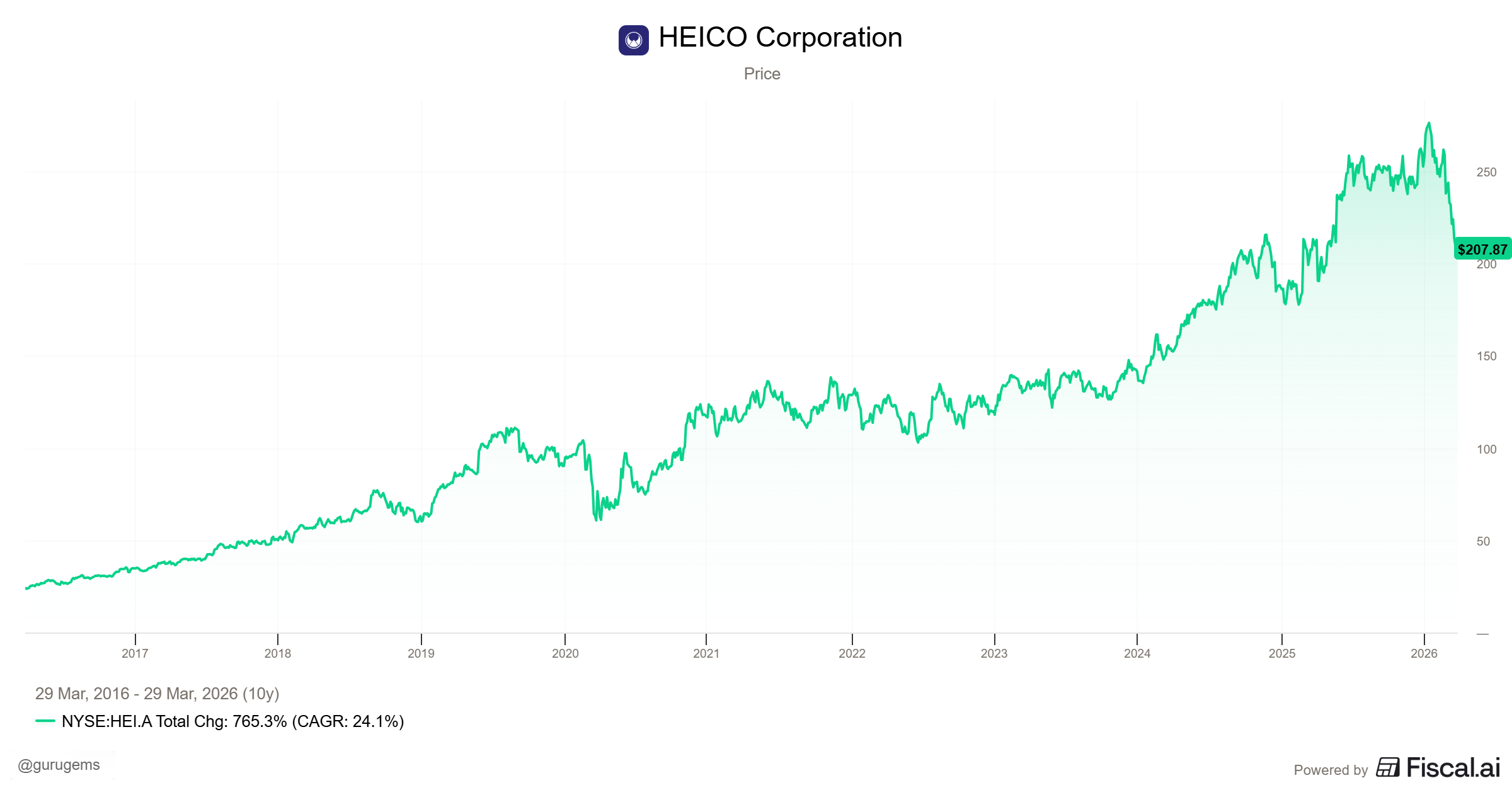

Rochon first acquired shares in HEICO in 2016, introducing the company in that year’s annual letter with characteristic brevity and precision. In just a few sentences, he identified the essence of the business: FAA-approved aftermarket parts, a multi-year catalog built over decades, and a moat created by regulatory complexity.

At the time, HEICO’s Class A shares traded at approximately $23 (adjusted for stock splits). EPS had grown at roughly 19% annually over the preceding decade — a figure Rochon described as “an exceptional performance.” By his 2021 annual letter, the stock had risen more than 200% from that first purchase, and he noted continued admiration for the Mendelson family who run the company.

Today, those same Class A shares trade at ~$208, a 800%+ gain from Rochon’s initial purchase price. HEICO remains a top-5 position in the Giverny portfolio, a core holding of ten years’ standing.

To Buy or Not to Buy

Let’s evaluate HEICO through our Terry Smith inspired framework to decide if I should add it to the Guru Gems portfolio.

1/ Buy good companies

What Does HEICO Do?

HEICO is a Florida-based aerospace and defence company with two main segments.

The Flight Support Group manufactures nearly 20,000 different FAA-approved aftermarket replacement parts for commercial and military aircraft, selling them at a 30-50% discount to the original equipment manufacturer (OEM) equivalents.

Source: HEICO website The Electronic Technologies Group provides specialized electronic systems and products for defense, space and industrial applications.

Source: HEICO website

HEICO is like the generic drug equivalent for aircraft maintenance. Airlines face enormous pressure to cut costs. Aircraft parts are one of their largest expenses. But safety cannot be compromised, every part must meet strict FAA airworthiness standards.

HEICO worked out decades ago that if you invest the time and money to get your parts FAA-certified, you can offer airlines a cheaper alternative that is just as safe and legally compliant. Airlines save money and HEICO earns exceptional returns.

How the Moat Was Built

The origin of HEICO’s dominance is a story of extraordinary persistence. When the Mendelsons took control in 1990, the company had $25 million in sales and was losing money. Eric Mendelson — 24 years old — practically lived in the FAA’s Washington DC headquarters, learning the certification process from the inside out. By 1991, they had their second approved part: a tube used in jet engines.

A pivotal moment came in 1997, when HEICO convinced the chairman of Lufthansa Airlines to invest a 20% stake in the PMA business. Lufthansa gave HEICO direct insight into which parts airlines most urgently needed, provided immediate credibility with other carriers who were still hesitant to buy from non-OEM suppliers, and guaranteed a buyer for each new part from day one.

The result, 35 years on, is a moat with three reinforcing layers:

🔒 Switching Costs. Once an airline integrates HEICO’s parts into its maintenance and supply chain, switching to an alternative means significant re-qualification, regulatory hurdles and operational disruption. Airlines do not do this lightly for critical components. Once integrated, HEICO’s parts stay integrated.

📚 IP and Regulatory Protection. The catalog of 20,000 different PMA (Parts Manufacturer Approval) parts, along with the underlying intellectual property, engineering data and regulatory approvals, constitutes an asset that would be extraordinarily expensive and time-consuming to replicate. Each new PMA approval requires substantial R&D investment, regulatory navigation and technical expertise. HEICO has been building this catalog since the 1980s.

⚙️ The Safety Record. Over the company's lifetime, HEICO has sold over 80 million parts with zero service bulletins, zero airworthiness directives and zero in-flight shutdowns. In a safety-critical industry where airlines need complete confidence in their suppliers, this track record is virtually impossible to replicate and makes switching to an unproven competitor almost unthinkable.

The Mendelson Family — Skin in the Game

The business is run by the Mendelson family, and it shows. Laurans A. Mendelson (Executive Chairman, formerly CEO) and his sons Victor (Co-CEO) and Eric (Co-CEO) together own approximately 7-8% of the company — a stake worth roughly $3.5 billion at current prices. This is not a family collecting a salary. Their interests are entirely, structurally aligned with long-term shareholders.

Rochon noted this explicitly in his 2021 letter: “One of the reasons for our purchase in 2016 was our admiration for the members of the Mendelson family who run the company.”

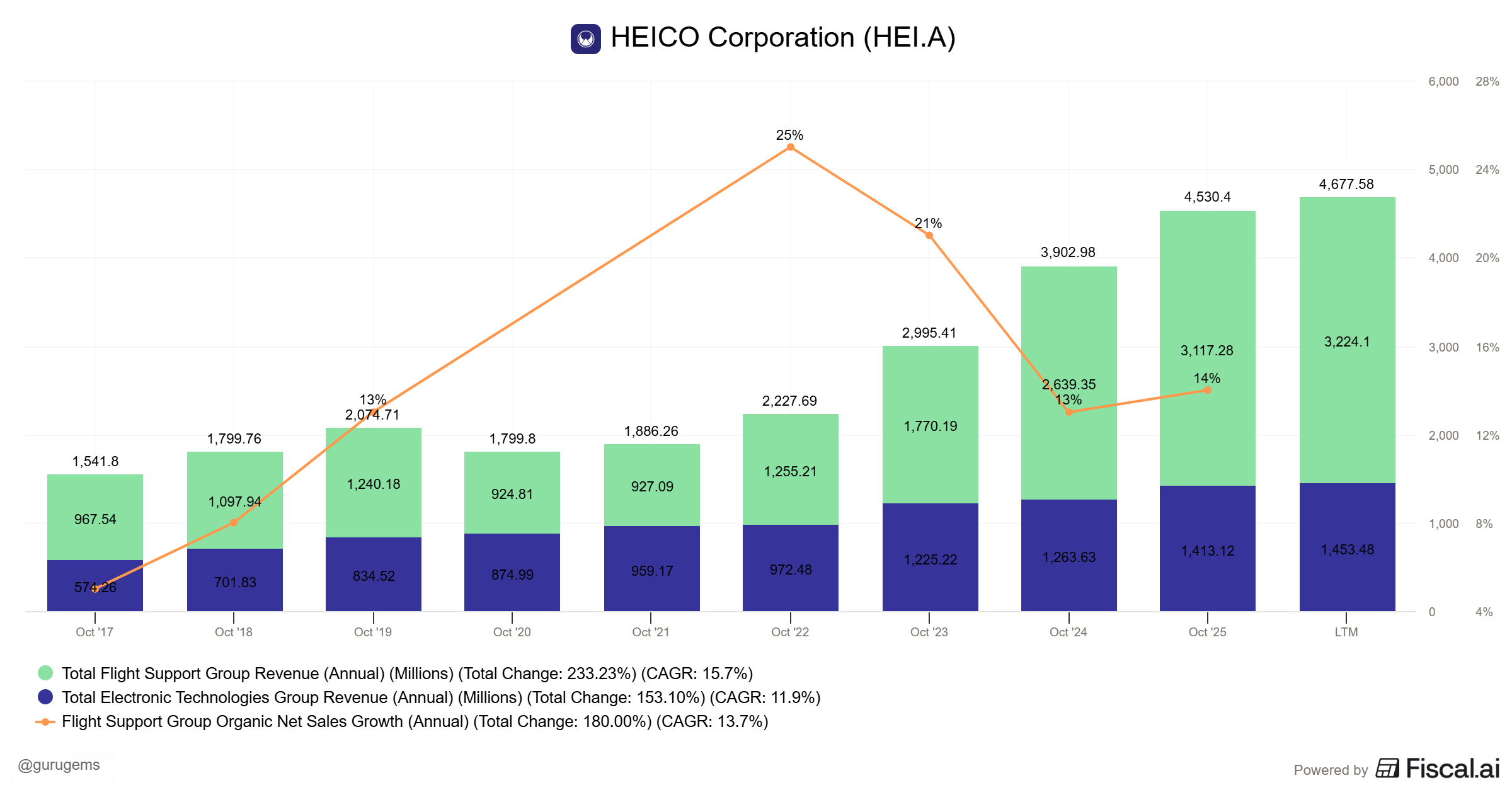

The Recent Numbers — Still Accelerating

In Q1 2026, HEICO reported record net income and strong increases in net sales:

Consolidated net sales up 14% year over year

Consolidated net income up 13% to $190.2 million

Flight Support Group: 15% organic growth

Electronic Technologies Group: 12% organic growth

Over the past decade, revenues have grown at nearly 13% CAGR and operating income at a 14.8% CAGR. The company has recently expanded into industrial gas turbine repair through the acquisition of EthosEnergy Group Limited. This is a significant new growth vector, serving the growing global power demand.

The track record since the Mendelsons took over in the late 1980s is truly phenomenal: a 23% compound annual growth rate in share price over 36 years. A $10,000 investment then would be worth over $9 million today. This is one of the greatest compounding records in American corporate history.

Berkshire Hathaway began acquiring a position in HEICO in Q2 2024. When both Rochon and Buffett are independently accumulating the same stock, it merits very serious attention.

For a more in-depth analysis of the company, I would highly recommend the below episode of The Investor’s Podcast.

It goes into great detail of HEICO’s business model and acquisition playbook and how the Mendelsons turned a small parts supplier into an aerospace giant.

I also recommend The Pursuit of Compounding’s article which has a mini deep-dive as well as an update on Fiscal 2025 year-end results.

2/ Don’t overpay

HEICO has rarely (never?) been cheap. And despite currently being down 25% from its 52-wk high, it is still not cheap today.

The stock currently trades at a forward P/E of ~48x. While this is a premium valuation, Rochon often reminds us that "wisdom is knowing when to break the rules" and that outstanding companies are often worth paying for.

HEICO is one of those companies that has always looked expensive to the casual observer and always proved justified to the patient long-term investor. Every year since the early 2000s, someone has said HEICO is too expensive. And every year, the business has grown into and beyond its multiple.

The stock is down 15% over the past month on a mix of 1) negative investor sentiment fearing rising competition, and 2) analyst downgrades. A further pullback could be a very interesting entry point for this high-quality compounder.

3/ Final decision

HEICO sits at the intersection of everything Rochon looks for: a wide and durable competitive advantage, family management with full alignment, a long runway for growth, and an exceptional compounding track record.

The fact that both Rochon and Buffett hold it independently is also a powerful signal.

I will be watching for a further pullback from current levels, which has historically occurred during any period of aviation macro weakness. When it comes (and it probably will), I intend to buy.

📌 Adding HEICO Corporation (HEI.A) to the Guru Gems Watch list

❕Just a reminder that you can access the Guru Gems watchlist here at any time

👜BONUS: The Full Circle - LVMH and the Return of Rochon

“LVMH is a French company that I have followed for a long time. I have always admired the many competitive advantages of the company and the management of its president Bernard Arnault.

During the euro crisis in the summer of 2011, LVMH stock fell to less than €100 and was trading at around 16 times earnings. To be able to acquire one of the best companies in the world at an attractive valuation is an opportunity that I should have known to seize. I seriously considered it but preferred to wait for an even more attractive evaluation. And I had several chances: the stock remained at a reasonable valuation for more than three years!

Since 2011, EPS has grown from €6.2 to €29.6 in 2022, a compound annual growth rate of 15%: a phenomenal performance for a company of this size. The stock reached €800 at the start of 2023 for an annual return of more than 20% over these eleven years. I am still looking for an excuse to explain this indecision.”

— François Rochon, 2022 Annual Letter — Gold Medal, Podium of Errors

Those who have followed Guru Gems from the beginning may recognize this passage. I quoted it in my second newsletter, when I introduced François Rochon for the first time and asked, in closing:

“I wonder if, at the current valuation, he is considering to finally including this gem in his portfolio.”

The answer — confirmed in a recent interview — is yes.

After more than 14 years of watching, admiring and awarding himself a Gold Medal for missing it, François Rochon has finally bought LVMH.

The circle that began with our first newsletter is now complete.

Why Now? Rochon in His Own Words

In his interview on We Study Billionaires, Rochon was asked directly why he finally pulled the trigger.

“I’m not that good in timing — I bought it last year and so far it has not produced good results. […] But I think the key factor is that you want the brand to be as strong as it’s ever been. Perhaps people are wary of buying a Louis Vuitton bag right now, but what you really want is a brand that still resonates with clients as quality, something you want to own because it’s of quality and also a symbol of wealth. I think those are intact.”

His five-year earnings thesis is specific:

“I think probably from here, earnings could increase 60 or 70% in the next five years — that’s a 10-11% annual growth rate. You’ve got a 2% dividend. Together, I think we should be able to attain our objective of finding a 13% grower including the dividend.”

He is enthusiastic about specific divisions he knows well: Louis Vuitton and Dior (the two most profitable luxury brands in the world), Tiffany (”a fantastic business — I followed it when it was separately listed”), and Sephora (”probably just 10% of revenues but growing pretty fast ”).

He is transparent about what he does not love: the spirits business (Moët & Chandon, Hennessy), where he sees a more secular challenge from generational shifts in alcohol consumption.

On China (roughly 20% of LVMH’s revenues) he is patient and structurally optimistic:

“Long-term it’s going to be a positive thing. China’s GDP per capita will continue to increase at a higher rate than North America. […] As they get richer, they’ll want to acquire LVMH products and other luxury products. There’ll be ups and downs, but they’re building a business for the next decades, not the next year or two.”

📌 I remain a holder of LVMH in the Guru Gems portfolio. Rochon’s purchase is the most meaningful external validation I could have hoped for.

That’s it for this week’s edition!

Thank you for reading and following along. You can find me on X @guru_gems for more Guru Gems insights.

Until next week!

Thanks for the shout out - nice to see the Mendelson family get some attention! I think they are under appreciated.

If only I was like Rochon and discovered HEICO a decade ago!” 🤑

Great post! I’m also looking at LVMH