Sir Chris Hohn & The TCI Way

S&P Global — A Toll Booth on Global Finance

“They say there is no free lunch in finance, but I do think long-termism in a great company is a free lunch” — Chris Hohn

In today’s edition:

👤 The Guru: Sir Christopher Hohn

🏛️ The Philosophy: TCI's fortress business approach

💎 The Gem: S&P Global (SPGI) — a familiar name with a fresh look

2-minute AI version:

👤 Guru in the spotlight: Chris Hohn

Christopher Hohn is one of the most successful - though not very public - investors of the past two decades.

He is the founder of The Children’s Investment Fund Management (TCI), a London-based hedge fund he launched in 2003, with a name that reflects his commitment that investing and purpose could coexist.

His results have been extraordinary. Over more than two decades, TCI has compounded at more than 18% per year. This is roughly nine percentage points ahead of the broader market.

In 2025 alone, the fund generated $18.9 billion in net gains, the single largest annual profit ever recorded by any hedge fund, surpassing Citadel’s previous $16 billion record from 2022.

“Investing is all about risk and return — and the vast majority of investors focus on return. But in my career I focused on risk. Return does matter, of course, but to me, risk was always the first thing that mattered.”

This risk-first framing is the key to understanding Hohn. He is not chasing the next hot thing. He is building a portfolio he can sleep with and hold for a decade.

What makes his record even more striking is that he achieved his results with a concentrated portfolio of 10-15 names, despite managing more than $75 billion.

The average holding period of TCI’s current portfolio is eight years. Some positions have been held for over a decade. This reflects his patient, concentrated ownership of the world’s best businesses.

Beyond investing, Hohn has committed to giving away essentially most of what he earns. The Children’s Investment Fund Foundation — seeded with his $10 million bonus from his first hedge fund job — has grown to over $6.5 billion in assets and donates more than $500 million per year to children’s health and climate change. He was knighted in 2014 for his philanthropy.

If you enjoy this newsletter, please help others discover it by clicking 🤍

And if you learned something useful, consider buying me a virtual coffee ☕

🏛️ TCI’s Fortress Business Model Playbook

Reading across his interviews and public statements, Hohn consistently emphasizes a few key ideas that guide TCI’s investment decisions, all centered around one central obsession: barriers to entry

“Most investors underestimate the forces of competition and disruption.”

1. 🏰 Fortress business models — barriers to entry above all else

For Hohn, the most important question about any business is not how fast it grows, but how well it is protected.

“We’re totally focused on fortress business models, where competition is limited and very difficult and so they have very high barriers to entry.”

The types of barriers he hunts for span a wide range:

Irreplaceable physical assets (airports, toll roads, railroads)

Intellectual property so complex it cannot be replicated (e.g., aircraft engines)

Network effects

Installed base and customer switching costs (e.g., mission-critical software)

Brand strength

Regulatory protection

Hohn’s preference is to find businesses with not just one of these, but several at once.

Aircraft engines are the perfect gems which have these multi-layered barriers to entry: IP, contracts, installed base. GE Aerospace (his ‘crown jewel’) and Safran SA (French aerospace and defense company) together make up more than 25% of his portfolio.

And while he loves aircraft engines, airlines on the other hand represent exactly what he avoids: growth without barriers.

“Airlines have been growing for 100 years — maybe 5% a year — fantastic growth. But collectively and cumulatively, the industry never made any money because competition was too strong. Growth without barriers to entry is not a combination you want.”

Pricing power is the ultimate test of a moat

Hohn has found that once you find one of these supercompanies that can dominate their industries, they have something special, which is pricing power.

The clearest test of whether a moat is real is a company’s ability to raise prices above inflation.

“There is a special group of super-companies that can price above inflation — and that’s, as Buffett taught, the test of whether you have the moat. Real pricing power above inflation can be very valuable.”

2. 🔭 Extreme long-termism — time horizon as competitive advantage

Most institutional investors hold a stock for under a year. Hohn holds for eight on average, and happily for twenty if the business warrants it. He calls this a “time horizon arbitrage”: the market systematically undervalues businesses that are great over decades but not exciting quarter to quarter.

“The value of a great company is only really seen over the long term.

This long-term view requires an important character trait: an almost stubborn refusal to sell.

“If you find something good — and it’s going to be good long term — stick with it. Don’t assume newer is always better.”

3. 🎯 Concentration — size your positions with conviction

Hohn holds roughly 10–15 positions, with meaningful stakes of around 10% or more in the top 8. He believes that if you have identified a true fortress business, adding more mediocre companies to ‘diversify’ only dilutes the quality of the portfolio.

“We’ve used concentration to great advantage. But it only makes sense where you have outsized risk/reward and conviction. That’s our formula for how we size positions.”

In one of this interviews he cites George Soros: “It doesn’t matter if you are right or wrong — all that matters is how big you are when you’re right and how big you are when you’re wrong.”

A very long list of industries to avoid

Hohn is quite explicit about what he won’t own. Banks, airlines, telecoms, insurance, utilities, traditional media, auto manufacturers, commodity producers, advertising agencies, traditional asset managers… all these industries are either too competitive, too cyclical, or too prone to disruption.

“We have figured out a lot of industries which have high and sustainable barriers to entry, and we pretty much ignore all other industries.”

Hohn estimates that only around 200 companies worldwide meet its definition of a truly high-quality business.

What the Wirecard short taught Hohn about independent thinking

Hohn's playbook is built around owning great businesses for decades. But one episode from his career stands out as a rare and instructive detour into short selling (i.e. betting against a company): Wirecard.

The German Enron

For years, Munich-based payments company Wirecard was celebrated as Germany's greatest fintech. It was a DAX 30 member valued at over €24 billion, backed by SoftBank, and given a clean audit by EY every year.

Red flags about its accounting had circulated since 2015, when the Financial Times first raised questions about its Asian operations. but Germany's financial regulator sided with Wirecard, banned short selling of the stock, and filed criminal complaints against FT journalists who reported on the fraud.

Hohn entered the picture in early 2020 with a short position, having applied the same accounting pattern recognition he learned at Harvard Business School: small auditor, no verifiable cash flows, empty offices in supposedly booming Asian subsidiaries.

When KPMG's special audit confirmed in April 2020 that it could not verify the existence of over €1 billion in foreign bank accounts, Hohn took the extraordinary step of filing a criminal complaint with Munich prosecutors against Wirecard's management and publicly calling for the CEO's removal.

In June 2020, €1.9 billion in company funds was revealed to be missing. Money that, Wirecard admitted, "probably never existed". The stock collapsed 98% and the company filed for insolvency days later.

What Hohn learned from this period

The lesson Hohn takes from Wirecard is not primarily about the profit. It is that shorting is structurally difficult.

“Over a dinner with Warren Buffett, I asked Buffett about shorting and he said that he and Charlie Munger never did it because they concluded it was too hard and unpredictable because of the investor psychology aspect of it.”

The first short seller to spot the Wirecard fraud, a decade earlier, had been forced to cover his position as the stock kept rising.

The deeper takeaway he applies to his long portfolio: fraud in plain sight is possible when institutions trust authority too much, and independent thinking — being willing to call something wrong even when the establishment says otherwise — is among the most valuable traits an investor can have.

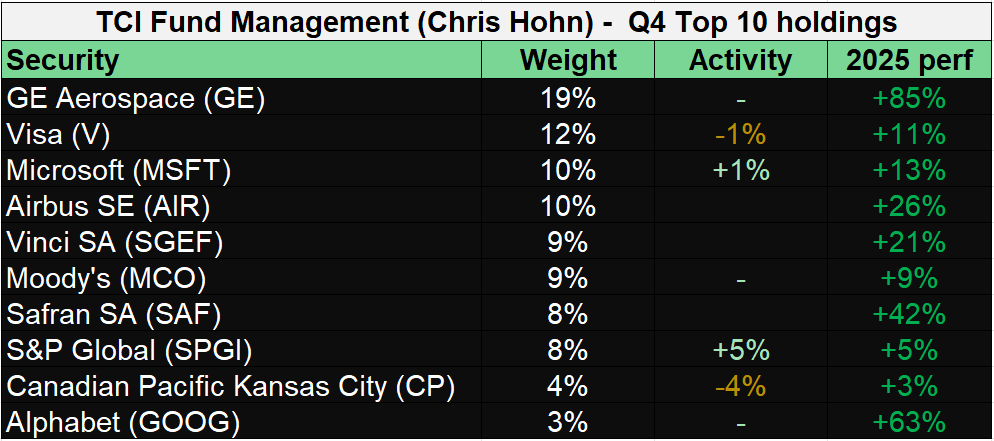

TCI portfolio

Below is an overview of Chris Hohn’s TCI stock portfolio at the end of Q4 2025. Note that the weights are approximations as the information is a combination of 13F filings (US companies) and shareholder reports (non-US companies), which may have different filing dates.

More than 90% of the $79 billion portfolio is concentrated in 10 names. This level of concentration would make most fund managers lose sleep, but for Hohn it is a consequence of his demanding criteria, making his investable universe very small.

The portfolio is a live demonstration of Hohn’s playbook: aircraft engines (GE Aerospace and Safran), payments networks (Visa), enterprise software with switching costs (Microsoft), credit rating duopolies (Moody’s and SPGI), toll roads and airports (Ferrovial, Aena), and railroads (CP and CNR).

In Q4 2025, Hohn added modestly to S&P Global (SPGI) a financial information and analytics company.

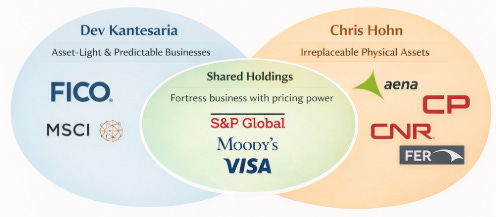

In my deep-dive on Dev Kantesaria, SPGI showed up as Valley Forge Capital's second-largest position at over 20% of his portfolio. Kantesaria has held it for years. And Hohn holds it too, at 8% of one of the most concentrated portfolios on earth.

When two of the world's most disciplined quality investors independently land on the same business, it deserves a very close look.

💎 The Gem: S&P Global Inc. (SPGI)

S&P Global is one of those companies that sounds boring but actually operates at the center of the global financial system.

It is the provider of the S&P 500 Index (the most replicated benchmark on earth), the world’s largest credit rating agency, a leading provider of financial data and analytics, and a dominant force in commodity pricing information.

S&P Global operates across five business segments:

Ratings — Credit ratings for bonds and debt instruments.

Market Intelligence — Data, analytics, and workflow tools for financial professionals. Subscription-based, ~85% recurring.

Indices — The S&P Dow Jones family of indices, including the S&P 500

Commodity Insights — Pricing benchmarks and data for energy and commodities markets (formerly Platts).

Mobility — Automotive data and analytics (includes former Carfax). Being spun off in 2026 as a standalone company.

2 of S&P Global’s divisions have operating margins above 60%

💰 To Buy or Not to Buy

1/ Buy good companies

There is no doubt that S&P Global is a high quality company. Two of the most respected quality investors in the world — Hohn and Kantesaria — hold it as a top position.

Its moats are historic, its margins are exceptional, and its business grows structurally with the global capital markets it serves.

Here is why SPGI fits the TCI Playbook

🏰 Fortress barriers to entry

S&P and Moody’s together control roughly 80% of the global credit ratings market — a duopoly enforced by regulatory recognition, investor mandates, and decades of institutional trust.

The Indices business is even more entrenched: the S&P 500 is the benchmark, not just a benchmark, with trillions of dollars of passive capital pegged to it. Every inflow to an S&P 500 ETF generates a licensing fee, with essentially zero marginal cost.

Market Intelligence subscribers embed S&P’s data into their daily workflows and compliance processes, creating high switching costs.

This is the multi-layered fortress model that Hohn is looking for.

The moat is confirmed by a real pricing power.

Because the cost of a credit rating is tiny relative to the size of a bond issuance, customers are highly insensitive to price.

If a company is issuing $1 billion in debt, the rating fee is essentially a rounding error.

That gives S&P Global enormous pricing power.

🔭 A business for the next 30 years?

S&P Global was founded in 1917. As long as corporations issue bonds, ratings are needed. As long as passive investing grows, index revenue grows. As long as financial professionals need data, Market Intelligence renews.

Hohn himself noted that Moody’s — his other ratings holding — has compounded revenues at 10% per year for a century. S&P’s upcoming Mobility spin-off simplifies and focuses the business further, leaving only the highest-quality, highest-margin core.

Will this still be in a dominant position in 20-30 years? Quite likely.

2/ Don’t overpay

High quality companies like SPGI rarely come cheap. But here is where it gets interesting. SPGI’s stock has had a difficult 12 months.

As of early March 2026, shares trade around $452, down roughly 22% from their 52-week high.

The market’s concern centers on two things: fears that AI disrupts financial data businesses, and a slightly disappointing 2026 earnings guidance that came in below Wall Street’s prior estimates.

The current forward P/E of ~23x is the cheapest SPGI has looked on a forward basis in many years.

The AI concern is worth examining a bit further.

S&P Global’s data is largely proprietary, structured, and deeply embedded in regulatory and contractual frameworks.

If anything, the AI supermachine needs reliable, trusted data to run on and that’s exactly what SPGI provides.

Case in point: S&P Global has already integrated its Capital IQ datasets directly into Claude, allowing financial professionals to query earnings transcripts, financials, and company intelligence through natural language.

The market appears to be applying a broad “data business = AI risk” discount without distinguishing between generic web content and S&P’s institutionalised, regulated financial intelligence.

Final decision

SPGI seems to tick all the boxes needed to make it into the Guru Gems portfolio.

📌 Decision: I’m adding S&P Global (SPGI) to the Guru Gems portfolio as a 3-4% initial position. As for any of my positions, I will be closely monitoring Hohn and Kantesaria’s moves and whether any other super investors may pick up the stock.

Hohn added slightly to his position in Q4, at a price between $475-$525, so at a current price of $452 I can buy it below that price.

That’s it for this week’s edition!

You can follow me on X @guru_gems and Substack @gurugems for more insights.

Until next week!

Nice one!