Portfolio Update March 2026 - My 'Podium of Errors'

A rough quarter, an honest look back

Welcome back!

Q1 2026 is behind us, time for a portfolio update.

Start here if you are new to Guru Gems.

No time to read this week’s update? Here is your 2-minute AI summary:

💎 Guru Gems Portfolio update

The broader market had a tough start to the year, and unfortunately the Guru Gems portfolio was no exception.

Perfect storm

It was a bit of a ‘perfect storm’ for the portfolio this quarter. The SaaSpocalypse hammered CSU and CCC (both down more than 30% since I bought them), while LVMH had its worst-ever start to a year as the war in the Middle East added even more pressure on the luxury goods outlook. These are three of the larger positions in the portfolio, so the pain is real.

I won’t lie, it’s not comfortable sitting on drawdowns like these. I would much prefer to come here and tell you I’m crushing it. But unfortunately that’s not the case (yet), and I plan to keep sharing very openly my learning journey with Guru Gems.

Do I still believe in my stock picks? Absolutely.

But have I made some mistakes along the way? Without a doubt.

The full Guru Gems portfolio and all transactions are available in the Guru Master Google Doc.

Looking back

As I approach the one-year anniversary of Guru Gems, it feels like the right time to reflect on what went wrong, and more importantly, what I can learn from it.

And who better to borrow a framework from than François Rochon? Last week I published a deep-dive on Rochon, one of my all-time favorite Gurus, and I’m quite proud of how it turned out, with lots of timeless investing wisdom in there… and it’s all free ;)

One of the traditions Rochon has in his annual letters is a ‘Podium of Errors’, a ranking of his biggest mistakes of the year. I love this idea, so I’m stealing the concept.

Before I share my podium, here is an extract from Rochon’s 2014 letter that feels very appropriate right now:

We have made many times our money with O'Reilly Automotive over 10 years. But after the initial four years of owning O’Reilly, we had not yet made a profit. Just a few years is not a long time in the world of business and investment.

🏆 My Podium of Errors

It is with a constructive attitude, to always improve as investors, that we provide this detailed analysis - François Rochon, every annual letter

🥉 Bronze - Magnera (MAGN)

Magnera was my Joel Greenblatt-inspired 'special situation' pick from May 2025. The company was formed by merging Berry Global's Health, Hygiene & Specialties non-wovens division with Glatfelter Corporation in late 2024.

Michael Burry had also started a position in Q4 2024, probably also seeing an interesting ‘special situation’ in this newly formed merger.

With a market cap below $500M, Magnera is a proper small cap and small caps can be wild. The stock surged 30% in Q4 but then dropped 37% in Q1 despite results that were largely in line with expectations.

It's now a <1% position in the portfolio, so the actual damage is minimal. I'll keep it, but I'm not expecting fireworks.

The lesson: Not every good idea belongs in every portfolio. Magnera might be perfectly fine in a more diversified strategy like my Magic Formula portfolio, but in a concentrated portfolio like Guru Gems where the focus is on quality companies, a volatile small cap probably doesn't fit.

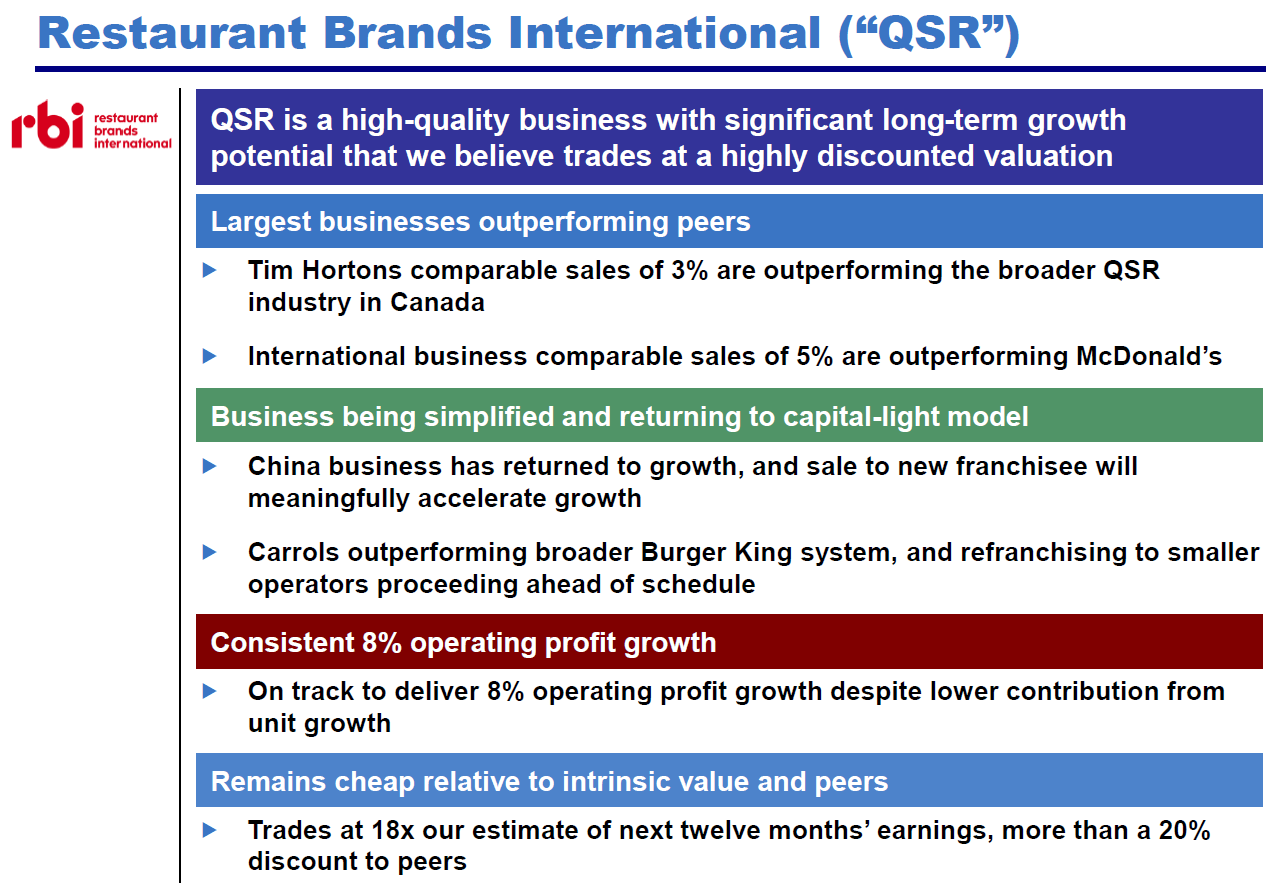

🥈 Silver - Restaurant Brands International (QSR)

This one is what François Rochon calls an error of omission.

I came across QSR when I did my deep-dive on Chris Davis. QSR owns and operates Burger King, Tim Hortons, Popeyes and Firehouse Subs.

It was a newer position for Davis, the valuation looked reasonable, and the business was solid. I wrote that QSR had traded as low as $60 in Q1 of 2025 and that this was probably the price at which Davis would have bought it and Seth Klarman would have added to his position. The price came very close to $60 again in September, but I was waiting for it go down a bit more, which didn’t happen, and it is now up around 24% from that September low.

Having a position in physical restaurants, where AI disruption fears don't really apply, would have been a nice buffer during a quarter like the one we just had. (In my Davis post I wrote: “This is definitely not a flashy AI stock nor a high-growth SaaS business.”)

Hindsight is always 20/20, of course. But QSR stays high on my watchlist, especially since it's also a significant holding in Bill Ackman's portfolio. Three great Gurus (Davis, Klarman, Ackman) on the same name is always a signal worth paying attention to.

The lesson: A position in a more defensive, real-world quality business like QSR could have added some balance to the portfolio. Going forward, I want to make sure I also take this into consideration when starting a new position.

→ If you enjoy this newsletter, please subscribe and like this post 🤍

→ If you find value here, consider buying me a virtual coffee ☕

🥇 Gold - Constellation Software (position size)

And here’s the big one.

Constellation Software is my worst performer, down 26% in Q1 alone. But that’s not why it gets the Gold medal. Stocks go down, that happens. The mistake was how much I put in from the start.

When I initiated the position, I went in at 8.5% of the portfolio. Two weeks later, I added more and brought it up to 11%. The stock then proceeded to fall even further. Looking back, it would have been much wiser to start at 3-4% and scale in gradually as the thesis played out (which so far it hasn’t).

I was reminded of this lesson when reading Stock Master Maestros, which I recently wrote about:

A clear pattern from the book is that many of the greatest investors start every new position at around 3% or less, regardless of how convinced they are. The idea is simple: let the position prove itself before you size it up.

“Don’t assume you can add value by sizing your positions based on conviction. Entering every position at a standard size and then letting them run, works.”

The lesson: Conviction is not the same as timing. I still believe I was right to be excited about Constellation Software, but I was wrong to go in heavy from day one. Starting small gives you room to average down if the stock keeps falling, and keeps the pain manageable if it does.

What Rochon says about Constellation

It’s reassuring to read what François Rochon had to say about Constellation in his latest annual letter. Constellation is one of Giverny Capital’s largest holdings, and the stock fell 26% in 2025 and another 25% drop so far in 2026.

But as Rochon pointed out, the decline is completely disconnected from the business: revenue grew 15% in 2025, adjusted EPS climbed 21%, and since Giverny’s initial purchase in 2014, earnings per share have compounded at roughly 20% annually.

Rochon’s argument against the AI disruption narrative is in line with what I had written in my January portfolio update. Constellation owns more than 1,000 niche software businesses, each deeply embedded in its customers’ daily operations and rarely representing a significant cost. As he puts it:

It seems unrealistic to believe that an operator of a dozen mini-golf courses is going to start coding their own AI-powered reservation software to save something like $5,000 in annual fees!

Rochon writes that AI could actually help Constellation, since the software sell-off has dramatically lowered acquisition prices. Cheaper acquisitions mean better returns on invested capital for a company whose entire model is built on buying niche software.

Bottom line: Rochon remains confident and intends to keep his shares. Coming from someone with a 32-year track record of 14.7% annualized returns, that conviction carries weight and reinforces my own decision to hold.

👀 Looking ahead and Watchlist update

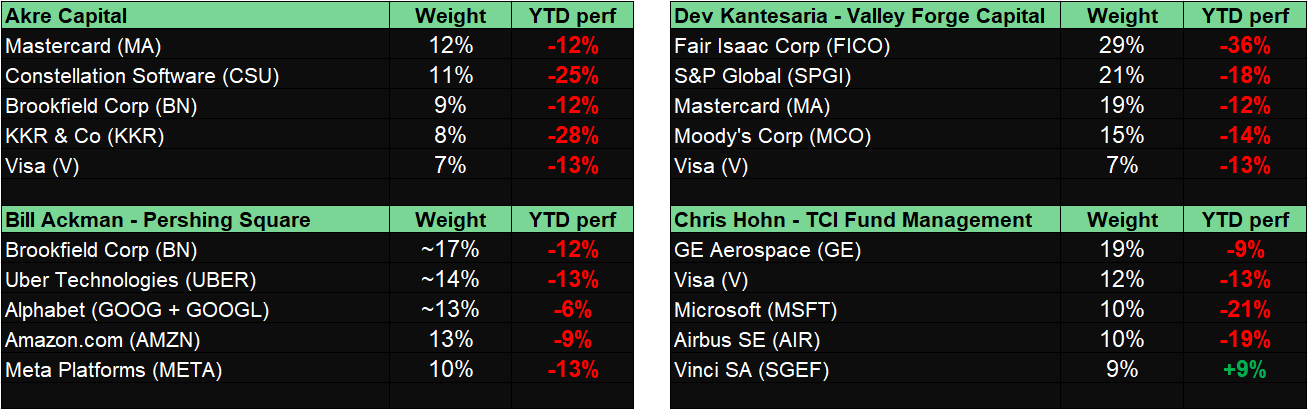

It’s not just the Guru Gems portfolio that has been hit hard. Some of the best ‘quality’ investors are sitting on significant drawdowns too.

Here is what the year-to-date (3 Apr 2026) performance looks like for some of the great investors I have covered in earlier editions. As you can see, there’s a lot of red in this table…

Watchlist Update

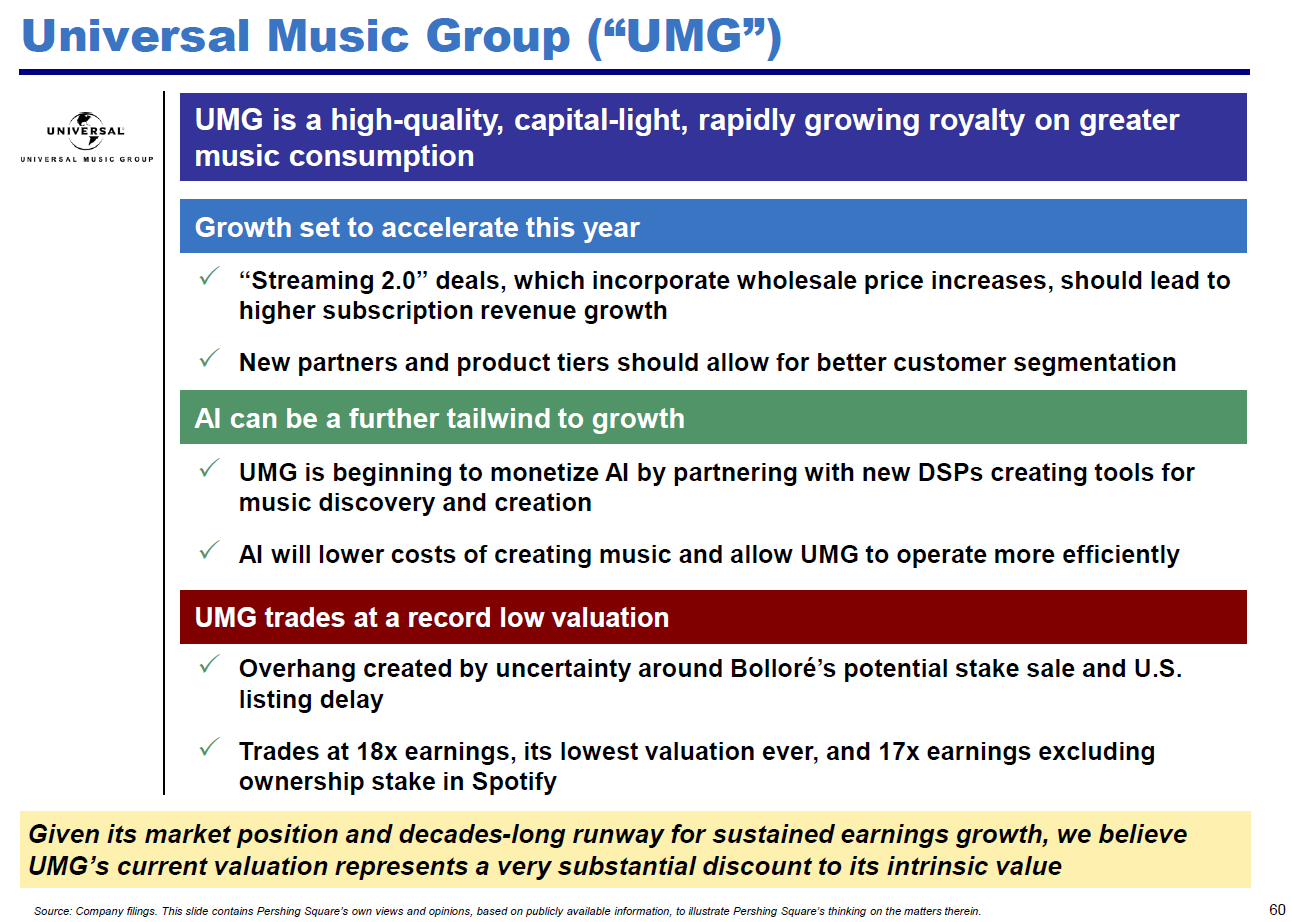

Last week I covered François Rochon in a deep-dive, and one of the things that caught my eye is that Rochon added a new position in Universal Music Group (UMG).

UMG is the world’s largest music company and home to Taylor Swift, Drake, The Weeknd, BTS, and many others with a catalog of nearly 5 million songs.

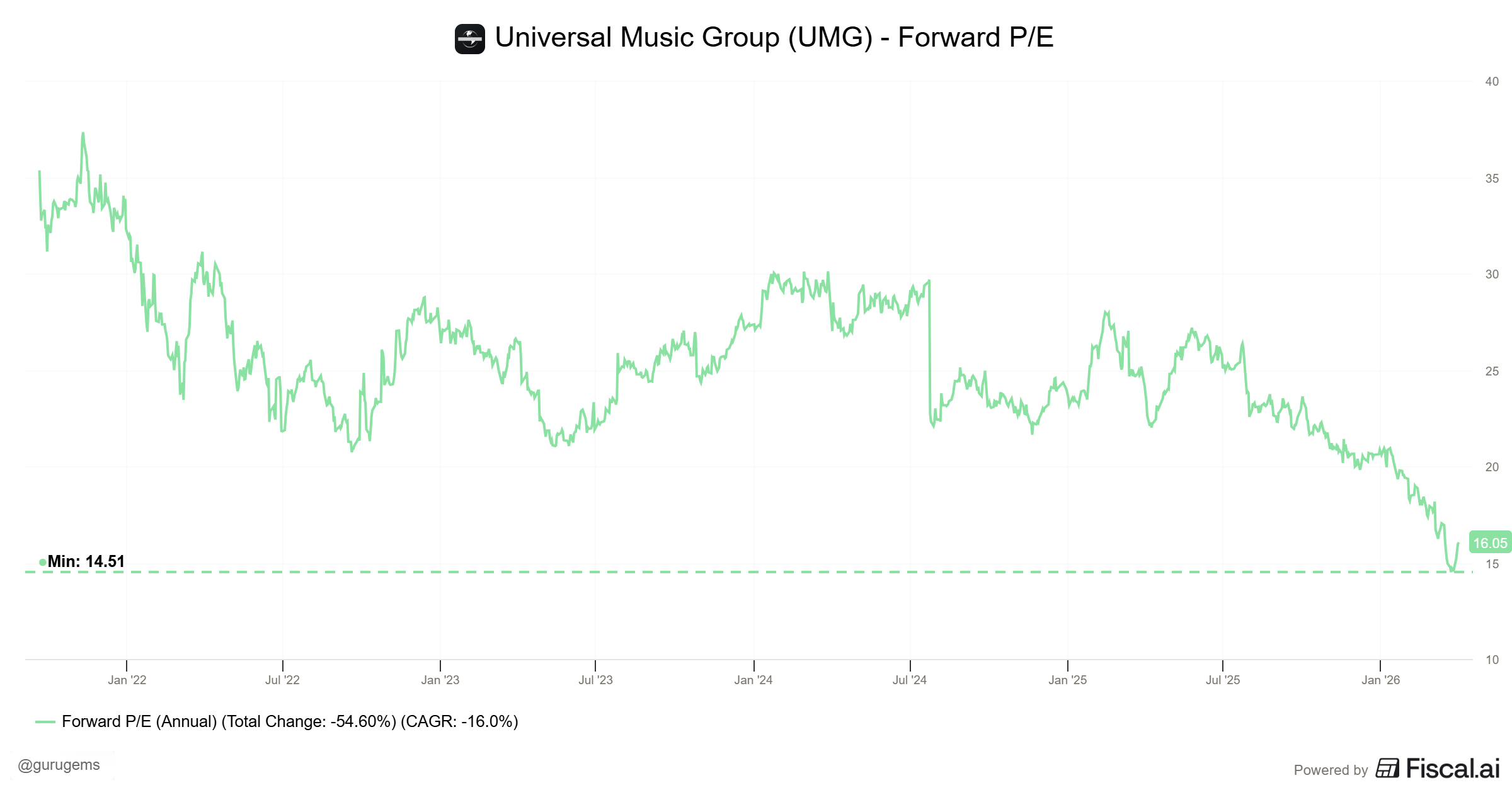

The stock has been beaten up pretty badly, trading at around €17, down 40% from its 52-week highs. At roughly 16x forward earnings, it’s trading near its cheapest valuation ever.

UMG is also a significant position in Bill Ackman’s portfolio, which adds another strong Guru signal. Two Gurus owning the same stock at its lowest-ever valuation, that’s the kind of setup that is worth studying more closely.

I’ve added UMG to the watchlist in my Guru Master Google Doc.

That’s it for this week…thanks for reading and I’ll be back next week with a special Guru Gems anniversary edition!