3 Lessons from 'Stock Master Maestros'

+ Watchlist update: MOH, FICO, MELI, CPNG, MA

Welcome to a new edition of Guru Gems, where I study the world’s long-term investing masters and build a portfolio of quality companies based on their wisdom.

In my most recent Guru deep-dive, I covered Chris Hohn, an exceptional investor who has compounded money at more than 18% per year.

In today’s edition:

📚 3 lessons from the book Stock Master Maestros, with a spotlight on Greg Padilla

📋 Guru Gems Watchlist Update: 5 stocks worth watching after recent sell-offs

Here is the 2 minute AI audio version:

📖 PART 1: 3 Lessons from 'Stock Master Maestros'

There are Stock Market Wizards and then there are Stock Market Maestros.

In my mind, wizards are exceptionally skilled traders who make money by speculating on the movements of stocks, currencies, commodities, bonds and cryptocurrencies. They are typically short-term oriented, and they aren’t necessarily focused on corporate fundamentals.

Maestros, on the other hand, are investors, not traders. They invest based on fundamentals, with reference to valuation and sometimes to technical analysis. They hold their positions for months and years, not hours or days. Maestros are playing a longer game. And they’re doing it on behalf of ordinary investors like you and me, using the same public equities the rest of us use to build our portfolios.

Stock Master Maestros by Lee Freeman-Shor and Clare Flynn Levy is a follow-up to Freeman-Shor’s bestseller The Art of Execution: How the World’s Best Investors Get It Wrong and Still Make Money, which revealed the winning habits of 45 of the world’s top fund managers and categorised them into 5 ‘tribes’: Assassins, Hunters, Rabbits, Raiders and Connoisseurs.

The findings from that book showed that it was how an investor behaved after they had invested in an idea that determined their success or failure (i.e. how much they let winners run and how fast they cut their losses or added to a losing position)

How they reacted to winning and losing mattered more than the stocks they picked to invest in.

This is quite insightful and is something that made me think of what legendary hedge fund manager Stan Druckenmiller has said a few times in interviews:

“Invest, then investigate”

Here is a great interview with Druckenmiller from last month:

So what separates the great investors from the rest is not what they pick but how they behave once they're in it.

With Stock Master Maestros, Freeman-Shor takes this a step further by profiling 12 investors who have been objectively identified — through detailed analysis of their trading data by Essentia Analytics — as true “Maestros” of execution. The book walks through their winning and losing ideas with real case studies.

Today I will highlight one of the featured investors: Greg Padilla.

Who is Greg Padilla?

Greg Padilla is a Portfolio Manager and Managing Partner at Aristotle Capital, a Los Angeles-based investment firm managing over $90 billion in assets.

He was a key contributor to a top ranked global equity fund in 2012, one of the few that outperformed both in the down market of the Global Financial Crisis and in the later bull run.

What makes Greg’s inclusion in the book particularly interesting is the data behind it. Essentia Analytics analysed 12 years of his historical trade data and uncovered some remarkable stats:

Hit rate: 56% — He gets it right more than half the time (the median for even top-performing fund managers was just 45%)

Payoff ratio: 216% — His average winner wins 2.16× as much as his average loser loses

That payoff ratio is the key number. It means that when Greg is right, he wins big. And when he’s wrong, he limits the damage. Those are the features of a true ‘Connoisseur’ and ‘Assassin’.

1️⃣ Lesson 1: Look for Catalysts

At Aristotle Capital, every investment must meet three criteria: quality company, attractive valuation, and a compelling catalyst. The first two are principles we’ve seen with virtually every Guru studied so far. But the third is what sets Aristotle apart.

Padilla is very specific about what type of catalysts they are looking for. Catalysts are not short-term events like an earnings revision. They are fundamental changes already underway inside a business: a new management team, a new product line, or a resolution of legal proceedings.

This emphasis on catalysts comes from hard-won experience. Earlier in his career, Padilla bought stocks simply because they were cheap. And he got burned repeatedly. The catalyst requirement is what protects Aristotle from value traps; cheap stocks that stay cheap because nothing is changing.

This lesson also applies in reverse: when a key manager leaves, it can be a catalyst to sell.

My takeaway

When looking at the Guru Gems watchlist (Part 2 of this newsletter), it will be good to ask: What is the catalyst? A cheap stock without a catalyst is just a cheap stock. But the real Gems are quality companies at an attractive valuation with an identifiable catalyst.

If you enjoy this newsletter, please help others discover it by clicking 🤍

2️⃣ Lesson 2: "Why Are We Idiots?" — The Power of the Pre-Mortem

Before making any new investment, Greg and his team perform what they call a WAWI, short for “Why Are We Idiots?”

It’s essentially a pre-mortem exercise. Before a single dollar is invested, the team asks: “What are the most likely reasons we will NOT make money in this investment? What are our primary concerns?”

By identifying the key risks upfront, the team creates a reference list they can monitor throughout the life of the investment.

‘WAWI’ also helps them in their sell decisions. If one of the risks they have identified for that stock plays out, it’s the team’s cue to strongly consider stepping aside.

My takeaway

I think the WAWI exercise is something every investor can apply. Before adding a stock to your portfolio, it helps to write down: “Why am I an idiot for buying this?” If you can’t identify at least 2-3 clear risks, you probably don’t understand the company well enough.

3️⃣ Lesson 3: Let Winners Run — And Don't Double Down on Losers

This is probably the most important lesson from Greg Padilla’s chapter, and it directly explains that impressive 216% payoff ratio.

When Padilla enters a position, he invests a standard 2-2.5% regardless of the company. No finessing the entry, no higher weight for higher-conviction ideas.

He then lets the position float: if it does well, the weight drifts up. If it doesn’t, the weight drifts down.

“We came across a study that showed that the vast majority of fund managers do not add any value from trading - that is, from adjusting position size and timing their decisions. We know that adding and trimming positions is not part of our edge. People like to trade because it makes them feel good, like they are adding value, but are they?”

The only time Padilla trims, is when a position hits 6% of the portfolio, which is purely for risk control.

But here’s where it gets really interesting: Padilla rarely adds to losers.

“By not adjusting the size of the position after the initial buy, we are making an active decision to manage mistakes. We are avoiding turning a minor mistake into a big mistake. That’s been a big secret of our success: not turning small mistakes into big ones.”

He learned this the hard way during the 2008 financial crisis. Earlier in his career, when running deep-value portfolios, he would throw more money at a losing investment. But the outcomes told a different story. As he puts it: “If I could go back 20 years and give myself some advice, it would be, ‘it’s cheap for a reason, Greg.’”

Combined with the discipline to let winners run, this approach creates a natural asymmetry: big winners more than offset small losers. It’s how you get to a 216% payoff ratio.

My takeaway: This is a powerful lesson and one that I will try to better implement going forward. Alphabet has been a massive winner in my portfolio and so far I have resisted the temptation to trim it, but I have added to some of my losers, which is maybe something I need to stop doing…

👀 PART 2: Guru Gems Watchlist Update

The markets have been going through some turbulence lately, and a number of high-quality companies have seen their share prices decline significantly.

Below are 5 companies I’m keeping a close eye on. For each, I’ll share why the stock has declined and which Gurus own it.

As we just learned from Greg Padilla, a stock that has dropped a lot isn’t necessarily cheap; “it’s cheap for a reason.” So, for each stock, I will also try to identify whether there’s a catalyst for recovery or whether the decline reflects genuine long-term deterioration.

You can access the full Watchlist in the Guru Gems Master Google Doc

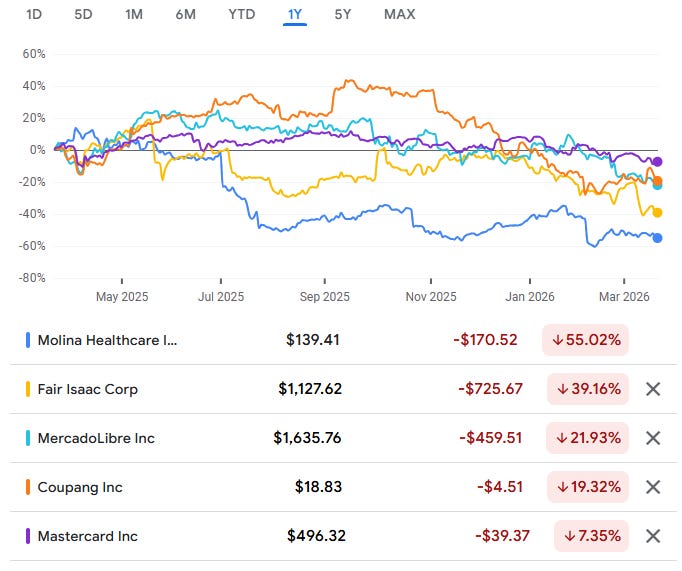

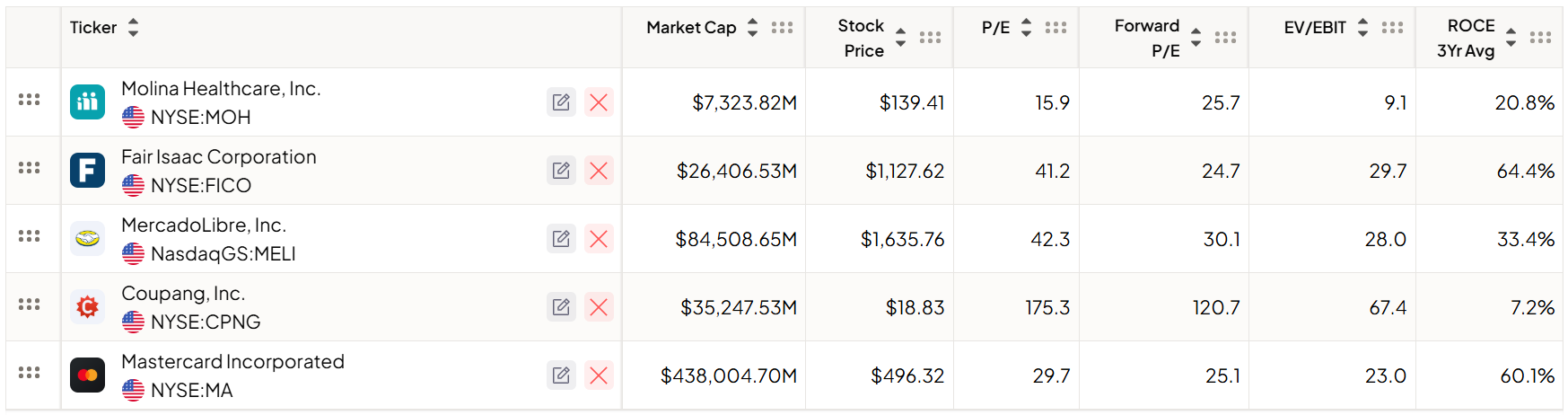

1/ Molina Healthcare (MOH) 📉 -55% over past year, -61% below 52-wk high

What happened?

This is the most dramatic decline on the watchlist. Molina reported a catastrophic Q4, posting a loss of $2.75 per share. Even worse, 2026 guidance of just $5.00 EPS was less than half of the consensus.

Surging medical costs in Medicaid, unfavorable premium adjustments in California, and underperformance in Medicare Advantage Part D (which they plan to exit in 2027) were the main drivers for the decline.

The decline has been so severe that Molina is being removed from the S&P 500 and moved to the S&P SmallCap 600.

Which Gurus own it?

Michael Burry, Bill Nygren, and Seth Klarman own the stock and believe it is a long-term opportunity. Michael Burry has written an extensive article about MOH and why he believes MOH is a ‘gem of an insurance company stock’.

Catalyst?

The catalyst identified by Michael Burry is the acquisition strategy. The very industry distress hurting Molina’s margins is simultaneously creating a full pipeline of struggling local health plans that can be acquired, something in which Molina has a proven track record.

I already own Molina in my Magic Formula portfolio, but as I wrote in my 2026 Watchlist post, I may also consider adding it to the Guru Gems portfolio, especially if it keeps declining back to $100/share where it would be a “generational buy” according to Burry.

2/ Fair Isaac Corporation (FICO) 📉 -40% over past year, -49% below 52-wk high

What happened?

FICO, the company behind the FICO credit score, has been hit by a perfect storm.

Earlier in March, the company announced a $1 billion offering of Senior Notes, which triggered negative reactions from investors as it raised potential liquidity concerns and questions about future financial stability.

Additionally, The FHFA (government agency) has pushed for a “Lender Choice” model, allowing alternative credit models like VantageScore 4.0. This would end decades of monopoly status in the mortgage market.

Despite this, Q1 2026 results were solid: revenue up 16% YoY to $512M, with EPS beating estimates.

Which Gurus own it?

Dev Kantesaria, Akre Capital and Lindsell Train.

Dev Kantesaria’s conviction is remarkable, nearly a third of his portfolio is in this single stock.

Catalyst?

FICO’s Platform revenue (growing 33% YoY) is becoming a bigger part of the business, which could help offset scoring pressure.

Also, acceleration of share repurchases is seen as a strong indicator of FICO’s robust free cash flow. But the regulatory picture needs to clarify before this becomes actionable.

Read more about FICO in my deep-dive on Dev Kantesaria

3/ MercadoLibre (MELI) 📉 -22% over past year, -38% below 52-wk high

What happened?

MercadoLibre, the dominant e-commerce and fintech platform in Latin America, spooked the market with a disappointing earnings report, leading to analyst downgrades and reduced price targets.

Revenue growth remained strong at 47% YoY (currency neutral), items sold rose 43%, and the company added 6.4 million new customers in Q4. But operating margin dropped from 13.5% to 10.1%, and EPS missed consensus.

Management says this is deliberate: they’re investing heavily in lowering free shipping thresholds in Brazil, building digital banks in Mexico and Argentina, and launching credit cards to capture market share while the opportunity is wide open.

Which Gurus own it?

Stan Druckenmiller and Miller Value Partners (here is their investment thesis). Michael Burry also highlighted it as a stock on his watchlist (target price ~$1200).

Catalyst?

Ecommerce penetration rates in the region (~14%) are roughly half the levels of more developed countries (27%-32% in US/UK/China), making the structural growth runway very significant.

Additionally, MercadoPago (fintech) has 78% AUM growth and is planning to become the largest digital bank in Mexico and Argentina. At a forward P/E of ~30x with 40%+ revenue growth and a Price/FCF under 9x, this is getting genuinely interesting.

4/ Coupang (CPNG) 📉 -19% over past year, -44% below 52-wk high

What happened?

Coupang, often called the “Amazon of South Korea,” has had a rough stretch. The main reason is a massive data breach affecting 33+ million accounts, followed by the CEO’s resignation and regulatory probes. Nomura slashed its 2026 EPS forecast by 95%, citing potential fines of up to $900 million. Q4 earnings missed estimates (EPS -$0.01 vs. $0.04 expected), and revenue came in light at $8.8B. The Farfetch acquisition has also weighed on profitability.

Which Gurus own it?

Stan Druckenmiller increased his position by 46% in Q4. Miller Value Partners also own it.

Catalyst?

Hard to identify right now. The regulatory fallout and legal challenges create significant uncertainty. The core e-commerce business (24.7M active buyers, dominant logistics) is strong, but the near-term uncertainty is real. As Greg Padilla would say, this is one where you need to “check yourself and be humble.”

5/ Mastercard (MA) 📉 -7% over past year, -18% below 52-wk high

What happened?

Mastercard faced multiple headwinds in early 2026: a proposal to cap credit card interest rates at 10% (which hit all payment stocks), the $1.8B acquisition of stablecoin infrastructure provider BVNK (which spooked some investors), and AI disruption concerns (fueled by the now famous Citrini Research report).

But the business itself is firing on all cylinders: Q4 revenue of $8.81B beat estimates, EPS of $4.76 was well ahead of the $4.24 consensus (a 12% surprise!), and the company raised its dividend by 14%.

Which Gurus own it?

Many of them…

Dev Kantesaria (~19%), Akre Capital (~13%), Thomas Russo (~10%), Peter Keefe (~6%), John Armitage (~3%), Berkshire Hathaway (~1%), Christopher Tsai (~2%), François Rochon (<1%)

Catalyst?

The shift from cash to digital payments continues to be one of the most powerful global trends. Electronic payments only surpassed cash payments on a global basis a few years ago, so there is still plenty of runway for growth.

Mastercard’s network model (fees on transaction volume) is incredibly durable.

The BVNK acquisition also positions them in stablecoins and tokenized settlements.

With many Gurus owning the stock, long-term growth opportunities and a low valuation (see chart below), this could be a really interesting company to add to the Guru Gems portfolio...

That’s it for this week! Please like or share if you find these insights valuable.

You can follow me on X @guru_gems and Substack @gurugems for more insights.

Until next week!

FICO, particularly at these levels, is worthy of further research. MELI would be intriguing if not for its fintech business, as I avoid banks and unsecured lending. MA is a great company.

MA and V look like great opportunities at current valuations