Portfolio Update February 2026 - Gains & Pains

Software stocks caught up in the SaaS massacre

Welcome back!

February is behind us, time for a portfolio update.

I’m currently working on two Guru deep-dives for the coming weeks (François Rochon and Chris Hohn). There is a LOT to learn from these two masters of investing, so stay tuned!

Start here if you are new to Guru Gems.

No time to read this week’s update? Here is your 2-minute AI summary:

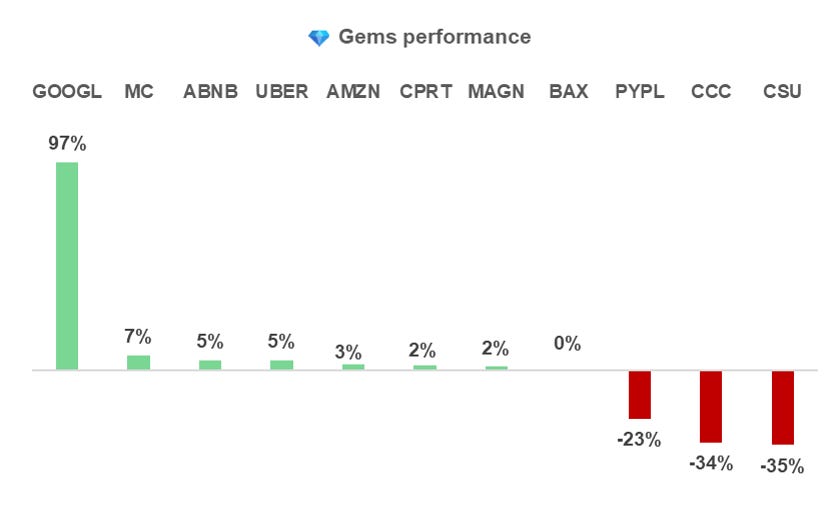

💎 Guru Gems Portfolio update

February 2026 will be remembered for the SaaS massacre, and the software companies in the Guru Gems portfolio certainly felt it.

The full portfolio and all transactions are available in the Guru Master Google Doc.

In the next section I will take a closer look at the companies in the Guru Gems portfolio.

I will group them into three clusters, as I explained in my post last week covering the latest 13F moves.

Cluster 1 — Clear Guru signals, strong business fundamentals

🔎 Alphabet

Alphabet continues to lead on AI innovation:

Gemini 3.1 Pro leads the Artificial Analysis Intelligence Index, ahead of Claude Opus 4.6, while costing less than half as much to run.

Google just rolled out Nano Banana 2, the upgraded version of its viral image model, now powered by real-time information and images from web search — claiming the #1 spot on text-to-image leaderboards.

Alphabet is still a double in the portfolio and I may trim the position slightly but for now I’m leaving it as is.

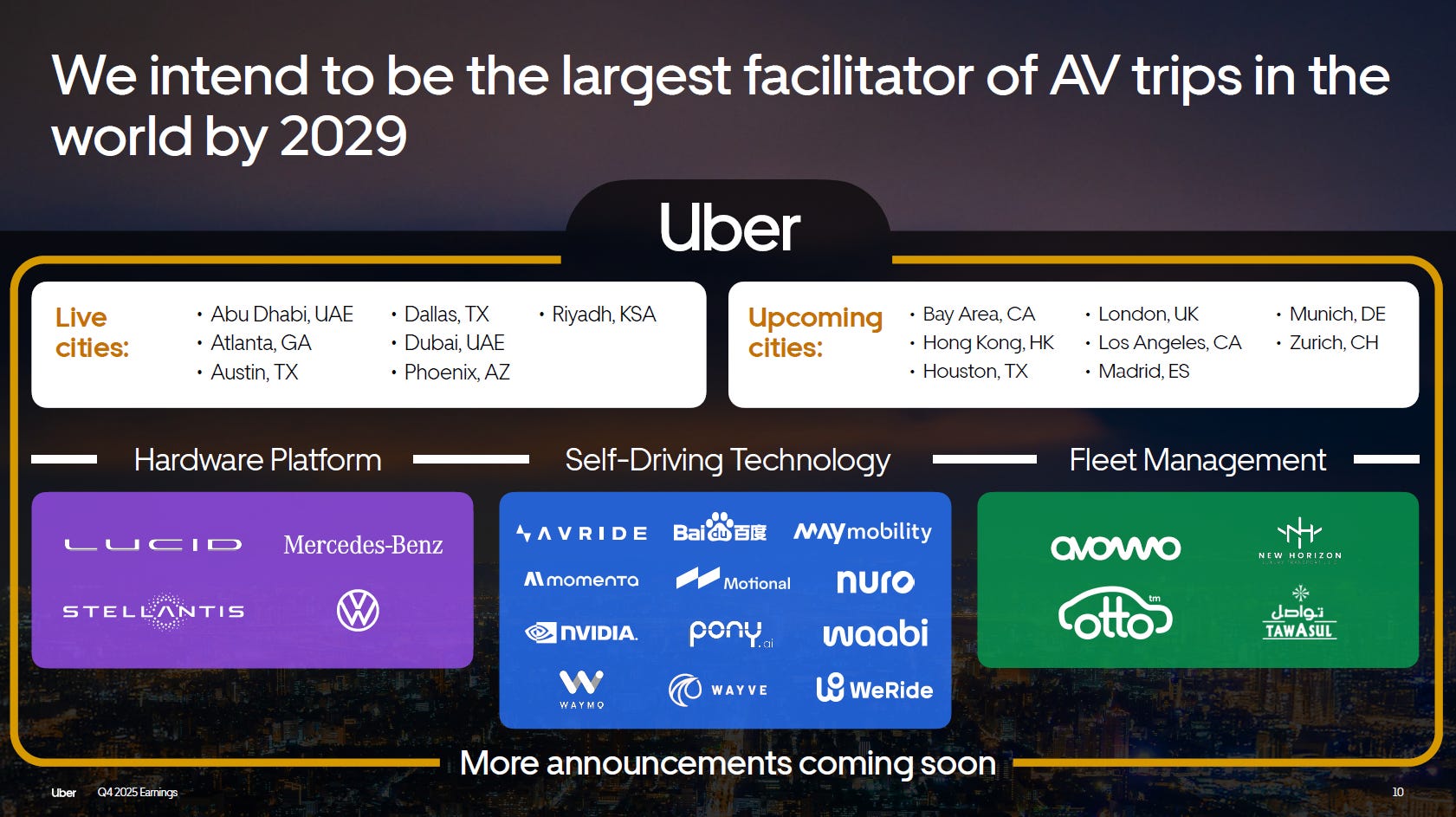

🚗 Uber

Uber delivered another outstanding quarter in Q4 2025. Revenue grew 20% to $14.4 billion, gross bookings jumped 22% to $54.1 billion, and full-year free cash flow hit $9.8 billion, up 42%.

The stock dipped ~5% after earnings on an EPS miss and softer Q1 guidance, which is probably more noise than signal.

In their recent Q4 and full year 2025 earnings call, management re-iterated that Uber is strategically positioning itself for a future where autonomous vehicles (AVs) are a significant growth driver, and an opportunity to expand the overall mobility market rather than a direct competitive threat.

Finally, Uber’s newly promoted CFO, Krishnamurthy Balaji, bought $1.6M worth of Uber shares shortly after his appointment. Always a good sign.

I have been buying Uber throughout the past week and it is now a ~9% position. I might buy more if the price drops back under $70.

🏪 Amazon

Following the Gurus’ big Q4 moves, I initiated a position in Amazon. It was the most bought stock by super investors in Q4.

I bought at $204, which is cheaper than what the Gurus have paid for it during Q4. It’s currently ~4% of the portfolio and I may add more over the coming weeks.

Cluster 2 — Guru conviction, business has ‘temporary headwinds’

👜 LVMH

An interesting development this week: CEO Bernard Arnault crossed the 50% ownership threshold in LVMH.

The Arnault family raised its stake from 49.77% at the end of 2025 to 50.01%, formally securing majority control of the group and bringing their voting rights to nearly 66%.

The family spent roughly €407 million buying shares on the market in late January and early February, immediately after LVMH reported weaker-than-expected full-year results.

The stock is down ~15% this year after mixed Q4 earnings, but it is still 7% above my average buying price.

🛌 Airbnb

Airbnb reported mixed results for 2025.

Revenue grew 10% to $12.2 billion, driven by growth in Nights and Experiences Booked and a modest increase in Average Daily Rate.

However, net income declined 5% to $2.5 billion, weighed down by higher compensation and marketing expenses as the company invests heavily in new business lines.

It’s a growth-versus-profitability trade-off, with expansion in several international countries and launch of experiences and services hopefully leading to higher profitability in the future.

⚕️ Baxter

Baxter sold off sharply after reporting weaker-than-expected quarterly earnings and adjusted EPS for 2026, but recovered in the following days.

“While the top line exceeds our expectations, adjusted EPS fell short” — Baxter CEO Andrew Hider

The stock is still up ~4% YTD and is back around my average purchase price.

Baxter remains a ‘turnaround play’. There is already a lot of pessimism priced into the stock, and a successful implementation of their new operating model could be a meaningful catalyst.

A few weeks ago, we internally announced the new operating model, and it's designed around simplifying our organization, accelerating innovation, and improving performance.

— Baxter CEO Andrew Hider

🛻 Copart

Copart is another name facing temporary headwinds.

I believe the core thesis remains intact, and Gurus seem to agree.

Here is a great update on Copart’s Q2 2026 results by Lucas | Summit Stocks

Cluster 3 — Guru conviction, market believes these companies are cooked

Constellation Software (CSU)

Constellation is my worst performer in the portfolio.

The stock is down more than 40% over the last 6 months, driven by fear that AI and agentic tools will completely disrupt its niche vertical market software businesses.

The bull case is straightforward: CSU’s portfolio consists of businesses providing sticky, mission-critical systems in industries like emergency dispatch, hospital billing, and agricultural logistics.

In these niches, customers are driven by operational risk aversion, rather than ease of software replication. And if anything, Constellation can use AI to improve their software rather than be disrupted by it.

Constellation will announce quarterly results on 9 March, giving us much-anticipated insight into whether AI is actually affecting the business.

CCC Intelligent Solution

Another victim of the SaaS massacre. CCC provides software for the property and casualty insurance ecosystem.

Their recent earnings were not bad at all, but the fear of AI disruption is real and is hitting the entire sector.

Here is what CEO Githesh Ramamurthy said on the recent earnings call:

In regulated, multiparty industries like insurance, AI increases the need for trusted data, governed workflows, and platforms that can operate safely at scale. As many of you know, CCC has been an AI pioneer and leader for over a decade.

[…] AI is embedded in our products, our support, and our internal operations. While other companies talk about AI in theory, we have been in production at scale for years.

Akre Capital, Peter Keefe, and Triple Frond Partners all significantly increased their CCC position in Q4.

Bryan Lawrence, one of my favorite Gurus covered so far, also increased his position in Guidewire Software (GWRE), which is a partial competitor of CCC in the insurance technology market.

I believe the market is selling all software companies indiscriminately in a kind of “sell first, ask questions later", while some companies (like CCC) have already been AI-first for a while and may actually be a winner long-term.

I am happy to hold CCC for now and will probably add to the position.

PayPal

PayPal stock crashed 20% after disappointing earnings report, but had a bit of a rebound earlier this week after rumors emerged of a possible takeover.

Hopefully a deal materializes at a price close to what I paid…for now, I'm keeping the position.

→ If you enjoy this newsletter, please subscribe and like this post 🤍

→ If you find value here, consider buying me a virtual coffee ☕

👀 Looking ahead and Watchlist update

It’s not just the Guru Gems portfolio that has been hit hard. Some of the best investors are sitting on significant drawdowns too.

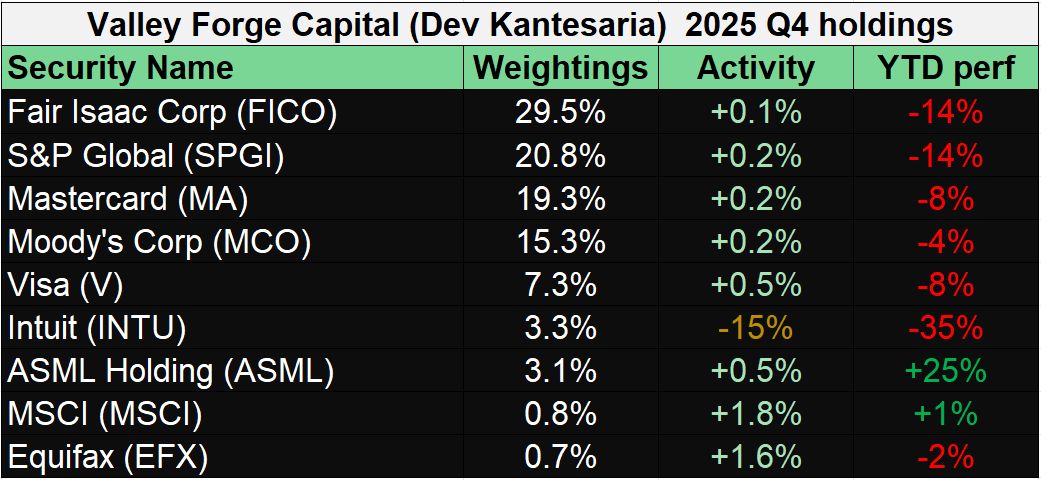

Dev Kantesaria at Valley Forge Capital is a good example.

I’ve covered Kantesaria before: he runs an exceptionally concentrated portfolio of 9 stocks, with over 90% of the fund concentrated in his top five positions: FICO, S&P Global, Mastercard, Moody’s, and Visa. It’s about as high-conviction as it gets, and his long-term track record is excellent.

But February wasn’t kind to him. S&P Global (SPGI), his second-largest position at ~21% of his fund, dropped more than 25% during the first 2 weeks of February. The AI storm was also hitting financial data companies, not just software.

But just like CCC, SPGI may actually be a beneficiary of AI, not a victim of it. The business model is built on selling credibility: credit ratings, benchmark indices, and essential financial data that global markets depend on to function.

If anything, the AI supermachine needs reliable, trusted data to run on and that's exactly what SPGI provides. Case in point: S&P Global has already integrated its Capital IQ datasets directly into Claude, allowing financial professionals to query earnings transcripts, financials, and company intelligence through natural language.

I had already put SPGI on my watchlist after my Kantesaria deep-dive, but after this sell-off, it is now high on the list to make it in the portfolio.

I included my watchlist in the Guru Master Google Doc, so feel free to have a look!

That’s it for this week…thanks for reading and I’ll be back next week with a new Guru deep-dive!