Most Moats Are an Illusion. Physics Tells Us Why

Physics for Investors, Issue 1: The second law of thermodynamics meets Buffett

Welcome to a new edition of Guru Gems, where I study the world’s long-term investing masters and build a portfolio of quality companies based on their wisdom.

In my most recent Guru deep-dive, I covered Josh Tarasoff, a lesser-known Guru, who is not only a brilliant investor but also a great thinker.

Today’s edition is a bit special…

And while it may not be everyone’s cup of tea, I still hope you’ll get something out of it. Please do share your thoughts and suggestions!

2 minute AI audio version of today’s update:

🔭 Introducing a new monthly series

Long before I started studying investing masters and companies’ balance sheets, I had a very different interest: physics.

When I was 17, I got intrigued by reading Stephen Hawkings’ popular book ‘The Universe in a Nutshell’, and it led me to studying physics at university.

After graduating, I went into consulting and never returned to physics professionally. But the fascination certainly remained.

Over the years, I noticed that some of the laws (or principles) that describe moving objects or a cup of coffee cooling on your desk, show up in the world of investing too.

To revive this old passion of mine, I am starting a new regular series at Guru Gems where I bring a single idea from physics and apply it to how we think about businesses and markets.

I promise there won’t be a lot of equations, and the focus will be more on frameworks and mental models.

In keeping with the spirit of Guru Gems, each issue will also feature a guru. Though this time, a guru of physics rather than of investing.

Let’s start with one of the most foundational ideas of all.

The most pessimistic law in science

Of all the laws in physics, the second law of thermodynamics is one of the bleakest.

The first law tells you that energy is conserved. It can’t be created out of thin air or destroyed, only changed from one form to another.

The second law tells you that while the amount of energy stays the same, the useful portion shrinks every time it changes form.

Each time energy is transformed, some of it is "lost" as waste heat, dispersed into a form you can no longer harness. Heat spreads out and hot things cool down.

The arrow of time, as physicists call it, points in one direction only: from order to disorder, from concentration to dispersion.

A famous example is dropping a sugar cube into a hot cup of coffee. Watch what happens. The sugar dissolves. The coffee cools. Both the sugar and the heat spread out evenly, and they never spontaneously go back.

The technical name for this tendency toward disorder is entropy, and it always increases in a closed system.

The British astrophysicist Arthur Eddington wrote in 1928 that entropy holds “the supreme position among the laws of Nature.”

He warned that if your theory is found to be against the second law of thermodynamics, “I can give you no hope; there is nothing for it but to collapse in deepest humiliation.”

Why am I telling you this? Because I believe the second law of thermodynamics also describes the world of business. And once you see it, you cannot unsee it.

🚦Businesses obey the second law too

Imagine the economy as a giant thermodynamic system. In this system, “heat” is excess profit, the returns a business earns above its cost of capital.

And just like heat in a coffee cup, those excess profits do not stay concentrated. They diffuse, competitors arrive, margins compress, customers become choosier, patents expire, brands fade...

The default state of any business, left to itself, is the economic equivalent of room-temperature coffee: returns roughly equal to the cost of capital, no more.

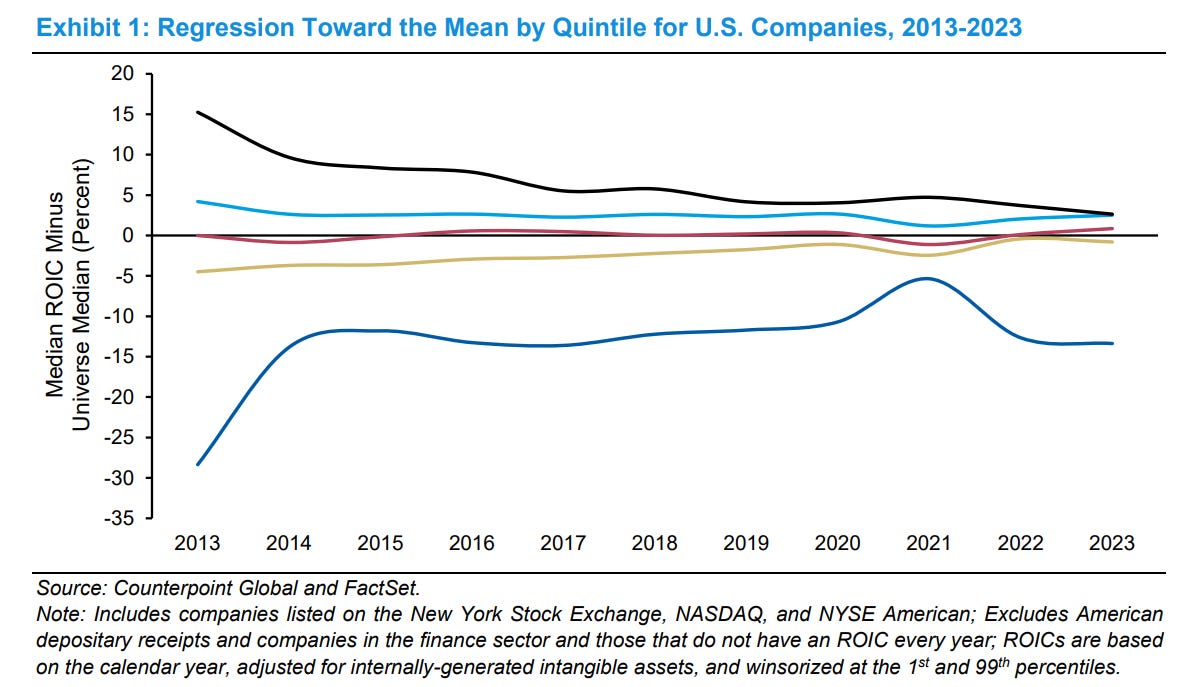

This is not just a metaphor, it is empirically observable. In their landmark 2024 paper Measuring the Moat, Morgan Stanley's Michael Mauboussin and Dan Callahan show that companies earning the highest returns on invested capital tend to see those returns ‘fade’ over the following decade as competition arrives.

This is essentially the second law of thermodynamics applied to ROIC.

High returns attract competitors the way heat attracts cold air. Most businesses, given enough time, regress toward the mean.

So how do some businesses stay hot for decades? The answer in physics is the same as the answer in business: work.

If you enjoy this newsletter, please help others discover it by clicking 🤍

👷 What “work” means in physics, and in business

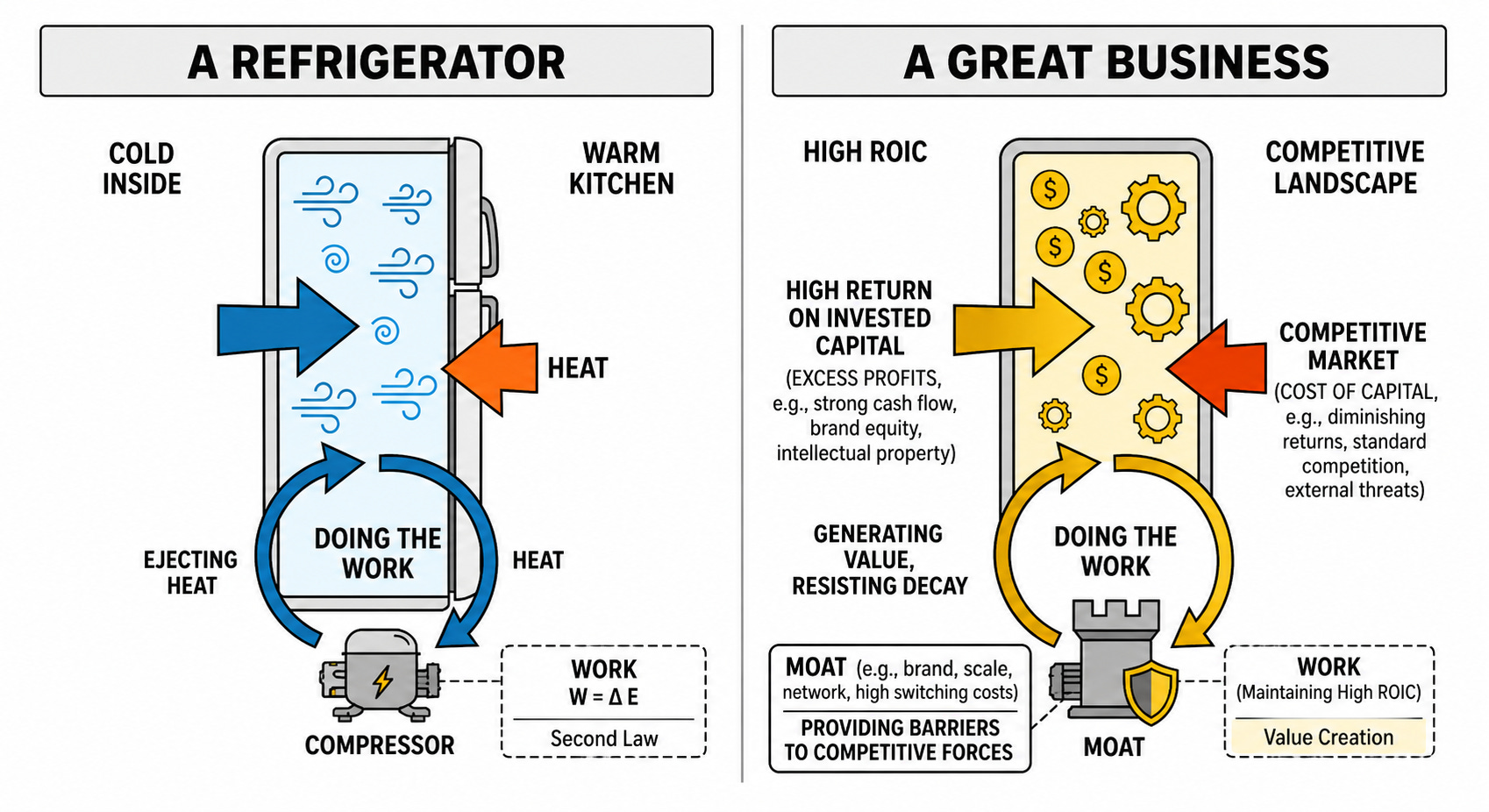

In physics, work has a precise meaning: it is the act of using energy to push a system away from where it naturally wants to go.

A refrigerator is the classic example. The inside of your fridge is colder than your kitchen. Left alone, the cold would leak out and equilibrium would win. So a compressor (the small motorized pump at the back of your fridge) runs continuously, doing the work of pushing heat from the cold inside into the kitchen. Stop the compressor and within hours your milk starts to warm up towards room temperature.

Now think of a great business like a refrigerator.

Here the fridge’s cold air is the company’s excess profits. The warm kitchen is the surrounding economy, pulling everything toward the cost of capital. And something, the moat, is the compressor doing the work to keep the two apart.

Here is where Chris Hohn’s “fortress business model” framework perfectly fits in.

When I wrote about Hohn last month, I described his obsession with barriers to entry. Re-read that issue with thermodynamics in mind, and you realize he is essentially asking: what is doing the work to keep this business away from competitive equilibrium, and how much does that work cost?

Look at the kinds of moats Hohn lists: irreplaceable physical assets, intellectual property too complex to replicate, network effects, switching costs, brand strength, regulatory protection. Each is, in physics terms, a different mechanism for keeping the system far from equilibrium. And the very best businesses use several at once.

As Warren Buffett puts it:

“All economic moats are either widening or narrowing, even though you can’t see it.”

That is the second law at work. A moat cannot stand still. Either work is being done to push it further from equilibrium, or it is silently decaying back toward it.

🧓 The Guru: James Clerk Maxwell (1831–1879)

Before we go further, allow me to introduce the man who played a key role in better understanding the second law of thermodynamics.

James Clerk Maxwell is, in my view, an underrated genius in the history of science.

Einstein kept three portraits on the wall of his study: Newton, Faraday, and Maxwell. When Einstein visited Cambridge in 1922 and was told he had achieved great things by standing on Newton’s shoulders, he replied: “No, I stand on the shoulders of Maxwell.”

A quiet Scottish physicist who died of cancer at just 48, Maxwell unified electricity, magnetism, and light into a single set of equations that still govern every wireless signal, every radio wave, every visible color. If you ever had advanced physics classes, you may have learned about Maxwell’s equations.

Maxwell showed that light itself is an electromagnetic wave, a theoretical breakthrough that lay the foundation for Einstein’s relativity and also made the wireless age possible.

Without Maxwell, no GPS, no Wi-Fi, no mobile phones.

But the work most relevant to investors came from his other great obsession: the behaviour of gases. Maxwell, along with Ludwig Boltzmann, laid the foundations of statistical mechanics, showing how temperature, pressure, and entropy emerge from the collective behaviour of countless jiggling molecules.

🎥 To learn more about Maxwell, the BBC documentary James Clerk Maxwell - The Man Who Changed The World is a wonderful introduction to his life and work.

⭕ Maxwell's demon: a very special type of compressor

In 1867, Maxwell described a thought experiment that would unsettle physicists for the next century.

He pictured a tiny intelligent being (Lord Kelvin would later call it a “demon”) sitting at a gate between two chambers of gas.

Whenever a fast molecule approached from the cold side, the demon opened the gate to let it pass into the hot side. Whenever a slow molecule approached from the hot side, the demon let it pass to the cold side.

Over time, all the fast molecules end up on one side and all the slow ones on the other. The demon has separated hot from cold without doing any apparent work. He has, in effect, broken the second law.

For nearly a hundred years, physicists struggled with this puzzle. The eventual resolution came through information theory: the demon does do work, the work of information processing. He has to observe each molecule, decide what to do, and remember. That information has a thermodynamic cost. You cannot get something for nothing.

But the demon does represent something profound: a system where the work required to maintain order is so cleverly leveraged that it almost looks like magic.

What this means for investors

Maxwell’s demon is obviously just a thought experiment. But it points to something real and important about businesses.

Every great company has a compressor, something doing the work to hold back competitive equilibrium. But the amount of work required varies enormously from one business to another.

The very best businesses look, at first glance, like Maxwell's demons. S&P Global, which I added to the Guru Gems portfolio after my Hohn deep-dive, is a good example. Every bond issuance needs a credit rating. The fee is tiny relative to the bond size, the regulators essentially require it, and S&P collects with almost no incremental work.

Moody's, Visa, and similar Hohn and Kantesaria favourites are variations on the same theme: every transaction, a small toll, with the network running itself. The ratio of work done to heat captured is extraordinary.

At the other end of the spectrum sit businesses where the compressor is real, durable, but loud. GE Aerospace (Hohn) and HEICO (Rochon) earn their returns through continuous R&D, regulatory certifications, and layered switching costs.

And then there are businesses that sit somewhere in between or are still moving along the spectrum. Uber (Ackman) is a good example: billions of dollars were burned over a decade to create a network effect that, now that it has reached critical mass, increasingly runs itself. A demon being built in real time.

The investor's job is to figure out what the compressor looks like that is doing the work to hold back competition. 3 question can help with this.

🏰 Three questions to ask before owning a moat

Knowing where on the spectrum a business sits is only the beginning. To put the second law to practical use, here are three thermodynamic questions worth asking before investing in a company.

1. Is there a compressor and what does it look like? What specifically is doing the work to keep this business above competitive equilibrium? Is it scale? A network effect? A regulatory license? A patent? A brand built over decades? If you cannot name the compressor in one sentence, you probably do not yet understand the business well enough to own it. “They have a moat” is not an answer. What the moat is, and how it does its work, is.

2. What is the work-to-heat ratio? A business that captures enormous heat for very little work (think Visa, Moody’s, S&P Global) is a different animal from a business that captures enormous heat for enormous work (think GE Aerospace, HEICO). Both can be excellent investments. But they require different mental models. The first kind throws off cash and needs little reinvestment. The second kind compounds beautifully but requires constant feeding, and the moment management starts under-investing to flatter quarterly earnings, the compressor might start to fail.

3. Is the kitchen heating up (too much)? A moat that worked in 2010 may not work in 2030, not because the company stopped trying, but because the world around it warmed up. Newspapers did not get lazy; the internet simply raised the temperature beyond what their compressor could handle. The question worth asking of any long-term holding is whether the surrounding environment is becoming hotter or cooler relative to the work the compressor is designed to do.

This last one is also a useful lens on the current AI fears around SPGI. The market is essentially asking whether AI raises the temperature of S&P’s kitchen. My own view, for what it is worth, is that S&P’s particular form of work is proprietary, regulated, embedded in workflows. This is not the kind that AI easily commoditizes. If anything, AI needs S&P’s data to function. But that is a question every investor should evaluate for themselves.

Closing thought

Let’s close with a perfect quote from Buffett, taken from his 2007 letter to shareholders

"A moat that must be continuously rebuilt will eventually be no moat at all."

The truly great businesses are not the ones doing the most work to hold back competition. They are the ones where the work is structurally cheap, where the compressor runs quietly because of the way the system is built, not because of how hard management is pushing.

Most “moats” are not really moats. They are construction sites, perpetually rebuilding. The second law catches up with them eventually.

The investor’s job is to tell the difference. To find the businesses where the work is done by the structure itself, not by the people running it.

That’s it for this week!

As you can see, a bit of a different issue this time but I believe that studying frameworks from the field of science can really help us become better investors.

If you enjoyed this post, I would really appreciate it if you could like or share it or leave a comment!

You can follow me on X @guru_gems and Substack @gurugems for more insights.

Until next week!

Interesting angle, using physics. Maybe you can apply some formulas (or create them) too?

Super interesting read. Well done!