The Lawrence Method, One Year Later & A Closer Look at Guidewire Software (GWRE)

On being wrong 30% of the time, and why I'm buying Guidewire

For those of you that have been following Guru Gems for a while, you know that I am a big fan of the Richer Wiser Happier (RWH) podcast. A few weeks ago, William Green reshared clips from his interview with Bryan Lawrence, and the timing couldn't be better, since it's also the one-year anniversary of my deep-dive on Bryan Lawrence and Oakcliff Capital.

So this week, I revisit Bryan Lawrence one year later: what he said, what he’s been buying, and what he’s building.

I’m also taking a closer look at one of Lawrence’s holdings: Guidewire Software (GWRE)

Here is a 2-minute AI audio version of today’s post:

Guru in the spotlight: Bryan Lawrence

There is a lot to unpack in the below 30-minute clip from William Green’s interview with Bryan Lawrence. It is one of the best 30 minutes you can spend if you want to understand what a real investing process looks like: how ideas get sourced, filtered, researched, sized, and (inevitably) how some of them go wrong.

1. 🎲 The Rule of 3

A recurring theme in the clip is how Lawrence expects to be wrong about 30% of the time.

“If you measure being right as the stock that we bought, either we sold for more than we paid for it, or we own it still for more than we paid for it — we’ve been right 70% of the time and wrong 30%. Like, we’re definitively wrong 30% of the time.”

The last of Oakcliff’s six research questions (more on those below) also builds directly on this:

“Question number six: if we’re wrong — because we can expect to be wrong at least 30% of the time — how much money will we lose?”

Lawrence also points to Buffett’s famous 1984 “Superinvestors of Graham-and-Doddsville” essay: every single one of the Graham-school managers with market-crushing long-term records underperformed roughly a third of the years when measured annually. Lawrence went back and counted for Berkshire itself: 19 of 54 years (i.e. 35% of the time) Berkshire Hathaway stock underperformed the S&P 500.

If this number sounds familiar to Guru Gems readers, it should.

It’s part of François Rochon’s ‘Rule of 3’, which I covered in my Rochon deep-dive:

“One year out of three, the market will go down (by more than 10%). One stock out of three that we will buy will be somewhat disappointing. And one year out of three, we will underperform the indexes.”

Two great investors converging on the same ‘law’ for concentrated stock picking.

2. 😣 The Pain of Underperformance

Knowing you’ll be wrong 30% of the time is one thing. Living through it is another.

Green counted that Lawrence underperformed the S&P in 8 of his 20 years, and still beat the index by more than 100 percentage points cumulatively. Lawrence’s response to how he endures those stretches is really a masterclass in temperament.

An interesting data point he shares comes from DALBAR’s studies of mutual fund flows:

The average active manager underperforms the market by roughly their fees (~1% per year). Painful, but survivable. The real damage is how the clients behave: they add money after strong performance and pull money after weak performance. The result, per DALBAR:

“The client’s returns underperform the active manager’s returns by four percentage points… Four percentage points of underperformance over a 30-year investment horizon leading to someone’s retirement is a nest egg that is 70% less.”

This is quite a statistic. Investors don’t just underperform the market, they underperform their own funds, by a ruinous margin, purely through timing their entries and exits emotionally.

Lawrence adds a nice thought experiment:

“It’s 1975, over the prior 2 years Berkshire Hathaway stock has fallen by half and the market is flat. Do you sell your stock? If you had, that would have been a very bad decision.

It’s 1999, Berkshire Hathaway stock is up slightly but 40 percentage points less than the S&P. Do you sell your stock? That would have been a very bad decision in 1999.”

It’s clear that both would have been really bad decisions. Berkshire has lost half its value three times under Buffett — and underperformed in a third of all years — on its way to one of the greatest compounding record in history.

Which brings me to Terry Smith.

Terry Smith just released his Semi-Annual Letter to shareholders, and it contains the biggest changes in Fundsmith’s 15-year history:

13 names out: Atlas Copco, Coloplast, EssilorLuxottica, Intuit, LVMH, Nike, Novo Nordisk, Zoetis, Unilever, Mettler-Toledo, Otis, Wolters Kluwer, Magnum Ice Cream

12 names in: AppLovin, Netflix, Mastercard, Uber, Veeva Systems, TSMC, GE Vernova, Sage, Legrand, Nextpower, TJX, Yum! Brands

Portfolio turnover in H1 2026: 51%. For a fund whose third commandment is literally “Do nothing”.

The fund was down 2.9% in H1 2026 while the MSCI World rose 11.2%, a 14-point gap in six months, on top of years of lagging a momentum- and AI-driven index.

Fundsmith has suffered massive redemptions, and it looks like this ‘Extreme Makeover’ is either an attempt to stop the bleeding or the result of significant pressure from the remaining investors to make drastic changes.

I have a lot of respect for Smith (he was the Guru of my very first issue!), but this level of change looks very strange and goes against many of Terry Smith’s own principles.

For further reading on Fundsmith’s Extreme Makeover, here are 2 posts which I enjoyed:

René Sellmann - Buy Good Companies, Don’t Overpay, Do EVERYTHING ...

The Compounding Tortoise - Terry Smith’s Radical Strategy Shift

In closing, here is something which I realized is quite ironic: if you ask yourself who is actually living Smith’s famous mantra today...

Buy good companies ✅ Lawrence: natural monopolies, rational duopolies, low-cost operators + only businesses with durable cash flows

Don’t overpay ✅ Lawrence: his 15 holdings traded at ~14x trailing free cash flow at the time of the interview, vs. ~22x for the S&P 500

Do nothing ✅ Lawrence: roughly two new investments per year. “You may see us do nothing for a year.”

Strong performance ✅ Lawrence: while we don’t have the exact performance numbers, based on his reported US holdings, his performance over the past few years must have been very strong

...it looks a lot like Bryan Lawrence is applying Terry Smith’s mantra more than Terry Smith himself.

If you enjoy this newsletter, please help others discover it by clicking 🤍

And if you would like to support my work, consider buying me a virtual coffee ☕

3. 🤖 Meet Marvin and Vicki

The second clip I want to share is Lawrence’s recent presentation at ValueX, and it’s a very different flavor: Lawrence on how he uses AI in the investment process.

Oakcliff has built two AI agents, running on Mac minis:

Vicki is a shop-bot: she hunts for real-estate deals, cars, and restaurant reservations, partly to stress-test Oakcliff investments in areas where agents might disrupt the business model, partly to see what the technology can actually do. Verdict so far: not much. Zillow, Cars.com, OpenTable and friends have all blocked her. The internet has become, in Lawrence’s words, a game of “spy versus spy.”

Marvin is an investment research analyst, and here Oakcliff is having far more success. Marvin applies Oakcliff’s frameworks, monitors the portfolio and watchlist, writes reports, and has a compounding memory base. Lawrence says Marvin can do “weeks of work in seven minutes.”

An interesting insight comes from Marvin himself, commenting on a draft of Lawrence’s presentation:

“My memory compounds correct and incorrect beliefs equally. Human discussion is the quality filter. Without discussion with you, I drift towards confident mediocrity.”

Lawrence’s conclusion: the quality of the agent’s work depends entirely on the quality of the frameworks you feed it. An agent will happily marinate in your biases and amplify them.

“What we’re trying to do with Marvin is have a small number of curated frameworks that maximize a query’s focus on information that is knowable, important, and true.”

There is one more gem in the Q&A that ties directly back to how Lawrence invests. Asked whether AI-driven quant trading changes the game, he lays out the market’s structure: roughly half is indexed, ~40% is algorithmic, and only ~1% is concentrated, long-horizon stock picking.

The algorithms are optimizing for what happens in the next ten days. But gradient descent (the mathematical engine that allows Large Language Models to "learn") doesn’t work when the outcome of a decision is only knowable in two or three years.

Lawrence’s edge (and the edge of everyone practicing this craft) lives precisely in that time horizon the machines can’t optimize for.

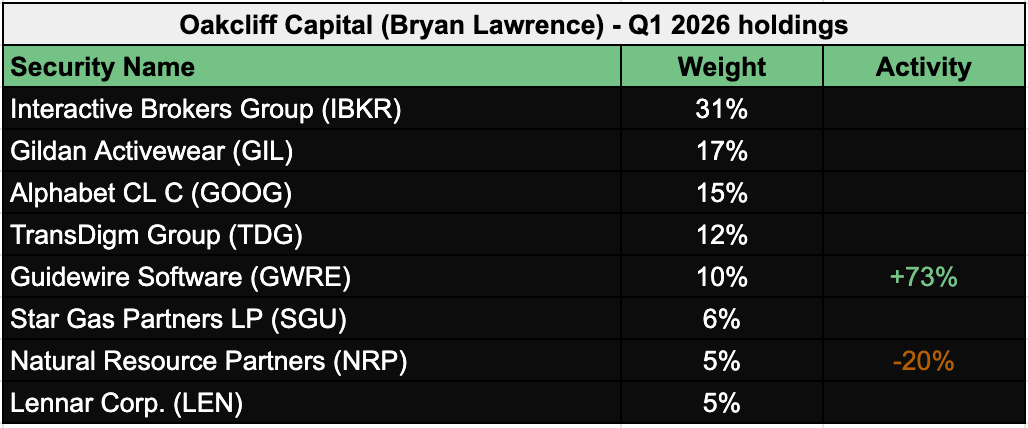

4. 📂 Oakcliff’s Q1 2026 Portfolio

So what does Oakcliff actually own, one year after my original deep-dive?

The answer is: pretty much the same portfolio as a year ago.

Here is the Q1 2026 13F snapshot (as of 31 March 2026, ~$227M in US-listed holdings):

Two things jump out:

Interactive Brokers (IBKR) is now a 30%+ position. IBKR was the Gem of my original Lawrence deep-dive, and it is also one of the larger positions in Marc Werres’s Hinde Group portfolio.

With IBKR up ~200% over the past 2 years, this position has kept compounding in a true “let your winners run” allocation.

Lawrence has been aggressively adding to Guidewire Software (GWRE). He added 73% in Q1 2026 alone, on top of adding 27% in Q4 2025. He’s been buying while the stock has been cut nearly in half from its highs.

A Guru I highly respect backing up the truck on a wide-moat software company during an AI-panic selloff? That sounds like a Gem I need to take a closer look at…

💎 The Gem: Guidewire Software (GWRE) — To Buy or Not to Buy

The setup: Guidewire Software (GWRE) has been caught in the great Software Selloff of 2026. The market has decided AI will eat software, and anything with “SaaS” in its description has been repriced accordingly.

GWRE trades around $136, down ~27% year-to-date and roughly 50% below its 52-week high of ~$273. Lawrence first bought Guidewire in 2020 and has been adding significantly for two quarters.

Let’s run it through the framework.

1/ Is it ‘Good’?

Guidewire provides the core software (the ‘system of record’) for property & casualty (P&C) insurers: ClaimCenter (claims), PolicyCenter (policies), and BillingCenter (billing). This is not a productivity tool an insurer could turn off; it is the operational nervous system of the company.

In the RWH interview, Lawrence shares what defines a good business for him: natural monopoly, rational duopoly, or low-cost operator. Guidewire is the closest thing to a natural monopoly in P&C core systems:

It is the leading provider to the industry, larger by revenue than its next several competitors combined, and wins more deals per year than its largest competitors combined (per Morningstar)

Its software already covers more than 25% of all direct written premiums in the industry

Customer retention is estimated at ~99%, making the duration of customer relationships longer than average within the software industry

Switching costs are enormous: insurers keep core systems for two or three decades. Ripping out the system that processes your claims and policies risks the entire business

In late 2025, Liberty Mutual signed a 10-year, Tier 1 deal that management called "one of the most strategic partnerships in our history"

Morningstar assigns a wide moat, and in March 2026, when Morningstar downgraded six wide-moat software companies (Adobe, Descartes, Manhattan Associates, Salesforce, ServiceNow, and Shopify) over AI disruption concerns, Guidewire kept its wide moat. Its analyst argues that a core system of record for a famously slow-moving, heavily regulated industry is relatively insulated.

Guidewire management also argues that AI is an accelerant: legacy systems from the 1950s can’t deliver AI capabilities, making modernization more urgent, not less.

Finally, the business is executing beautifully through the panic: fiscal Q3 2026 revenue grew 27% YoY to $373M with a 20.9% non-GAAP operating margin, both above the high end of guidance.

This looks like a great business. ✅

2/ Is it ‘Cheap’?

This is the more difficult part. Here are a few elements to help us determine whether GWRE is cheap:

Versus its own history, GWRE has de-rated sharply: the stock fell from a 52-week high of ~$273 to the $120s–130s, compressing EV/ARR from roughly 18x toward ~9x, near multi-year lows despite accelerating ARR* growth.

ARR

In the software and SaaS (Software as a Service) industry, ARR stands for Annual Recurring Revenue. It is a key financial metric that measures the predictable and recurring revenue a company expects to generate from subscriptions over a 12-month period.

EV/ARR

Enterprise Value to Annual Recurring Revenue (EV/ARR) is a commonly used valuation metric in the software and SaaS industry

Morningstar’s fair value estimate for GWRE is $220 per share. At ~$136, the stock trades at a Price/Fair Value of ~0.6, which is one of the largest discounts in their software coverage.

On a current free cash flow (FCF) basis however, Guidewire does not look cheap. GWRE is trading at 33 times FCF, which is on the higher end for a software business and a multiple investors usually pay for expected future cash expansion.

In other words: investors are expecting strong growth and expanding FCF margins driven by the cloud transition.

Verdict: cheap compared to its own history; reasonably priced on the margin-expansion thesis; not cheap on today’s cash flows. ⚠️ ✅

3/ To Buy or Not to Buy

Before I make my final decision, let’s score Guidewire against Lawrence’s own six questions:

Do we understand the business? ✅

Guidewire provides cloud-based core systems and data/analytic solutions to the global property-casualty insurance industry, serving hundreds of insurers in 30+ countries in claims management, policy administration, and billing.

Is it a good business? ✅ ✅

Near-monopoly, ~99% retention, decades-long switching costs, wide moat

Does management think like shareholders? ✅

Consistent execution; Morningstar rates capital allocation Standard; Well thought out acquisitions that complement the portfolio

Is it cheap? ⚠️

~0.6x fair value, but the IRR depends on future margin expansion

Why is it cheap? ✅

Indiscriminate AI-panic selloff vs. an insulated (possibly AI-advantaged) system of record

If we’re wrong, how much do we lose? ⚠️

Hard to assess. If the AI disruption is real, the stock can go much lower still.

📌 Adding Guidewire Software (GWRE) to the Guru Gems portfolio

I plan to add a starter position (1-2%) to the Guru Gems portfolio in the next few days.

This is a good business undergoing a temporary crisis of confidence, with a Guru I highly respect significantly increasing his position.

Since I expect to be wrong 30% of the time, and if the AI bears turn out to be right about even core systems software, there is still real downside from here. So position sizing will be key and hence a small starter position.

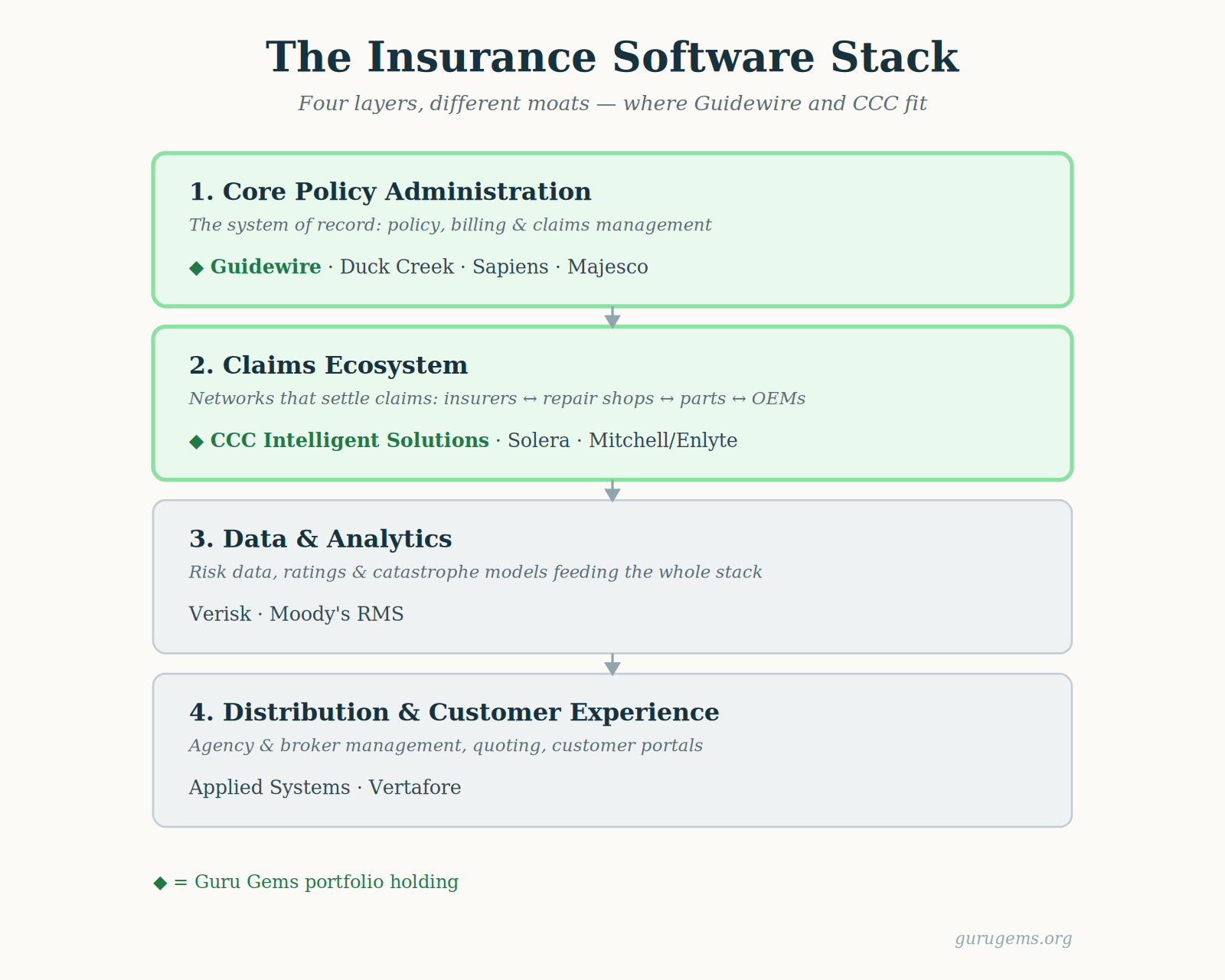

🧩 One More Thing: Guidewire Meets CCC

Regular readers will remember that I already own CCC Intelligent Solutions (CCC) in the Guru Gems portfolio: another insurance software name held by several Gurus. So am I doubling up on the same bet?

No, and it could be helpful to get a basic understanding of the four layers of the insurance software stack.

Guidewire and CCC sit in different layers. Guidewire is the operational backbone an insurer uses to issue policies and manage the claim file; CCC is the specialized auto-claims network the claim gets routed through.

A single auto insurer commonly runs ClaimCenter as its system of record and pushes the physical-damage workflow through CCC. They don’t bid against each other.

So rather than doubling the same bet, I now own two dominant, ~99%-retention franchises in two different layers of the stack: the core (Guidewire) and the claims network (CCC). Both have been de-rated by the same indiscriminate software selloff. Same storm, different moats.

That’s it for this week’s edition!

Thank you for reading and following along.

Until next week!

✅ Further Reading

This week’s issue connects across the Guru Gems archive:

Bryan Lawrence & IBKR: the original deep-dive, one year old this week.

Timeless Lessons from François Rochon: the Rule of 3, the Podium of Errors, and why patience is the rarest quality.

Cloning the World’s Best Investors: my very first Guru Gems issue. Here I introduced Terry Smith’s framework.

Marc Werres & The Hinde Way: Marc Werres, the other guru with a massive IBKR conviction position.

Physics for Investors #2: on feedback loops