Adding a new Gem & 2 Things I learned this week - 10 May 2026

Lessons from Paul Tudor Jones, Christopher Tsai, and a wide-moat compounder on sale

Welcome back!

Today I’m sharing my thoughts on 2 interesting pieces I came across this week. I also started a small position in a new company.

This company reported Q1 2026 earnings on Thursday and the stock dropped more than 20% in a single day after missing expectations and cutting full-year guidance. Both Terry Smith (Fundsmith) and David Rolfe (Wedgewood Partners) are shareholders, and after a drop of this magnitude, I think it’s worth a serious look.

Last week I started a new regular series where I bring a single idea from physics and apply it to how we think about businesses and markets. Make sure to check it out and tell me what you think!

Here is the 2 minute AI audio version of today’s post if you are short on time:

1️⃣ Paul Tudor Jones: “Buffett is the OG of compound interest”

Paul Tudor Jones is one of the most legendary traders alive. Famous for predicting the 1987 Black Monday crash, Paul Tudor Jones (‘PTJ’) is a pioneer in global macro trading, often focusing on currency and interest rate fluctuations.

He is also the founder of the Robin Hood Foundation and runs a fund that has delivered significant returns while having roughly zero correlation to the S&P 500 over four decades.

He recently sat down with Patrick O’Shaughnessy on the ‘Invest Like the Best’ podcast for a wide-ranging conversation.

The whole interview is worth watching, but a few moments stood out.

PTJ’s respect for the GOAT

For decades, PTJ used to “rail on Warren Buffett year after year after year”, dismissing him as a guy who just happened to be in the right place at the right time during the great American bull market.

And while he envies the ‘belief system’ on which Buffett’s approach was based, he realized that he didn’t have Buffett’s calm, patience and fortitude to sit through a significant market drawdown and do what Buffett does. He jokingly says:

“Why couldn’t I be Warren Buffett? Just believe in America. When you’re down 50%, who cares? America’s going to bring you through.”

But after listening to an ‘Acquired’ podcast on Berkshire Hathaway, something clicked:

“For the first time I learned that at 9 years old, 9 years old, he understood the power of compound interest. And actually when I listened to that podcast, I just went, Oh my god, this guy is a genius and I have been the biggest fool.”

And he closes with his characteristic humor:

“Warren, if you happen to hear this, I’m deeply apologetic. You are the OG of compound interest, and I wish I was one-tenth as smart as you are.”

For someone running a strategy with 0.12 negative correlation to the S&P 500 for 40 years, this is a great acknowledgment of the power of the approach I study here at Guru Gems: owning great businesses and letting them compound.

Trading as boxing

When the interviewer asked PTJ to describe what trading actually feels like, he uses a boxing analogy:

“You’re going into the ring with this opponent who’s after you the whole time. You’re pairing, jabbing, feeling each other out, looking for an opening. And then every now and then you’ll have a great opening and you take a big shot. And you may land one.”

A few examples from his career:

Bitcoin in 2020 (a ‘knock-out’): When central banks and treasuries were intervening at unprecedented scale, he saw Bitcoin as the best inflation hedge available

Two-year rates in 2022 (also a ‘knock-out’): As inflation surged, PTJ believed the Federal Reserve would be forced to aggressively tighten policy, leading him to bet against the short end of the yield curve.

Dollar/yen today: He believes the yen is grossly undervalued and with Japan’s first dynamic prime minister in half a century, he sees a yen ready to repeat what happened to the dollar under Reagan and the pound under Thatcher.

The pattern he looks for: under-owned, undervalued, way out of whack, plus a catalyst.

Are we 1999 again?

The most interesting part of the interview for me was PTJ’s view on today’s market. He went through the big moments of his career: 1987, 1998, 2000, the GFC, and noted most of them shared a common feature: too much leverage, often derivative-driven.

But 2000 was different, and that’s the one that today’s market reminds him of:

“2000 was the easiest bear market I’ve ever seen my whole life. It’s got so many similarities to right now in the sense that the bear market of 2001 and 2002 were a consequence of all the IPOs in ‘99-2000 and then as they unlocked you just had this never-ending cascade of selling.”

His worry today is based on a simple piece of math:

For the past 10 years, S&P 500 buybacks have retired 2-3% of market cap every year.

Planned IPOs over the next year are estimated at 5-6% of market cap.

Hyperscalers’ massive AI capex commitments are eating into the cash flow available for buybacks.

In other words, the equity supply/demand balance is about to flip: new equity supply rising while retired equity supply shrinks. Add the unlock schedules from a wave of IPOs and you have the same setup that produced the 2001-2002 bear market.

The lesson for me

I’m not going to start trading the dollar/yen anytime soon (although it may be a great time to look for undervalued Japanese stocks). But two things from this interview that I think are worth remembering:

Even legendary traders eventually recognize the value of compounding. PTJ’s career has been spectacular, but his honest reflection is that Buffett’s “boring” approach has been mathematically superior. That’s a powerful endorsement of what we try to do here.

Be aware of the supply/demand math for equities. With the IPO pipeline filling up and buybacks under pressure from AI capex, this is something worth watching, even for long-term investors.

→ If you enjoy this newsletter, please subscribe and help others discover it by clicking 🤍

→ If you find value here, consider buying me a virtual coffee ☕

In my latest deep-dive I covered Josh Tarasoff, a lesser-known Guru who is not only a brilliant investor but also a great thinker

2️⃣ Christopher Tsai: Value Investing 4.0

Last year I covered Christopher Tsai of Tsai Capital, who runs a quality-growth strategy with a portfolio of long-term compounders like Apple, Brookfield, Amazon and Markel.

Tesla is Tsai’s largest position, and while I struggle to see Tesla as an attractive investment at its current valuation, the stock went more than 5x since Tsai started buying it in 2020.

Tsai just published an essay titled “Value Investing and the Emerging 4.0”, which is an interesting framework for thinking about how the discipline of value investing has evolved over the past century.

He breaks it into four eras:

Value Investing 1.0 — Graham’s “cigar butts” (~1930s)

Buying assets at a steep discount to book value, or even net current asset value… for less than two-thirds of [a company’s] net liquid assets alone — getting the plant, property, and equipment for free.

Value here was immediate: it resided entirely in the company’s balance sheet. This worked brilliantly in a manufacturing-heavy world full of forced liquidations, but Tsai argues most investors are still mentally trapped here, fixating on a single year of earnings rather than long-term earnings power.

If you want to learn more about Benjamin Graham and his book ‘The Intelligent Investor’, make sure to check my deep-dive:

Value Investing 2.0 — Buffett & Munger’s “wonderful companies” (~1970s onwards)

Value Investing 2.0 is best expressed by Buffett’s famous shift: “It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.”

Value here became the present value of discounted future cash flows, projected meaningfully into the future. Margin of safety still applies, but it’s calculated against intrinsic value, not against book value.

Value Investing 3.0 — “The Medium is the Moat” (today)

This is Tsai’s preferred lens for evaluating great growth companies. Borrowing from Marshall McLuhan, he argues the new moat isn’t the product, but rather the environment built around the product:

Leading companies don’t merely sell products or services; they architect entire digital infrastructures and economic castles that redefine how we live, work, and interact — often invisibly.

Within 3.0, he highlights a particularly powerful subset: scale-economies-shared businesses, and (building on Nick Sleep’s foundational work) makes a distinction between:

Supply-side scale economies (positive marginal cost): companies like Amazon, Tesla, and SpaceX that pass scale benefits back as lower prices, igniting a flywheel of more customers → more scale → lower prices

Demand-side scale economies (zero marginal cost): platforms like YouTube, Instagram, and Google Search where the price is already free, so the company instead competes on user experience. Tsai coins a term for this: “Engagement Value per Unit Time”

In both cases, the company builds latent pricing power that it deliberately chooses not to flex, which means surface-level multiples often understate true intrinsic value.

Value Investing 4.0 — Intelligence as the castle (emerging)

In Tsai’s Value Investing 4.0, the company doesn’t just operate on top of an established platform. It must first build the platform itself, and the platform is intelligence.

In Value Investing 4.0, the economic castle is intelligence itself. And for the first time, the primary output that consumers are buying is digital labor.

Because the upfront capital required is enormous, Tsai argues that true 4.0 businesses don’t yet exist as standalone public companies. The closest examples are subsidiaries inside profitable 3.0 companies that can fund the bets:

Tesla (Dojo + FSD + Optimus) - Funded by profitable car and energy businesses

Frontier AI labs (Anthropic, OpenAI, xAI) - Funded by large 3.0 technology companies

Valuing a 4.0 business requires “an even more probabilistic, optionality-rich mindset”, projecting not five- or ten-year cash flows, but the present value of capabilities that may reshape entire industries.

My thoughts

I have to admit that Tesla is where the 4.0 lens gets hardest for me to apply. Paying today’s valuation for an “optionality-rich future” that may or may not arrive requires more conviction than I currently have, and I suspect many readers feel the same.

It doesn’t invalidate the framework. What I like is that the framework explains why the most successful quality-growth investors of the past decade have leaned into businesses that look “expensive” on a 1.0 or 2.0 basis but are deeply undervalued through a 3.0 lens.

Tsai’s 4.0 lens is certainly interesting food for thought…

💎 New Gem: Zoetis (ZTS) — A wide-moat compounder on sale?

Now to this week’s main event.

Zoetis reported earnings on Thursday and the stock dropped 21%, its largest single-day decline as a public company.

Two very disciplined quality investors, Terry Smith at Fundsmith and David Rolfe at Wedgewood Partners, have been building positions in Zoetis since early 2025.

When two great investors land independently on the same business and the price drops 20%+ in a day, that deserves a very close look.

Let’s evaluate Zoetis through our Terry Smith-inspired framework.

What does Zoetis do?

Zoetis is the global leader in animal health. Spun off from Pfizer in 2013, the company sells medicines, vaccines, diagnostics, and genetic tests for both companion animals (dogs, cats, horses) and livestock (cattle, swine, poultry, fish).

The mix is roughly 70% companion animals / 30% livestock, with the U.S. accounting for ~55% of revenue and operations in more than 100 countries.

1/ Buy good companies

✅ Wide moat in an attractive industry. Morningstar rates Zoetis as having one of the widest moats in animal health: 300+ products across 8 species, 17 therapies generating over $100M each annually, long product lifecycles (less generic pressure than human pharma), and decades-deep veterinary relationships.

✅ Powerful secular tailwinds. The global animal health market is forecast to grow at ~8-10% CAGR (~$70B in 2025 → $150B by 2032), driven by the humanisation of pets, rising emerging-market pet ownership, pets living longer, and growing global demand for animal protein.

✅ Strong financials and capital allocation. 5yr ROCE of 26%, net margin of 28%, ~15% annualised dividend growth, and an active buyback program which was recently increased.

⚠️ What the market hated this quarter. The Q1 weakness was concentrated in one segment: U.S. companion animal. Total revenue grew just 1.9% to $2.26B (a miss); U.S. business declined 8% (companion animal alone -11%); but International grew 10% and livestock grew 12%. CEO Kristin Peck cited “a more price-sensitive and competitive environment” and lowered FY26 guidance accordingly.

2/ Don’t overpay

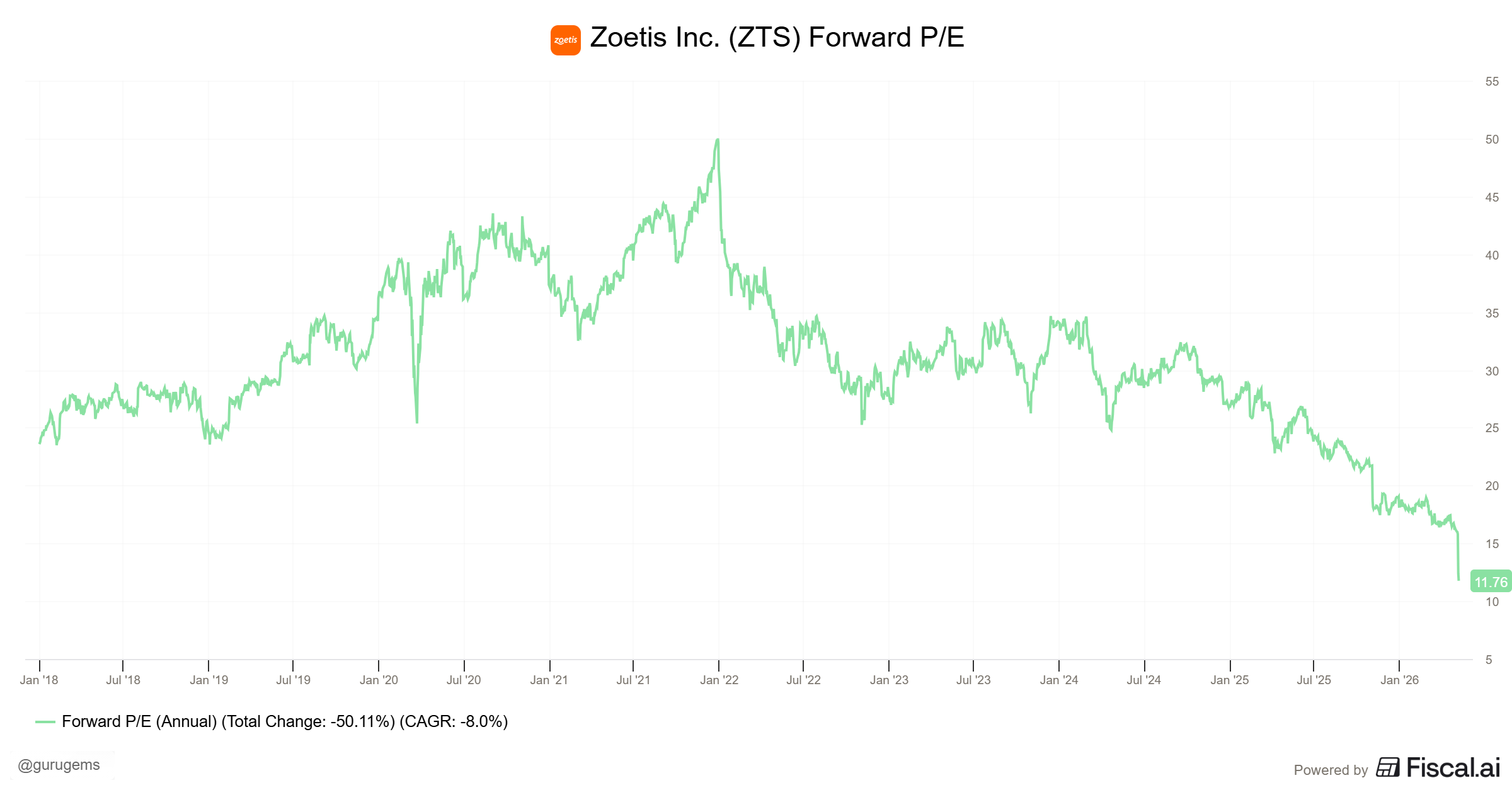

Here is where it gets interesting. Zoetis has historically been a “premium” stock. But after Thursday’s drop, ZTS trades at ~12x forward earnings, a historically low valuation.

With a 5yr ROCE of 26% and a EV/EBIT multiple of 12, Zoetis is now entering ‘Magic Formula’ territory…

Here is what David Rolfe wrote in his Q2 2025 letter, when the stock was much higher than today:

“We believe that, over the long term, reality tends to win; high-quality businesses earn the valuations they deserve at some point and will outperform the broad market. We believe we have been given the opportunity to do this with Zoetis now.”

3/ Final decision

Zoetis looks like a great Guru Gems portfolio candidate: a wide-moat business, in a structurally growing market, owned by two very disciplined quality investors I follow, and now trading at the cheapest valuation in a decade.

The Q1 results are genuinely disappointing, but the weakness is concentrated in one segment where the issues appear cyclical and competitive rather than structural. International and livestock continue to grow, and the long-term tailwinds for animal health are intact.

As Howard Marks often points out:

“In the real world things fluctuate between ‘pretty good’ and ‘not so hot’, but in the minds of investors they go from ‘flawless’ to ‘hopeless’, and so prices fluctuate enormously around intrinsic value.”

This feels like one of those moments.

📌Adding Zoetis (ZTS) to the Guru Gems portfolio.

I plan to add a starter position (1-2%) to the Guru Gems portfolio in the next few days and may buy more if the price continues to fall.

That’s it for this week! Please like or share if you find these insights valuable.

You can follow me on X @guru_gems and Substack @gurugems for more insights.

Until next week!