A Hidden Master: Marc Werres & The Hinde Way

Gem in the spotlight: Interactive Brokers - The ultimate Compounder

In today’s edition:

🕴️ The Guru: Marc Werres — founder of Hinde Group, one of the best investors you’ve probably never heard of

🏛 The Playbook: The Hinde Way — The 5 Pillars of a great business

📺 The Playbook in action: A Netflix case study (a 4× return in under four years)

💎 The Gem: Interactive Brokers Group (IBKR) — Werres’s decade-long compounder

2-minute AI audio version of today’s post:

Guru in the spotlight: Marc Werres

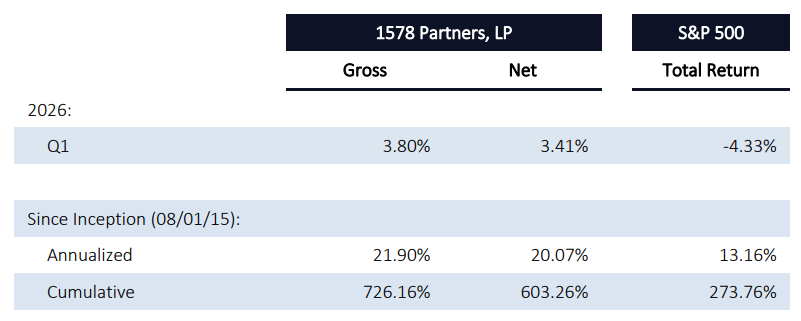

Marc Werres is the founder and Managing Partner of Hinde Group, a San Francisco–based investment firm he launched in August 2015.

His performance over the past decade has been outstanding. Since inception in 2015 through the end of Q1 2026, the portfolio has compounded at ~20% net per year, significantly outperforming the S&P 500’s ~13% return.

He has done this with a concentrated portfolio of less than ten names, no leverage, and through periods where he held meaningful cash when nothing looked attractive.

I came across Hinde Group thanks to a reader recommendation, and the more I read, the more convinced I became that this is a ‘hidden master’ worth highlighting.

Like other great investors, Werres focuses on the long horizon. Hinde holds many positions for years (some since inception) and places almost no weight on short-term benchmarks.

The team’s information edge comes from deep primary research and alternative data, but above all it is the investment discipline characterized by concentration, patience, and strict quality filters that defines the ‘Hinde Way’.

If you enjoy this newsletter, please help others discover it by clicking 🤍

And if you learned something useful, consider buying me a virtual coffee ☕

The Hinde Way

Hinde Group’s investment approach is built on a small number of clear principles.

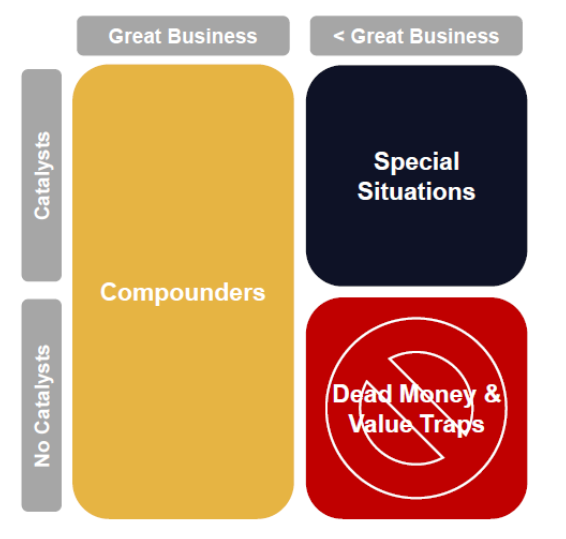

1️⃣ Two categories: Compounders & Special Situations

Hinde Group’s investments fall into two categories:

🟡 Compounders are great businesses that are out-of-favor, misunderstood, or underappreciated. The intended holding period is indefinite. Most positions get held for many years.

⚫ Special Situations are less-than-great businesses trading at a meaningful discount to intrinsic value, where a specific catalyst like a spin-off, merger, restructuring, or litigation outcome, is expected to close that gap within two years.

That’s the entire universe. Just compounders to own (most of the portfolio) and special situations to harvest (smaller part of the portfolio).

2️⃣ The 5 pillars of a great business

According to Marc Werres, a great business has all five of the following characteristics

🏰 1. Meaningful & Durable Market Power

Great businesses are those that create large amounts of value for their owners over time. One of the essential elements to achieving that, is meaningful and durable market power.

These businesses are characterized by pricing power, high returns on investment (ROE of 15–20%+), and barriers to entry that protect those returns from competition over the long term.

Pricing power and barriers to entry are also at the core of Chris Hohn’s investment framework:

🔮 2. Predictable Performance

It is hard to overstate how unpredictable the future is. Precisely forecasting the performance of any business over an extended period of time is a fool’s errand.

[…] But it is more reasonable to make such forecasts for some companies than it is for others.

Some companies have certain characteristics that make their performance relatively predictable: a stable market demand, recurring revenue, long product cycles, diverse sources of demand, limited dependencies, flexible operations, high profit margins and conservative financing.

The point is not to forecast quarterly EPS but to be confident that the business will look meaningfully bigger and more profitable in 5–10 years.

Predictability is also the #1 criteria Dev Kantesaria looks for in a business:

🚀 3. Abundant Growth Opportunities

Great businesses have abundant growth opportunities from multiple sources that should allow them to grow earnings per share at a compound annual rate in the high single digits or more over the next decade.

While there are different ways a business can grow (Improving existing products, enhancing pricing effectiveness, reducing costs … ), the most noteworthy way is to develop new products and services, which when done successfully “can create abundant growth opportunities for decades.”

Hinde looks for systematic innovation: maintaining a ‘stock and flow’ of products and services across Core, Emerging, and Viable horizons.

Amazon is a prime example of a company whose ability to successfully develop new products and services seems to provide it a nearly limitless source of growth.

🧠 4. Talented, Honest & Driven Leaders

Leaders who embrace reality, move fast, advocate simplicity, and obsess over attracting top talent. Similar to what I have seen with many other Gurus, they look for owner-operators whose incentives are aligned with long-term shareholders.

🔥 5. A Cult-Like Corporate Culture

Great businesses have cult-like corporate cultures that play an essential role in their success. Those cult-like corporate cultures share three fundamental characteristics:

Clear & Compelling Vision

Permeating & Guiding Ideology

Zealot Employees

You can read more about each of these pillars on Hinde Group’s website.

3️⃣ Concentration with a margin of safety

Hinde Group typically holds about 10 positions or less.

This is a deliberate concentration that focuses capital on their best ideas. At the end of Q1 2026 the portfolio was just seven long positions plus cash.

At the same time, they insists on a margin of safety for every position: a discount relative to a conservative appraisal of intrinsic value. The combination of high concentration and high selectivity is the engine.

We do not need every investment to be successful for the overall portfolio to deliver exceptional results. We only need to limit unsuccessful investments in number and magnitude. Hinde Group’s investment process is designed to target a 90% success rate over time and to ensure unsuccessful investments are not disasters. Even if everything is working exactly as planned, 1 in 10 of our investments will fall short of our 15% hurdle rate when all is said and done.

At the same time, just because we expect to have some unsuccessful investments does not mean that we should just brush them off when they occur. One of Hinde Group’s principles is ‘Own the Outcome’. Putting that principle into practice means recognizing unsuccessful investments when they occur, critically examining what mistakes may have been made, and learning whatever we can from the experience.

🎬 The Hinde Playbook in Action: Netflix (2022–2026)

Before we get to the current portfolio, I want to take a brief detour through what I believe is a brilliant illustration of The Hinde Way.

Werres has a favorite Warren Buffett quote:

“A great investment opportunity occurs when a marvelous business encounters a one-time huge, but solvable problem.”

Netflix in early 2022 was, in Werres’s words, an “archetypal example” of that pattern.

Act 1: Building a position into a 75% drawdown

Hinde began building its NFLX position in Q1 2022, when the stock had fallen sharply from its November 2021 high. They kept adding right through the brutal April 2022 earnings crash that ultimately took the stock to nearly 75% off that all-time high.

The investment community had largely written Netflix off after just a couple of quarters of softer membership growth.

Werres ran Netflix through the 5-pillar framework and concluded it was the rare company that scored well on all of them: meaningful and durable global-scale market power; predictable, low-churn subscription revenue; a vast unpenetrated TAM (only ~6–7% of US TV viewing time, even in its most established market); an elite founder-led management team in Reed Hastings and Ted Sarandos; and a famously cult-like corporate culture.

Some of the challenges that were feared by the market he saw as solvable.

A key signal for Werres was also the fact that Reed Hastings personally bought $20 million of stock in the open market at roughly the same time Hinde was building its position.

Act 2: A strong contrast with Bill Ackman

Werres was not the only great investor who saw Netflix in early 2022 as a “marvelous business with a one-time, solvable problem.”

Bill Ackman saw exactly the same setup.

In January 2022, at almost the same moment Werres was building his Hinde position, Pershing Square put over $1.1 billion into Netflix at similar prices, for almost identical reasons.

Then came the April 2022 earnings report.

Netflix announced it had lost 200,000 subscribers (its first decline in over a decade) and forecast a steeper drop ahead. The stock crashed more than 25% in a single day.

Ackman sold the entire position the very same day, locking in a ~$400 million loss after just three months of ownership.

I covered this full episode in Bill Ackman & The Pershing Square Playbook 👇

As I highlighted in my Ackman post, being “right” about the quality of a business clearly doesn’t help if you sell too soon.

[Quick sidenote: it looks like Bill Ackman and Marc Werres have a very similar investment framework since quite a few names have appeared in both investors’ portfolios at similar times: Netflix, Alphabet, Amazon, Uber, …]

Final act: The payoff

The stock fell further in 2022 before having one of the greatest recoveries of the decade.

By early 2025, NFLX had climbed above $1,000 and became Hinde’s second-largest position at just under 18% of the portfolio.

And this is when Werres started reducing his position:

“Netflix remains a great business with a bright future, but its stock clearly offers a notably lower prospective return above $1,000 than it did below $300.”

Hinde began trimming at the start of 2025, and by the end of Q2 the position was down to just ~2% of the portfolio.

Over a 41-month holding period, the Netflix investment delivered a 62.7% IRR and a 4.1x MOIC (Multiple on Invested Capital, i.e., Hinde got 4.1× their money back).

Bought when the business was great but the market was terrified. Held while the thesis was proven out. And trimmed when the prospective return no longer cleared the hurdle.

Perfect execution…

The sequel: Act 1, Take 2

As I was finishing this piece, Hinde Group released its Q1 2026 letter and Werres has started buying Netflix again.

NFLX is now down more than 30% from its June 2025 high, weighed down by AI-related disruption fears and the company’s failed bid to acquire Warner Bros. Discovery.

The Q1 2026 letter confirms that Werres used the weakness to increase both his Netflix and Amazon positions.

He is not alone. As I covered last week in What Gurus are buying and selling — Q1 2026 13F updates, several other long-term Gurus were also adding to Netflix during the quarter:

Josh Tarasoff initiated a new ~8% position

Thomas Russo added +12%

Bill Nygren significantly increased Oakmark’s stake

The shared thesis is that Netflix is entering a new phase of pricing power and margin expansion, with or without transformative M&A.

In other words, we are watching the Hinde playbook run a second time on the same business with the same framework, but as a new opportunity.

The Hinde Group Portfolio

At the end of Q1 2026, the Hinde portfolio consisted of just seven long equity positions and ~10% cash.

There are no exact weightings available of the positions, but from the letters we can get a pretty good idea of what the portfolio looks like:

Interactive Brokers Group (IBKR), Uber Technologies (UBER), Northeast Bank (NBN), Alphabet (GOOG)

At the start of 2025 these 4 companies accounted for most of the portfolio’s equities

Werres mentioned some trimming and adding during 2025, but it looks like these are still significant positions in the current portfolio

In the Q1 2026 letter, Werres mentions that IBKR “still represents a mid-teens percentage of the portfolio’s value”

Amazon.com (AMZN), Netflix (NFLX)

Positions that had been trimmed during 2025

Werres has been adding again to both names in Q1 2026

Becton, Dickinson and Company (BDX)

BDX is a ‘special situation’ stock added in Q3 2025

It was their first new position since 2022.

Three observations from this portfolio:

1/ Having the patience to wait for 2 years before buying something new, reminds me of Norbert Lou’s Punch Card mindset:

2/ Several names overlap with the Guru Gems portfolio (GOOG, UBER, AMZN), which is obviously a great validation of what I have done so far :)

3/ Finally, the portfolio’s evolution over the past decade is also quite fascinating.

Werres bought IBKR at inception in 2015.

He added Alphabet in 2017 and UBER in 2020.

He initiated Netflix during the 2022 valuation collapse and harvested most of it in 2025.

Werres is comfortable holding meaningful cash when attractive opportunities are scarce. In Q1 2017, after some big wins, cash was nearly at 48% of the portfolio.

In summary: The discipline is to ride winners while constantly hunting for the next mispriced great business or special situation and having the patience to wait if nothing good shows up.

💎 The Gem: Interactive Brokers Group (IBKR)

Werres has owned IBKR since Hinde Group’s first day. The position has delivered a ~27% compound annual return over more than a decade.

IBKR is the position he keeps returning to in his letters, and IBKR was the largest single contributor to Hinde’s 2025 performance.

So if there is one Gem worth studying from this portfolio, this is this one.

A brief callback: Bryan Lawrence

Long-time readers may remember that I touched on IBKR last summer in The Lawrence Method, where Bryan Lawrence’s Oakcliff Capital held it as their largest position at over 22% of portfolio (now 30%).

Lawrence’s four-question framework gave IBKR a green check on three of four boxes (Business We Understand, Good Business with Durable Cash Flows, Shareholder-Aligned Management) and a question mark on valuation.

When I wrote about Lawrence in July 2025, I concluded that while IBKR looks like a high quality business, I should do a bit more research on this company, and that’s exactly what I did when researching for today’s Guru Gem.

What does Interactive Brokers actually do?

IBKR is a highly automated global electronic brokerage firm founded by Thomas Peterffy. It provides ultra-low-cost trading across stocks, options, futures, FX and other assets in 150+ markets.

Key customers are primarily professional traders, hedge funds, and financial advisors, but also include active retail traders.

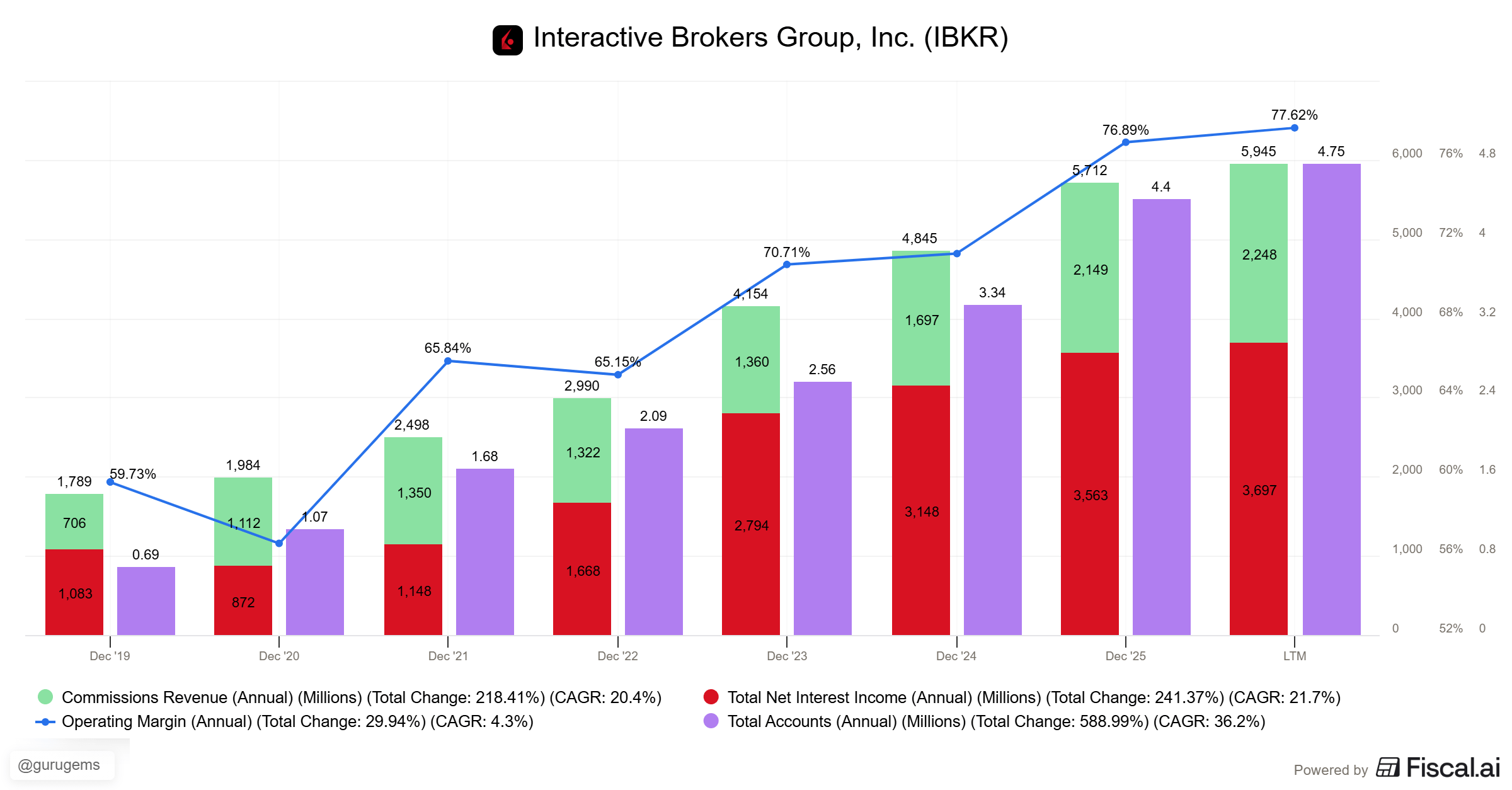

The business has two main revenue streams:

Commissions earned on trades. In 2025, commission revenue grew 26%.

Net interest income earned on customer credit balances and margin loans. In 2025, this grew 13% despite multiple Fed rate cuts, because customer credit balances grew 28% and margin loans grew 31%.

IBKR’s Q1 2026 results show how impressive this business really is:

$1.7 billion in net revenue (+17% YoY)

$1.3 billion in pre-tax income (+22% YoY)

77% pre-tax margin (highest profit margin in the industry)

4.8 million customer accounts (+31%)

$789 billion in client equity (+38%)

Why IBKR is a ‘great business’ by Hinde’s 5-pillar framework

🏰 1. Meaningful & Durable Market Power ✅

IBKR’s automation-first cost structure lets it offer what Werres calls “the least expensive brokerage services while maintaining the highest profit margins in the industry.”

In his Q3 2019 letter he highlighted that IBKR was charging 3.40% on a $25,000 margin loan while Schwab and Fidelity each charged 8.82% for the same loan. Today, per IBKR’s Q1 2026 investor materials, US margin rates are 4-5% for IBKR Pro, still well below larger retail brokers.

When Schwab and TD Ameritrade went to zero-commission in late 2019, Werres argued in that same letter that while this would hit some online brokers hard, IBKR would be “relatively unscathed”, which turned out to be a correct analysis.

🔮 2. Predictable Performance ✅

IBKR’s ‘Total Customer Equity’ has grown at a 25% annualized rate over the last decade, proving its intrinsic value grows regardless of the macro environment.

This is the metric Werres started emphasizing in his 2023 letters because it captures intrinsic value growth without the noise of interest rates and trading volumes.

Customer accounts have grown alongside it at a similar high pace.

🚀 3. Abundant Growth Opportunities ✅

IBKR has penetrated less than 1% of its addressable market.

Growth levers include introducing-broker partnerships (the “white-label” model that fueled Asian growth), new geographies and new products (crypto, prediction markets via ForecastEx, overnight trading, mutual funds, bonds, event contracts).

🧠 4. Talented, Honest & Driven Leaders ✅

Founder Thomas Peterffy is still chairman, still owns roughly 73% of the underlying LLC, and still drives the company. Senior management is dominated by software engineers, not bankers. And the company emphasizes long-term growth over short-term metrics.

🔥 5. A Cult-Like Corporate Culture: ✅

The mission has not changed since 1977:

“Create technology to provide liquidity on better terms. Compete on price, speed, size, diversity of global products and advanced trading tools.”

Every product decision like the recent push into prediction markets and AI tools, runs through that same lens. This is the kind of cultural continuity that tends to survive the founder.

Five out of five… looks like we found ourselves a ‘good’ business :)

To Buy or Not to Buy

Now that we’ve established that IBKR is a great business, let’s look at the valuation

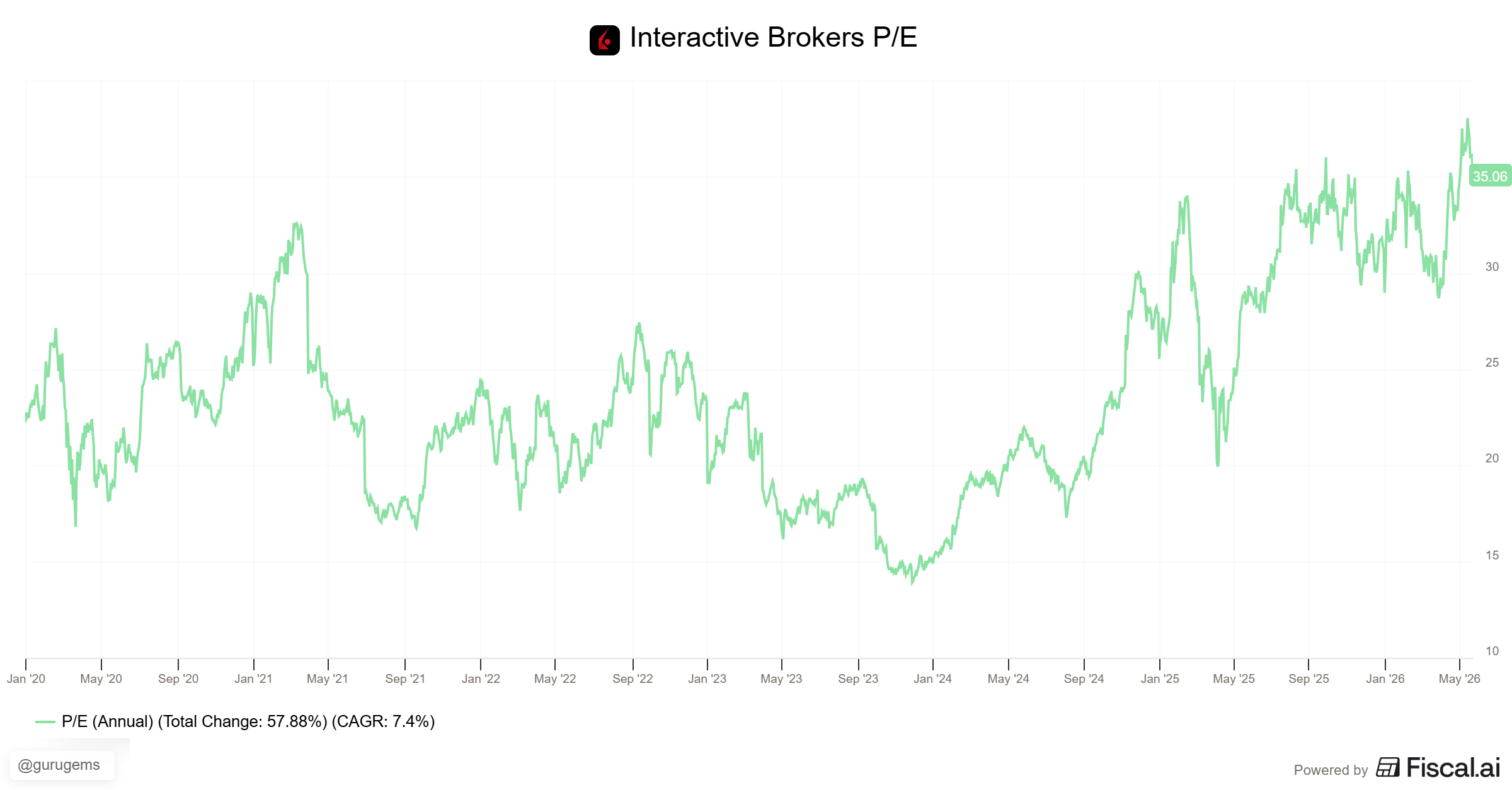

IBKR was up 113% in 2024, 46% in 2025 and currently trades at roughly 36x earnings.

Has it become too expensive?

The fact that IBKR is still a significant position in the portfolios of Bryan Lawrence and Marc Werres, indicates that they still expect to earn a decent return from this stock, even at the current levels.

Here is what Werres wrote in his Q4 2025 letter:

“Interactive Brokers should still grow its earnings at least at a mid-teens annual rate. […] Interactive Brokers also aims to pay out a dividend equivalent to a 0.5% to 1.0% yield. Between earnings growth and its dividend yield, IBKR seems poised to deliver a high teens or better annualized return over the coming years. IBKR would need to trade at more than $100 per share today to offer a market-level return.”

At the price IBKR traded at end of 2025 ($65-70), Werres is implicitly saying IBKR still offers above-market prospective returns, even after the recent run.

At the same time, Werres indicated in his latest letter that he sold some IBKR (probably in the $75-80 range), not because the thesis broke, but because the price had run hard:

While IBKR gained only 4.3% for the quarter as a whole, we trimmed some of our position early in the quarter at prices notably higher than where IBKR ended the quarter

Final decision

📌 Keeping IBKR on the watchlist (but moving it to the top of the list)

The business is exceptional, the long-term thesis is intact, but entry price matters as we have shown with the Netflix case study.

The long-term thesis is supported by two of the most disciplined long-term investors I have studied, who have both built their portfolios around this stock:

Bryan Lawrence (Oakcliff Capital): IBKR held since 2017, now 30% (!) of portfolio

Marc Werres (Hinde Group): IBKR held since 2015, ~15% position, ~27% CAGR over the holding period

That is a meaningful long-term endorsement.

My entry trigger: I will initiate a position if IBKR pulls back to around $65 or below, which is the Q1 2026 closing level and would put it materially below Werres’s trim range and meaningfully below his $100 market-level-return threshold.

That’s it for this week’s edition!

Thank you for reading and following along.

Until next week!

Thank you for introducing me to Werres! Never heard of him until now. Love the theme of your Substack. Keep sharing interesting investors 👏