Warning Signs, Downside Protection, and a Salvage Yard

Lessons from Coldplay and Seth Klarman - and a fresh look at Copart

Welcome back!

A few things on my mind this week:

⚠️ Warning Signs - Some red lights are flashing in the stock market

🛡️ Downside Protection - Legendary investor Seth Klarman on the one thing he cares about as much as upside

🚗 Salvage Cars - A fresh, honest look at one of my Guru Gems holdings that’s been bleeding: Copart

New to Guru Gems? Start here.

Last week I covered lesser-known Guru Dennis Hong, founder of ShawSpring Partners, who runs a concentrated portfolio of companies in the technology, internet, and consumer sectors

Here is the 2 minute AI audio version of today’s post if you are short on time:

⚠️ Warning Signs

🎶

“A warning sign

I missed the good part, then I realised

I started looking and the bubble burst”Warning Sign - Song by Coldplay

I’m fairly sure Chris Martin had something other than equity markets in mind when he wrote these lines. But listening to this song earlier this week, I realized how well these first three lines capture the mood around AI stocks right now.

I missed the good part

The rally has convinced a lot of people that they've missed the ‘easy’ money and that the only way to fix that is to pile into the 'hot' names before it's too late.

Howard Marks described exactly this psychology in his book Mastering The Market Cycle:

“But most investors do capitulate eventually. They simply run out of the resolve needed to hold out. Once the asset has doubled or tripled in price on the way up — or halved on the way down — many people feel so stupid and wrong, and are so envious of those who’ve profited from the fad or side-stepped the decline, that they lose the will to resist further.

My favorite quote on this subject is from Charles Kindleberger: “There is nothing as disturbing to one’s well-being and judgment as to see a friend get rich” (Manias, Panics, and Crashes: A History of Financial Crises, 1989).

Market participants are pained by the money that others have made and they’ve missed out on, and they’re afraid the trend (and the pain) will continue further. They conclude that joining the herd will stop the pain, so they surrender. Eventually they buy the asset well into its rise or sell after it has fallen a great deal.

In other words, after failing to do the right thing in stage one, they compound the error by taking that action in stage three, when it has become the wrong thing to do. That’s capitulation. It’s a highly destructive aspect of investor behavior during cycles, and a great example of psychology-induced error at its worst.”

Look at what is happening in Taiwan and Korea and tell me this isn't exactly what Marks is describing…

I started looking and the bubble burst

Is there an AI bubble? Is it 1999 all over again? I’m seeing many posts on Substack and finance news sites debating these questions, claiming either that we are reliving 1999-2000 or that “this time is different”.

As with everything, the answer needs some nuance rather than bold statements.

I have written in a few previous posts about how history seems to be rhyming lately:

Rather than repeating myself by listing every warning sign I'm seeing today, let me share two excellent pieces I read this week that captured my current thinking:

Come on in… I’ve gotta tell you what a state I’m in

So what does all this mean for my Guru Gems portfolio?

Starting with Alphabet and Amazon, my two best performers. Both have benefited from the AI rally, especially Alphabet which I bought in April 2025 when everyone thought they were done because Search was no longer relevant.

Both companies would almost certainly take a hit in a broad selloff (in fact, both are down 13% and 14% over the past month as part of a broader tech sell-off). But I see them as genuinely high-quality businesses that should keep compounding over the long run, so I'm comfortable holding them. They also remain two of the most widely owned names among the Gurus, as the latest 13F filings confirmed.

Then there is a group of names that have been sold off on the fear that AI will disrupt them (Constellation Software, CCC Intelligent Solutions, S&P Global). I probably bought CSU and CCC too early, but I remain convinced all three will do well over time, and the long-term Gurus’ activity backs up that thesis.

And finally, a few companies that are essentially AI-agnostic and have been left for roadkill despite still being high quality (Zoetis, Copart). These are exactly the kind of unglamorous, high-quality names that tend to do well once the euphoria around the hot names fades. When the dot-com bubble burst, these type of boring businesses quietly compounded while the hot names were collapsing.

→ If you enjoy this newsletter, please subscribe and help others discover it by clicking 🤍

→ If you find value here, consider buying me a virtual coffee ☕

🛡️ Downside Protection

I watched 2 very interesting interviews with Seth Klarman this week. Klarman is a legendary investor who runs Baupost, the Boston-based firm he has led for almost 44 years. In those 44 years he has had only five down years, the worst around −10%. He is also the author of the famously hard-to-find book Margin of Safety.

I will be doing a full post on Seth Klarman in the coming weeks or months, so stay tuned for that one.

For now, I just want to share one insight that stuck with me from the interviews.

It is about the importance of downside protection.

Here is the line from the first interview that captures it:

It’s a downer to talk about downside. Nobody wants to hear it when the market’s going up every day. But there’ll be a moment when things will correct. There’ll be a lot of pain and usually in those environments if we’ve protected well which so far we have, we’ll be able to put capital to work when our competitors are maybe standing back a little bit. So the opportunities that happen in the worst environments can lead to returns for years afterward from deploying more capital into those markets.

And from the second interview:

“The only place where we’re making decisions is if the downside is protected and if we can see lots of paths to winning, then we’re very interested”

In almost 44 years, Baupost only had five down years. That record came from an obsession most of the industry finds boring. As Klarman put it, “the way we protect capital is we focus on downside as much as upside.” In practice that means meticulous bottom-up research, no leverage, a willingness to hold cash when nothing is compelling, and buying unloved or distressed assets during market panics.

Protecting the downside is precisely what lets you show up on the day everyone else can’t. Klarman’s example was 2008–09: as markets fell apart after Bear Stearns and Lehman, Baupost raised significant capital within a single quarter and deployed it into distressed assets while much of the industry sat “paralyzed and frozen with fear.”

There's a deeper, mathematical reason protecting the downside matters, which a fellow Substack writer I follow, James Emanuel of Rock & Turner, laid out beautifully in his article Are You Losing A Game You Should Win?.

Using a simple coin-flip (win +50%, lose −40% on a 50:50 flip), he shows why a strategy that looks favourable can still destroy capital: a loss always needs a larger percentage gain to recover, so the typical compounded outcome is negative even when the average looks positive. His conclusion is perfectly aligned with what we just heard from Klarman: "large drawdowns damage compounding more than large gains help it."

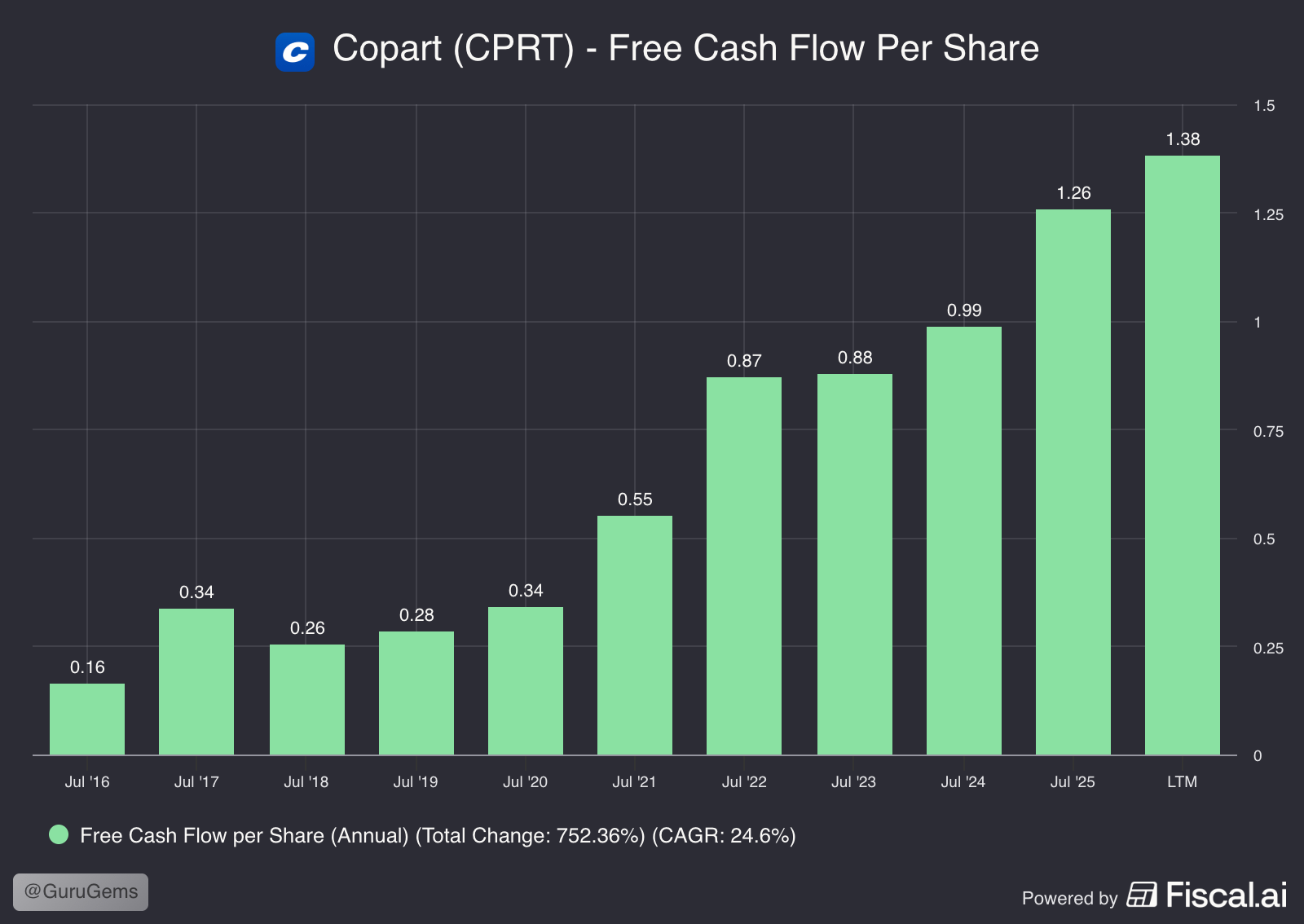

💎 Copart (CPRT) — Undervalued or value trap?

Copart (CPRT) runs online vehicle auctions, primarily for salvaged and total-loss cars. Insurance companies rely on Copart to efficiently dispose of vehicles, while buyers around the world compete for inventory through Copart’s digital platform.

Copart has compounded capital through multiple cycles without relying on leverage or hype.

Its strength can be summarized in 3 dimensions

Network effects: More buyers → higher auction prices → attracts more sellers (insurance companies) → more inventory → attracts more buyers

Long runway: Increasing vehicle complexity and repair costs means more cars are written off

Strong balance sheet: Cash is piling up, offering opportunities for buybacks and/or acquisitions

I first wrote about Copart in my review of Peter Keefe and his Rockbridge Capital portfolio.

I added the stock to the Guru Gems portfolio in January 2026, when it was down nearly 40% from its 52-week high. I added more in February when the stock kept falling.

The stock is deeply out of favor, mostly driven by slowing revenue growth over the last several quarters, and shares are now down more than 50% from their peak, the largest drawdown in over 20 years.

But the fundamentals seem to suggest a different story:

Revenue 5yr CAGR: 9.8%

ROIC 5yr Avg: 31.6%

Why I think this is still a high-quality compounder

First, let’s start with was has gone wrong:

Volumes are soft. Unit volume has declined for several quarters. More Americans underinsured or uninsured (fewer claims → fewer salvage cars), plus some share shifting between insurers. Fiscal 2026 revenue is set to dip slightly year-over-year, the first stumble in a long time.

A competitor woke up. IAA, Copart’s longtime #2, was bought by RB Global in 2023 and appears to be competing harder.

The market lost patience. A couple of earnings misses compressed the multiple hard. The forward P/E has fallen from the 30s into the high-teens.

But none of that means the moat is broken:

Pricing power is intact. Even with volumes falling, average selling prices have kept rising (mid-single digits globally, high-single digits for US insurance auctions). A broken business doesn’t get to raise prices into declining volumes.

The balance sheet is a fortress. Roughly $4.2 billion in cash against essentially no debt, with ROIC around 29%. Morningstar still rates the moat Wide.

Management is buying back stock. After years of hoarding cash, Copart repurchased about $1.6 billion of shares over the past year (~6% of market cap), most of it last quarter, with the stock below analysts’ fair value. This is the corporate version of Klarman’s “playing offense when competitors are sidelined.”

So: undervalued, or value trap? A value trap keeps getting less valuable with margins eroding and the moat crumbling. That isn’t what these numbers describe. This looks more like a wide-moat compounder working through cyclical challenges. The bear case to take seriously is “volumes staying soft longer than expected and the stock sitting in the penalty box for a year or two”. This would be painful, but survivable.

So I’m holding, and at ~$30, with the moat intact and management buying back stock, I believe the risk/reward has improved.

Red flag to watch for: if average selling prices start falling alongside volumes, that could mean the moat is genuinely eroding, and this is when I would revisit straight away.

That’s it for this week! Please like or share if you find these insights valuable.

Thank you for reading and following along.

Until next week!