Pzena at Halftime & A Fresh Look at Baxter (BAX)

Deep Discounts in Deep Value

Welcome back!

In today’s update

🔭 Pzena’s Mid-year outlook for Value

📈 Deep Discounts in Deep Value

⚕️ Baxter - A closer look at one of my Guru Gems holding

New to Guru Gems? Start here.

Last week I revisited Bryan Lawrence one year later and added Guidewire Software (GWRE) to the Guru Gems portfolio: a wide-moat software business caught in the AI-panic selloff. This week one a deep-value Guru is hunting in exactly the same waters.

Here is the 2 minute AI audio version of today’s post:

🔭 Pzena’s Mid-year Outlook for Value

I always enjoy listening to Rich Pzena. Pzena was Joel Greenblatt’s Wharton classmate and co-author of their 1979 research project that validated Ben Graham’s stock picking formula. Greenblatt once called him “one of the highest quality, smartest, nicest people I know”.

Earlier this week, Pzena Investment Management shared their 2026 mid-year outlook webinar.

Rich Pzena, together with portfolio manager Akhil Subramanian, shared what really matters for value investors in this volatile year. Three things stood out to me.

1/ The third technology cycle

Rich Pzena has now lived through three technology cycles as a professional investor: the internet bubble, the fintech boom, and now AI. His observation is that they all rhyme in the same specific way:

“The market sees it as great for the new entrants and poor for the incumbents... It’s not new technology versus old technology. It’s the purveyors of the technology versus the customers of the technology.”

In 1999, you could buy virtually any Western manufacturer for about five times its cyclical earnings power, while the internet builders were priced as if we already knew who would win. Instead, virtually every dominant incumbent adopted the new technology, ended up with higher margins than before, and the stocks were “doubles and triples and quadruples”.

Same story with fintech. Rich recalls the Citigroup CEO looking back in 2017 at the endless stream of 28-year-old founders who had promised to put him out of business five years earlier:

“Now I have a new crop of 28-year-old CEOs of startup fintech companies who are coming to sell me their technology, because they understand they don’t want to be a bank.”

The lesson for the AI era: don’t assume the customers of the technology are the losers. History suggests the opposite.

2/ Memory: peak, or plateau?

The most extreme exuberance today is in memory chips. Pzena’s view:

“While AI will change the world, it isn’t going to negate the cyclicality of memory demand.”

Akhil Subramanian on that cyclicality:

“My 8-year-old has lived through three memory cycles. He was born, there was a peak, then a trough, then a peak, then a trough, and now we’re at a peak again. My 5-year-old has lived through a cycle as well.”

Three years ago, Micron’s gross margins were roughly break-even. Today it is guiding to 85% gross margins, for an asset-heavy manufacturing business, higher than most asset-light software companies.

What’s even more striking: Micron, Samsung and SK Hynix currently earn higher gross margins than Nvidia and TSMC, the companies everyone considers the widest-moat monopolies in the industry.

Many argue memory has reached a “new plateau”. Pzena Investment instead anchors on normalized, mid-cycle earnings power five years out, factoring in new supply, potential Chinese entrants, and demand destruction from rising device prices:

“So we’re living in a moment where the demand is insatiable and everyone believes that this might be a plateau and we may not go back to the past cyclicality.

What we try to anchor ourselves to is what is the normalized earnings power of this industry based on competitive dynamics. So when we say normalized earnings power, we’re talking about 5 years out on a midcycle basis..

On the basis of normalized earnings, it’s not entirely obvious to us that this is a new plateau... it’s probably fair to say the earnings are at a peak.”

The lesson here is something I already highlighted in my Pzena deep-dive: value on today’s earnings is not value if today’s earnings are a cyclical peak.

3/ Opportunities in software

While the market crowds into the “purveyors” of AI, Pzena has been buying the customers. Specifically, software companies crushed by the SaaSpocalypse: the fear that AI lets anyone replicate established software over a weekend.

In the webinar they discuss 2 names:

Workday (WDAY) — mission-critical ERP software for people-centric businesses (think Chipotle or Walmart, hiring thousands of people a week). Retention runs at 97–98%, and AI cuts both ways in their favor: it powers new products (a conversational AI tool that filters 2,000 job applications for a single Chipotle store) and reduces R&D, the biggest cost bucket of any software company. Pzena calls it “a very compelling investment opportunity.”

SAP — another ERP giant, serving supply-chain-heavy customers like BMW and Mercedes. Same mission-critical profile, plus a catalyst: as SAP retires its decades-old ECC product, most of that installed base is migrating to SAP’s next generation, which is a multi-year revenue uplift the market is undervaluing.

If you read last week’s Guru Gems issue, the following description of WDAY and SAP will sound familiar:

Mission-critical system of record. Retention near 100%. Enormous switching costs. AI as an accelerant rather than a death sentence. Sold off indiscriminately in the AI panic.

That is, almost word for word, the Guidewire (GWRE) thesis from last week. Guidewire’s ~99% retention is even higher than Workday’s.

Two Gurus with completely different styles (Lawrence the concentrated quality investor, Pzena the deep-value contrarian) are finding opportunities in the same corner of the market.

→ If you enjoy this newsletter, please subscribe and help others discover it by clicking 🤍

→ If you find value here, consider buying me a virtual coffee ☕

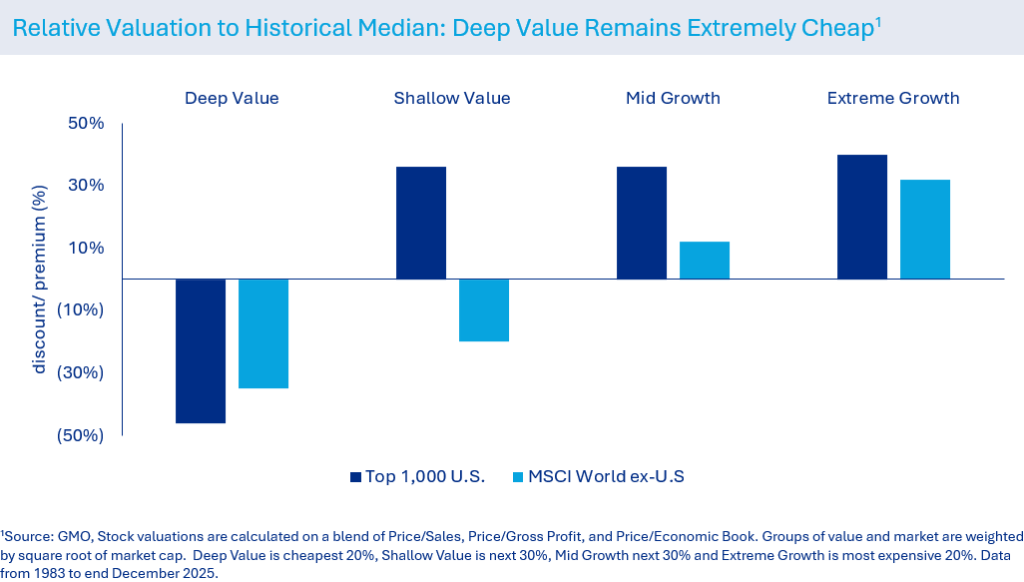

📈 Deep Discounts in Deep Value

I came across a piece from Oldfield Partners — Away From the Casino Tables: The Wildest Value Gap Since 1999 — which connects beautifully with Pzena’s webinar.

It was the most widely read piece in Latticework‘s Weekly Inspiration newsletter last week. I highly recommend subscribing; there are always fantastic articles.

The core of the piece is one chart and one statistic. Splitting global equities into four valuation buckets and comparing each to its own 40-year median:

Deep value globally trades at a 45% discount to its historical average

Extreme growth trades at a ~40% premium

The author, Sam Ziff, notes that only once before (late 1999, early 2000) has the market been more expensive than today based on the Shiller P/E ratio. Warren Buffett recently observed that “we’ve never had people in a more gambling mood than now”.

The last time markets were this concentrated and this expensive, the following decade (2000–2009) delivered roughly zero total return for the S&P 500 and MSCI World, while emerging markets doubled and value beat growth. This should serve as an important warning to index investors.

Now connecting this to what Rich Pzena said in the webinar. Asked whether value investing is broken after another stretch of index outperformance:

“Value investing can’t be broken... if you do it right and buy things for less than they are worth, you will win.”

And on today’s valuation spreads:

“Our portfolio sells at about 20 or 30% below the valuation [forward P/E] it did 10 years ago... and the market is roughly 30% higher than it was 10 years ago on the same metric. The spreads are as wide as they get.”

Betting that the same expansion repeats from today’s starting point is, in Pzena’s words, “a tough bet”.

Or as Oldfield puts it:

“The casino may stay open a while longer. However, the best returns over the next decade are unlikely to come from the tables everyone is crowded around.”

The point is not to see this as a signal to time the market, but rather as a signal about where the next decade’s returns are likely to come from.

Which brings me to one of the most out-of-favor stocks in my portfolio…

💎 A Gem Revisited: Baxter (BAX) — Hold, Add, or Fold?

The setup: Baxter is a 95-year-old medical technology company selling essential hospital products: sterile IV solutions and infusion pumps, smart hospital beds and patient monitoring, and specialty injectables. Its North Cove plant produces roughly 60% of all IV solutions used in US hospitals.

Baxter is deeply out of favor by any objective measure: the shares have lost over 70% over five years while the market sits near record highs, Wall Street's consensus rating is Hold with an average price target below the current share price, and the dividend cut expelled the income-investor base.

Exactly the kind of situation Rich Pzena hunts for. At the end of Q1, Baxter was among Pzena’s top-5 positions, and at the end of Q1 Pzena Investment Management owned more than 10% of the entire company.

In the mid-year webinar, when asked where he sees value today, Pzena pointed to healthcare, and named Baxter specifically:

“You have companies like Baxter, which hasn’t really rallied and has a very strong set of businesses that have earned high margins, strong free cash flows, modest growth rates — that have run into problem after problem after problem that the former management team was unable to solve, and the new management team is in the process of solving...

It’s priced as if they’re not going to succeed. And so if they do, you make a lot of money. If they don’t, you don’t lose a lot of money.”

I first bought Baxter in September 2025 around $23, added below $20 in November, and again around $20 in January. My average purchase price is $20.4. The stock closed at $22.6 this week, putting my position up 10.6%, and making Baxter a 5–6% position in the Guru Gems portfolio. A good moment to re-examine the thesis.

1/ What has gone wrong (a lot)

First a reality check. Since my original write-up, the “problem after problem after problem” list has grown:

The Novum IQ pump hold. In July 2025, Baxter voluntarily paused US/Canada shipments of its Novum IQ infusion pump after reports of underinfusion were linked to 79 serious injuries and two deaths. The stock fell ~21% in a day. The hold remains in place, ceding pump share to BD and ICU Medical, and has triggered a securities class action.

The dividend is essentially gone. In late 2025, Baxter cut its quarterly dividend from $0.17 to $0.01 (a 94% cut, ending a 55-year streak) to free up >$300M per year for debt reduction.

The balance sheet is stretched. ~$8.6B of long-term debt remains from the 2021 Hillrom acquisition. S&P and Moody’s both downgraded Baxter in November 2025 to one notch above junk, and the 3.0x net-leverage target slipped from end-2025 to end-2026.

Margins and earnings are going the wrong way. Adjusted gross margin fell 900 basis points year-over-year in Q4 2025, adjusted operating margin is guided at just 13–14% for 2026, and adjusted EPS is guided down to $1.85–$2.05 from $2.27 in 2025.

Management churn. CEO Joe Almeida left abruptly in early 2025; new CEO Andrew Hider (ex-ATS and ex-Danaher) only started in August 2025, and the CFO seat is currently held on an interim basis.

This is not a quality compounder having a bad quarter. This is a genuinely wounded business. So why hold it?

2/ Is it ‘Good’?

The core franchise survived all of the above intact:

Irreplaceable infrastructure: ~60% of US IV fluids from one vertically-integrated plant. When Hurricane Helene knocked North Cove offline in 2024, US hospitals rationed IV bags, which shows how few substitutes exist.

Switching costs: infusion pumps and smart beds are wired into hospital electronic medical record (EMR) systems, drug libraries and biomed workflows

Essential demand: hospitals buy these products in every economic scenario.

Morningstar still assigns a narrow moat, though it flags real erosion at the edges: pump share losses during the Novum hold, IV share slippage during the Helene outage, and generic price pressure in injectables.

Verdict: an essential, moaty core wrapped in a badly managed decade.

3/ Is it ‘Cheap’?

At $22.6, Baxter trades around 11–12x forward earnings, which is a steep discount to the medtech peer group (typically mid-teens) and to its own pre-2022 history.

Analysts’ average price target is ~$21.50 (consensus: Hold), which is below the current price. The market is pricing in that nothing improves.

If new management delivers the margin recovery and the Novum hold lifts, earnings could reach ~$2.40+ by 2027 and a re-rating toward 13–14x would imply a stock around $30. If execution slips further, trough multiples on ~$1.80 of earnings suggest ~$15.

From $22.6, that is roughly +33% in the good scenario versus −34% in the bad one. This ‘bet’ only remains attractive if you believe, as Pzena does, that the odds of the fix are meaningfully better than a coin flip: the problems are operational rather than structural, demand is not in question, and a cost-focused outsider CEO with 92% performance-linked pay now runs the company.

Verdict: statistically cheap, but cheap for a reason. The bet is on execution, not on the multiple.

4/ To Hold or Not to Hold

Last week I scored Guidewire against Lawrence’s six questions. Let me do the same for Baxter and score it against Pzena’s own framework from my original deep-dive:

Is the business under-earning versus its historic norms? ✅ Operating margins of 13–14% sit well below medtech peers, returns on capital are currently below Baxter's cost of capital, and earnings are depressed by fixable operational issues (pump hold, hurricane costs, stranded costs, mix), not by falling demand.

Are the problems temporary and fixable, not structural? ⚠️ ✅ Pump holds, hurricane damage, bloated costs and bad M&A are all fixable in principle, but this management team hasn’t proven it can fix them yet.

Is the market pricing the downside case? ✅ ~11x forward earnings, consensus price targets below the share price, a departed income-investor base, and a 70%+ drawdown from the 2021 highs.

If they fix it, is the outcome skewed in my favor? ⚠️ Only with better-than-even odds on execution, and less skewed at $22.6 than it was at my $20.4 average cost.

📌 Final decision: Holding, not adding

Baxter stays in the Guru Gems portfolio as my designated deep-value turnaround, but I’m not adding at ~$23.

Baxter reports Q2 2026 earnings on July 30, its first quarter under a newly announced two-segment structure. Three things I’ll be watching:

Operating-margin progress toward the 13–14% guide;

Any timeline on lifting the Novum pump hold. Current guidance assumes the hold stays in place for the entire year, so any lift would be pure upside versus guidance;

Progress toward the 3.0x leverage target.

If those indicators start moving the right way, Baxter could be the kind of skewed outcome Pzena describes. If margins stall again, I may need to consider if holding this company still makes sense.

That’s it for this week! Please like or share if you enjoyed this post.

Thank you for reading and following along.

Until next week!