Norbert Lou - The Punch Card Mindset

On punch cards, patience, and PayPal

Welcome to a new edition of Guru Gems, where I study the world’s long‑term investing masters and build a portfolio based on the Gurus’ wisdom.

In today’s edition:

🔍 Guru in the spotlight: Norbert Lou

🧿 Why less is more — and how focus drives extraordinary returns

💳 Stock in focus: PayPal Holdings (PYPL)

If you are new to Guru Gems and want to know more about my journey, start here.

Guru in the spotlight: Norbert Lou

Norbert Lou is the founder of Punch Card Capital, an investment firm named after Warren Buffett’s famous ‘20-punch card’ metaphor. Buffett told business students that they’d be better off if they could make only 20 investments in a lifetime — a reminder that investing success comes from patience, conviction, and selectivity.

Norbert Lou took that literally. His fund rarely holds more than five positions. Since founding Punch Card in 2004, he has quietly compounded capital at rates that put him among the most successful — yet least publicized — investors of his generation.

Despite managing more than $300 million, there is very little public information on Norbert Lou. If you Google him, you won’t find pictures, you won’t find interviews (except for one in 2011), and you won’t find any investor letters.

The Greenblatt connection

Just like investing master Rich Pzena, Norbert Lou has a connection with Joel Greenblatt

In 2001, Lou came across Joel Greenblatt’s Value Investors Club - an online idea-sharing forum for investors - and submitted a write-up on NVR, a small homebuilder with a new business model.

Lou first purchased NVR in 1997 and while the stock had already gone up more than 500% since then, he still believed it was a very attractive opportunity. Within a year, the stock went up another 140% and it ended up being a 15-bagger within 5 years.

Lou posted more ideas over the next years and all of them ended up beating the market. Three of his ideas won the site’s ‘Idea of the Week’ award.

This caught Greenblatt’s attention and he ended up helping Norbert Lou set up Punch Card Capital, and even seeded the fund together with his Gotham partners.

“We wanted to be involved with a great investor and there are many benefits as a result of being able to collaborate in a small way with someone who is so talented. Our benefit is that we get to invest our own money with him.”

“To this day, I hand out the first 3 write-ups he wrote on the Value Investors Club to my students at Columbia, to show them what a brilliant, concise, straightforward and clear investment thesis looks like.”

—Joel Greenblatt

If you enjoy this newsletter, please help others discover it by clicking 🤍

The Punch Card Mindset

Since there is very little public information available about Norbert Lou, I will quote from the 2011 article which gives some insight into his thinking process and approach.

I highly recommend reading the full article.

On concentration

“In college I had seen a study that said a portfolio of six to eight stocks could get you most of the statistical benefits of diversification, so I never started out with the idea that you had to have 50 to 100 stocks to be prudent. And I hadn’t been drilled into believing that a position over 5 percent was considered big […]. I knew NVR was better than anything else I had seen to that point, and I knew that I should buy as much as I could stomach.”

This first sentence is almost exactly what Joel Greenblatt wrote in ‘You Can be A Stock Market Genius’:

After purchasing six or eight stocks in different industries, the benefit of adding even more stocks to your portfolio in an effort to decrease risk is small.

You can read a detailed summary of this book in my deep-dive on Joel Greenblatt:

On patience

“By buying a great stock and just hanging on, I ended up seeing how that could work out better than a lot of strategies. That really had an impact later on how I viewed the ideal investment.”

The next one is a brilliant example of doing deep research, knowing what you want to own and then buying it when the opportunity presents itself:

Norbert watched TGS-Nopec [a provider of marine seismic data] for seven years without buying any shares. Then, in April 2010, the Deepwater Horizon offshore drilling rig leased by BP suffered a blowout in the Gulf of Mexico, releasing five millions barrels of oil into the water in three months. The U.S. government immediately imposed a moratorium on drilling in the Gulf […]

TGS-Nopec, which derives roughly half its business from the Gulf, saw its stock price trade down to six times after-tax earnings. “TGS-Nopec was priced as if the Gulf of Mexico would never re-open,” Norbert said. “And with the constant stream of negative headlines in newspapers every day, it was easy to see how investors could get scared away.”

Punch Card began accumulating a position in June 2010. During the second half of the year, the stock appreciated 90 percent in U.S. dollar terms as the drilling moratorium was lifted, and it rose another 30 percent in the first half of 2011.

On long-term thinking

Norbert decided he would report his performance to limited partners only twice a year. “If you have to report monthly, you start being concerned about what the monthly numbers are and it’s just hard to be unaffected by it,”

[…] Finally, he wanted an extra restrictive lock-up policy. It required initial investors to keep their money in the fund for two years. “Actually, it’s a little worse,” he admitted. “If you invest in December, it would take two and a half years to get to the point where you could redeem on June 30

“The fund will limit itself to investors who are not concerned with short-term results,” he wrote in his first letter to partners in 2005.

Punch Card Portfolio

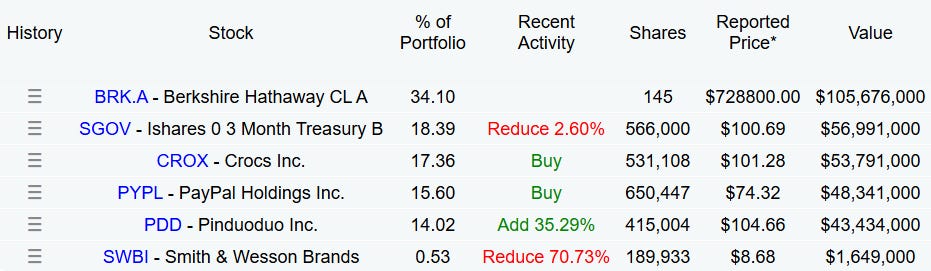

Based on Punch Card’s most recent 13F filing, here is a snapshot of Lou’s Q2 holdings:

If we exclude the 0-3 Month T-bills (SGOV) which is essentially cash and the Smith & Wesson Brands position which he has been unwinding, there are really only 4 stocks in his portfolio.

As the chart below shows, Norbert Lou makes very few changes to his portfolio:

It was therefore quite surprising to see that during Q2 of this year he initiated 2 new positions: Crocs and PayPal Holdings.

Crocs currently has a very high ‘Magic Formula’ ranking (‘Cheap’ and ‘Good’) - which is why I recently added it to my Magic Formula Portfolio.

The other new position is PayPal Holdings, a global leader in digital payments.

Let’s have a closer look at PayPal

PayPal Holdings - To buy or not to buy

As always, I’ll evaluate this Guru Gems candidate using my Terry Smith-inspired framework:

1/ Buy good companies

PayPal Holdings (PYPL) is a global leader in digital payments, with over 400 million active users operating in 200+ countries.

But the stock tells a painful story. PayPal is down nearly 77% (!) from its all-time high of $300+, now trading near $70.

Many investors have written it off as disrupted by Apple Pay, Google Pay, Stripe and Adyen.

But it looks like Norbert Lou sees something different.

I came across many deep-dives online; some claiming PayPal is a value trap, others claiming PayPal is at an inflection point with very strong fundamentals and profitable growth ahead.

Here are two good write-ups I would recommend for a deeper understanding:

The Intrinsic Value Newsletter - PayPal: Value Trap or Multibagger?

Rijnberk InvestInsights by Daan | InvestInsights - PayPal is a Bargain – A Rare Chance for 19% Annualized Returns

Let’s look at PayPal through Norbert Lou’s eyes and highlight why he might believe PayPal is at an inflection point.

Why PayPal made it on the Punch Card

Strong brand & network moat:

PayPal remains one of the most trusted digital payment platforms, with over 430 million active accounts worldwide. Its brand and embedded position across merchants form a self-reinforcing network effect — something Lou has highlighted as a factor in some of his previous winners.Pricing power & cash flow engine:

Like Lou’s past winners (NVR, Quinsa), PayPal exhibits the quiet power of recurring revenue and pricing power. Despite competitive pressure, it still generates $6-7 billion in free cash flow annually.Underappreciated intrinsic compounding:

PayPal’s fundamentals have outpaced its share price — trading at 13× forward earnings despite double-digit EPS growth. Lou likely sees this as a “great business, mispriced for fear” — similar to how he viewed NVR post-bankruptcy or Quinsa amid Argentina’s chaos.Operational turnaround:

New CEO Alex Chriss is cutting costs, focusing on high-margin products, and quietly executing a turnaround

Aggressive capital return:

PayPal authorized a massive $15 billion share repurchase program - with $6 billion allocated for 2025 - representing over 20% of its current market cap.

I believe this last point could be what triggered Norbert Lou’s interest in PayPal (and Crocs as well!)

Buybacks was exactly why Lou started looking into NVR in 1997:

“By mid-1997, Norbert was actively searching for companies that were buying back their shares […]. He saw buybacks as a good indicator that a business was generating cash and was disciplined about returning it to shareholders. One day during some downtime at Brown Brothers, he came across a press release announcing that NVR Inc., a small homebuilder, was initiating a stock repurchase program. When he saw that NVR’s buyback was the latest in a series that would total $100 million over four years—remarkable for a company with a market cap of only $275 million—he set out to learn more.”

2/ Don’t overpay

One thing most people seem to agree on is that PayPal is relatively cheap; PayPal’s forward P/E of 13x is well below its historical average.

The stock trades at 2017 levels despite more than doubling revenue and net income since then.

PayPal reached a 52-week low of around $56 in early April (probably following the ‘Liberation Day’ sell-off), so it could very well be that Norbert Lou saw that as an opportunity to initiate his position.

3/ Final decision

When an investor like Norbert Lou makes a 15% bet on a stock at 13x earnings, it’s worth asking: what does he see that the market doesn’t?

I’m strongly considering adding PayPal to the portfolio but will wait for the Q3 earnings (28 October) to clarify the turnaround progress and I will also watch for any further accumulation by Lou in his Q3 13F (deadline 14 November).

📌 I’m not (yet) adding PayPal Holdings to the Guru Gems portfolio, but I am adding it to the watchlist with a view to start a 4–5% position pending next quarter’s results.

“When you can be really patient and selective, you have the luxury of waiting for that confluence of multiple forces.” — Norbert Lou

As always, thank you for reading and following along on my journey. Follow me on X @guru_gems for more Guru Gems insights.

Until next week!

Great post. Thanks!

Alternative Magic Formula Ranking:

The Higher the score the better

.

Alternative Magic Formula Score

= ROIC × E/P