Dennis Hong & ShawSpring's Ecosystem Control

On ecosystem lock-in, solving for ‘Hall of Fame’ returns, and the Korean Amazon

In today’s edition:

🕴️ The Guru: Dennis Hong — the shopkeepers’ son who grew ShawSpring from $10m to over $1bn, running just 5–10 stocks

🌐 The Playbook: Ecosystem Control — Hong’s framework for defining quality

💎 The Gem: Coupang (CPNG) — a new Q1 2026 position, and a stock Hong has held before

2-minute AI audio version of today’s post:

Guru in the spotlight: Dennis Hong

Background

Dennis Hong grew up as the son of two shopkeepers in Ontario (“We basically were purveyors of cigarettes and lottery tickets”) which is where he first learned about business. Neither parent went to university, Hong was the first in his family to do so.

One of his applications (“one of my lottery tickets”) hit, and he got into Yale. To cover ~$4,000 a semester he searched the campus job board for the highest hourly rate and landed, almost by accident, at the Yale Investments Office, which was run by the legendary David Swensen.

At the time he didn’t even know who Swensen was. Sitting in on manager meetings with the likes of Seth Klarman and Chase Coleman, and reading partner letters in the filing room, became his real education.

From there he spent a couple of years at Matrix Capital, then in 2009 he became employee number two at Altimeter Capital (founded by Venture Capitalist Brad Gerstner), which he helped scale from $2m to $400m.

Launching ShawSpring

At 30 he enrolled at Harvard Business School intending to network his way into a fund launch, and then dropped out after his first year when a Boston family office offered to back him. ShawSpring Partners launched on 15 July 2014 with $10m.

ShawSpring’s assets grew from $10m to over $1.5bn in less than seven years. (It did significantly decrease again over the past years, more on that later.)

There is no IR team and no marketing department. Hong is, in his words, the IR, the portfolio manager, the marketer and the CEO. The ceiling on the firm’s size, he says, is simply his own bandwidth to maintain a real relationship with every client.

If you enjoy this newsletter, please help others discover it by clicking 🤍

And if you would like to support my work, consider buying me a virtual coffee ☕

ShawSpring’s Playbook

ShawSpring’s Partner Letters are unfortunately not publicly available and there aren’t a lot of recent interviews, but there are some older interviews and letters that contain enough to study Hong’s thinking process and investment approach.

Here is a chat between Dennis Hong and Robert Vinall which I much enjoyed:

Hong’s firm runs on a single organising principle: maximise the return on time and effort spent. With a five-person team hunting for 5–10 stocks out of a universe of ~50,000, everything has to be “repeatable, replicable and scalable”.

Here are 4 pillars of Hong’s framework which I distilled from the different interviews or available letters

1. 🌐 Ecosystem Control: lock-in across every constituency

One idea sits at the centre of how Hong invests: Ecosystem Control

Think of every business as an ecosystem. The customer is the catalyst that brings cash in, and that cash then flows through all the other constituencies: suppliers, manufacturers, employees, management, investors…

The highest-quality businesses are the ones where every constituency is locked in so completely that it would be economically irrational for any of them to leave for a competitor ecosystem.

That dynamic is rare, and it’s the filter ShawSpring uses to sort ~50,000 companies down to a handful.

“If it doesn’t have this characteristic of ecosystem control, you just sort of drop it and go to the next one.” — Dennis Hong

Underpinning it is a definition of compounding borrowed from Peter Kaufman: “constant, continuous, dogged improvement over very long time frames”. Hong wants businesses that grow revenue, earnings and free cash flow with that kind of positive linearity regardless of the macro environment. Ecosystem Control is his test for which ones can.

Hong applies Ecosystem Control to his own firm, too. He deliberately builds lock-in with his clients (access to him directly, no intermediaries), his teammates (he wants them for their whole careers), and even his portfolio companies (being the kind of shareholder a CEO is glad to see on the register). His framework is as much about how he runs ShawSpring as what he buys.

2. 🎯 Concentration and a punishing hurdle

ShawSpring runs just 5–10 stocks in service of what Hong calls “Hall of Fame returns”

Over his ~40-year horizon he says he is aiming for a “two-handle” annualised return (20%+), with a very high bar for entry of roughly a 30% IRR (internal rate of return) over 3–5 years. (Whether he’s actually clearing that bar, we can’t verify, but it’s a useful way of how to think about a hurdle rate.)

As he tells his team, unless an idea could plausibly triple or quintuple over that window, it isn’t worth the time.

The firm runs as “one team, one portfolio, one P&L” (“there’s no ‘sleeves’ in our firm, everyone owns every position”), and to fight group-thinking, Hong appoints himself ‘chief pain in the a**’: once a new idea is about a third researched, his job is to try to kill it.

With ten strong names already in the portfolio, the bar to displace an existing name is meant to be very high.

3. 🛒 The ‘trigger-ready’ list: patience as process

ShawSpring keeps a shopping list of ~200 businesses that appear to have ecosystem control.

And within that shopping list they have a ‘trigger-ready list’, a subset of fully researched businesses which they really like, but where the only criteria missing is a good price.

When a sell-off drags a business down to Hong’s hurdle rate, the team can act immediately. His March-2020 purchase of Square, after a ~60% drop, is an example of this.

4. 🔭 Optionality: paying for the upside the market can’t see

If Ecosystem Control is how Hong defines quality, Optionality is how he thinks about growth the market is missing.

In a 2020 letter, Hong defined Optionality as “the expected value of a current or future investment that is unknowable or difficult for the market to discern.”

He argues that the market prices the visible core business well, but struggles with the less knowable, so it tends to draw a straight line from today’s numbers and ignore what isn’t yet on the page.

Hong identifies four types of optionality:

New business — leveraging the core’s infrastructure (Amazon → AWS; JD.com → JD Logistics).

Product / category expansion — complements that deepen the value proposition (a marketplace adding groceries; software adding modules).

Strategic shift — a related pivot to a better model (Netflix DVDs → streaming; Adobe → SaaS)

Geographic expansion — replicating success in a new region (Starbucks into Asia; Sea’s Shopee across markets).

Hong’s Optionality reminded me of the “Abundant Growth Opportunities” pillar from Marc Werres’s framework.

A company with significant optionality possesses a pipeline of potential future products, services, markets, or business lines. If management successfully develops those opportunities, they become the growth engines that allow the business to compound for many years.

Amazon illustrates this connection well. Hong would highlight AWS, advertising, Prime, and logistics as examples of Optionality. Werres would look at the same developments and conclude that Amazon possesses ‘Abundant Growth Opportunities’. Different language, but ultimately the same underlying idea: great businesses continuously create new ways to grow.

The ShawSpring Portfolio

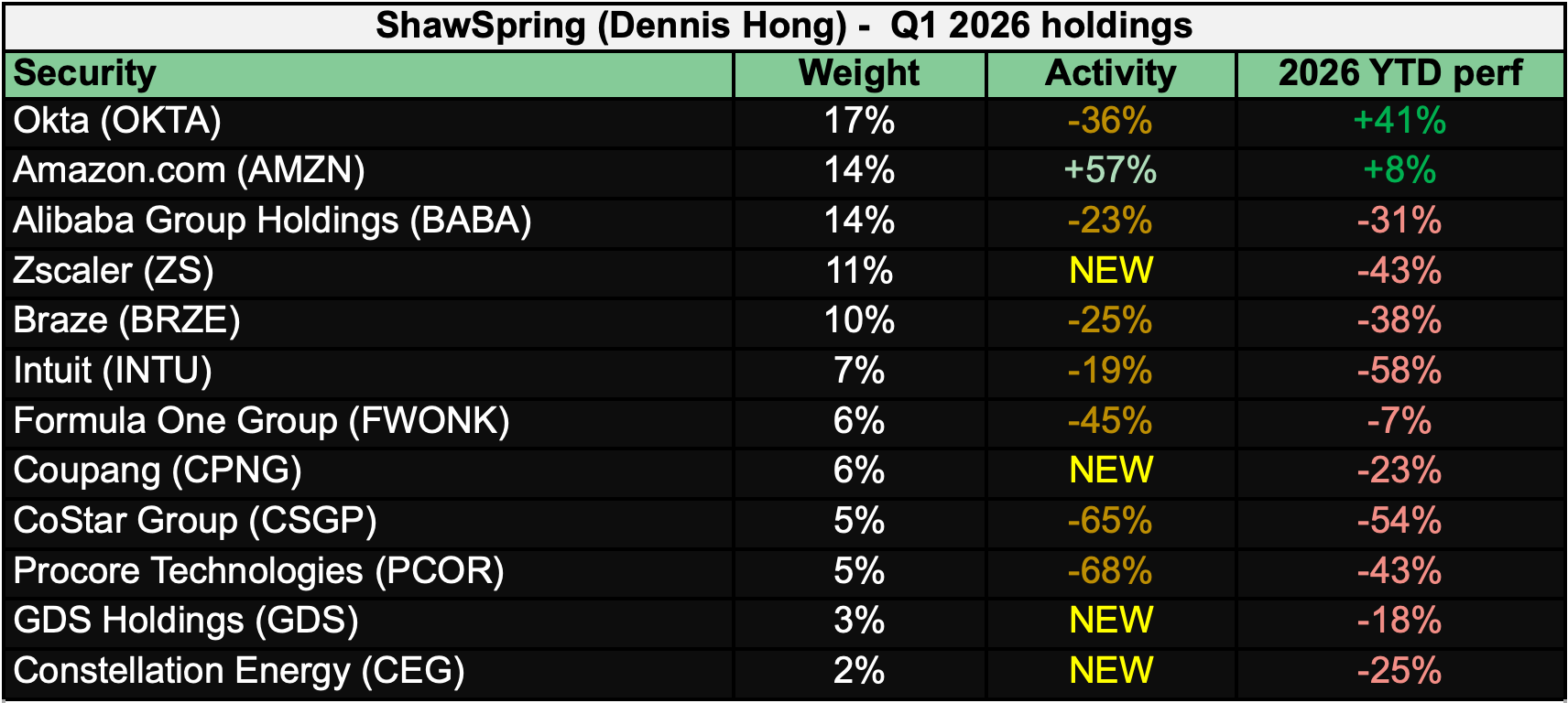

Below is an overview of ShawSpring’s US equities portfolio at the end of Q1 2026.

This is a portfolio of high-growth technology and internet names: Okta, Zscaler, Braze,… businesses earlier in their potential compounding curve than a typical Guru Gems holding.

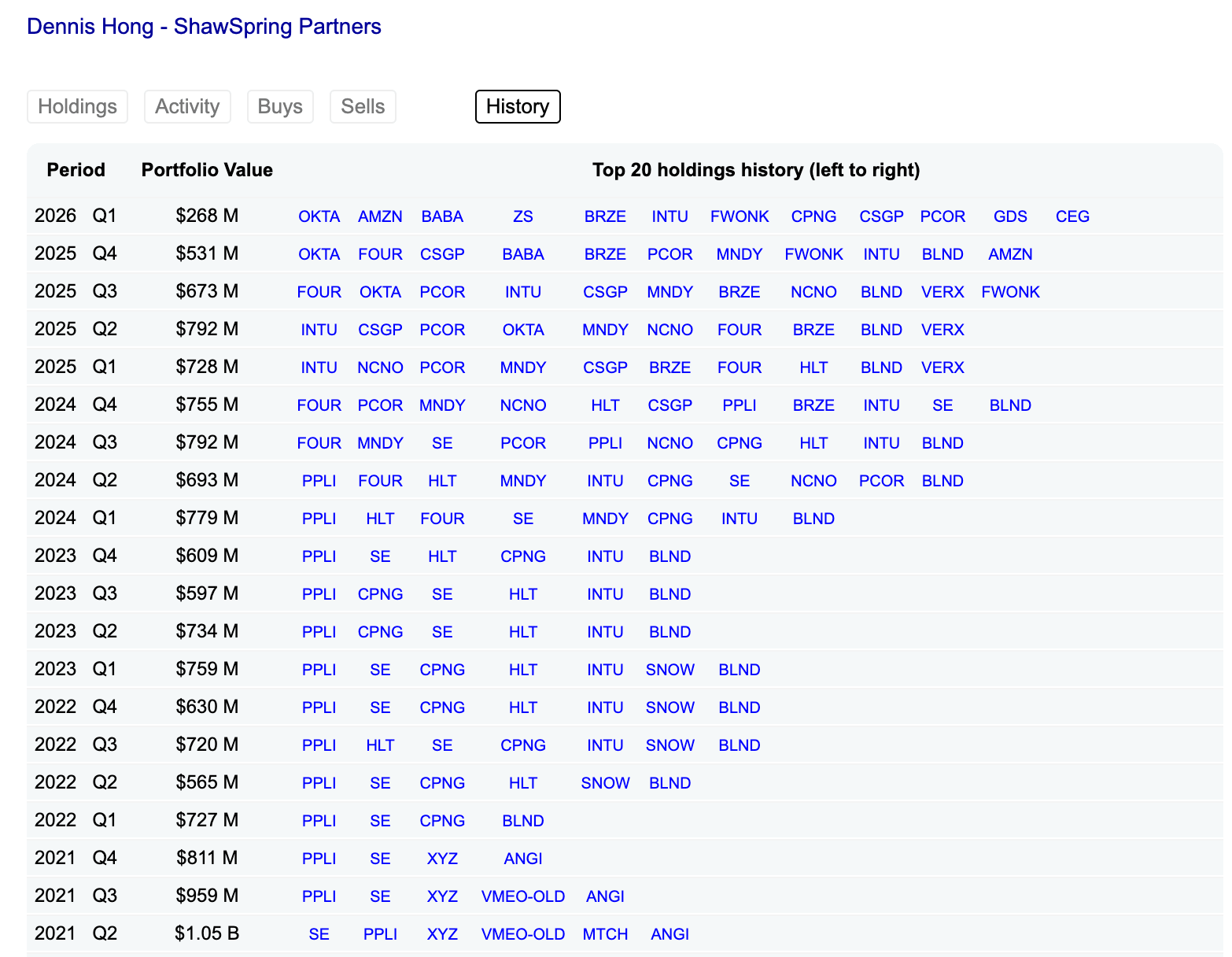

It’s also worth looking at the holdings history to get a sense of the turnover in the portfolio

Here is where I’m struggling a bit to match the frameworks and what I can actually observe. With no audited returns, the public 13F filing is the only view we have, and it may not be the full picture (US-listed long positions only, so no non-US names or cash).

But it’s still worth looking at it, because it raises some questions:

The turnover looks relatively high for a framework built on the idea of ‘constant, continuous, dogged improvement’

Shift4 Payments (FOUR) was bought in Q1 2024, became the largest position by Q4 2024, then trimmed throughout 2025 (possibly taking profits as the stock peaked in early 2025), significantly adding again in Q3 2025, but then sold entirely during Q1 2026.

Intuit (INTU) became the largest position in early 2025 and is both much smaller and down sharply since.

Coupang (our Gem for today) was owned in 2022–24, exited, and is now back in the portfolio.

The disclosed US equities portfolio has shrunk a lot. ShawSpring’s 13F value peaked over 1 billion in 2021 and stood at about $268m by Q1 2026. Some of that could be market drawdown, some could be client redemptions or it could be a move to cash or foreign equities (Dennis Hong did mention in an interview that he would be looking more at Asia). But a ~70% decline in disclosed US equities is still hard to reconcile with a smoothly compounding fund.

Of course, the above doesn’t prove the approach is flawed, a concentrated portfolio is volatile by design, and 13Fs certainly don’t tell the full story. But it does mean I can’t point to ShawSpring and say “look how well this works” like I may have done with Marc Werres and Hinde Group.

If anyone has access to ShawSpring’s performance or recent letters (@Dennis Hong, if you happen to read this ;-) ), I’d love to read them and will be more than happy to do a part 2 of today’s post.

💎 The Gem: Coupang (CPNG)

In Q1 2026, Hong re-opened a position in Coupang (NYSE: CPNG), the dominant South Korean e-commerce and logistics company often described as ‘the Amazon of Korea’.

It was one of four new buys in the quarter (alongside Zscaler, GDS Holdings and Constellation Energy), and he also added 57% to his Amazon position. With Alibaba as his 3rd largest position, his portfolio is clearly tilted toward scaled ecommerce platforms.

Hong is not the only Guru buying Coupang

I always look for Gems held by multiple Gurus and Coupang caught my eye in Hong’s portfolio because I had just read an investment thesis from Miller Value Partners on the same name. Here is the link:

Miller Value Funds - What We Own/Why We Own It - Coupang Inc. (CPNG)

Miller Value Partners was founded in 1999 as a joint venture between Bill Miller and Legg Mason Inc.

Bill Miller is most famous for his historic run managing the Legg Mason Capital Management Value Trust, where he beat the S&P 500 for a record 15 consecutive years (1991–2005). He’s definitely on my list of Gurus to cover in the future.

What does Coupang actually do?

Here is the introduction from Miller Value Partners’ write-up:

Dubbed the “Amazon” of Korea, Coupang is the leading e-commerce retail and logistics provider in the country. The company has over 100 fulfillment centers in Korea, with 70% of the nation living under 7 miles from a Coupang fulfillment center, enabling rapid delivery. In addition to selling owned inventory, Coupang sells advertising and goods from third-party merchants. It also provides restaurant ordering and delivery service through its Eats segment, while Coupang Play is a content-streaming service.

Coupang generates roughly $35bn in revenue across two segments: Product Commerce (~85% — its core retail, Rocket Delivery and WOW membership engine) and Developing Offerings (~15% — Coupang Eats, Play streaming, fintech, Taiwan and other bets). It serves Korea plus a growing international footprint, and employs over 100,000 people.

Not the first time Dennis Hong buys Coupang

Hong has owned Coupang before: it was the second largest ShawSpring holding in 2023 (around 22% of the 13F portfolio in Q2 2023). So it isn’t exactly a new idea for ShawSpring. While it’s unclear why they got out of the position in Q4 2024, I assume the reason they are getting back in, is because they believe it is a ‘great company temporarily on sale’:

A late-2025 data-security incident and a large customer-voucher program hit margins, pushing Coupang to a Q1 2026 net loss of ~$266m on revenue of ~$8.5bn.

The shares fell sharply, down roughly 30%+ year-to-date by spring 2026, resulting in multiple analyst downgrades.

Underneath, the business kept growing (Developing Offerings +28%), membership recovered toward ~80% by April, and management expanded the buyback authorization to $2bn.

One of Hong’s favourite lines, from Intel’s Andy Grove, captures the bet he’s making on Coupang’s management:

“Bad companies are destroyed by crisis, good companies survive them, great companies are improved by them.” — Andy Grove

Why CPNG fits the Ecosystem-Control playbook

Coupang’s Rocket delivery network, WOW membership, Coupang Eats and Play streaming, and its third-party marketplace lock customers, merchants and the logistics fleet into a single web.

The more members join, the denser the delivery network; the denser the network, the harder it is for a customer or a merchant to leave. That is lock-in across constituencies, exactly what Hong screens for.

Let’s look at some of the key elements from Hong’s framework

🔒 1. Customers locked in ✅

Coupang has built one of the strongest consumer ecosystems in South Korea.

Rocket Delivery, Rocket Fresh, Eats, Travel, and the WOW membership create increasing switching costs. Once consumers become accustomed to same-day or next-day delivery and bundled services, changing platforms becomes inconvenient. The WOW membership is particularly powerful because it increases engagement across multiple services.

🏪 2. Suppliers/Merchants locked in ✅

Coupang is becoming an increasingly important sales channel for merchants, but merchants are generally less captive than consumers. Large brands can still sell through multiple channels, while smaller merchants benefit greatly from Coupang's logistics and customer reach. The marketplace is strong, but merchant lock-in is probably not yet at Amazon Marketplace or MercadoLibre levels.

🚚 3. Logistics moat (scale) ✅

This is probably Coupang's strongest advantage. The company has spent years building a nationwide fulfillment and last-mile delivery network that would be extraordinarily expensive to replicate. The density of its network creates faster delivery, lower costs, and better customer experiences, reinforcing its competitive position. Few competitors can justify the capital required to build a similar infrastructure.

🔭 4. Optionality ✅

Coupang scores exceptionally well here and fits all four of Hong’s types: new businesses, category expansion, strategic evolution, geographic reach.

The company continues to launch new businesses that leverage its existing customer base, logistics network, and brand. Advertising, Eats, Travel, Fintech, WOW, and future services all represent potential growth engines. Importantly, these initiatives are not standalone ventures, they are extensions of the existing ecosystem, which increases their probability of success.

To Buy or Not to Buy

Now that we’ve shown that Coupang fits the Ecosystem-Control playbook, let’s have a closer look at whether I should add it to the Guru Gems portfolio

Is it ‘good’?

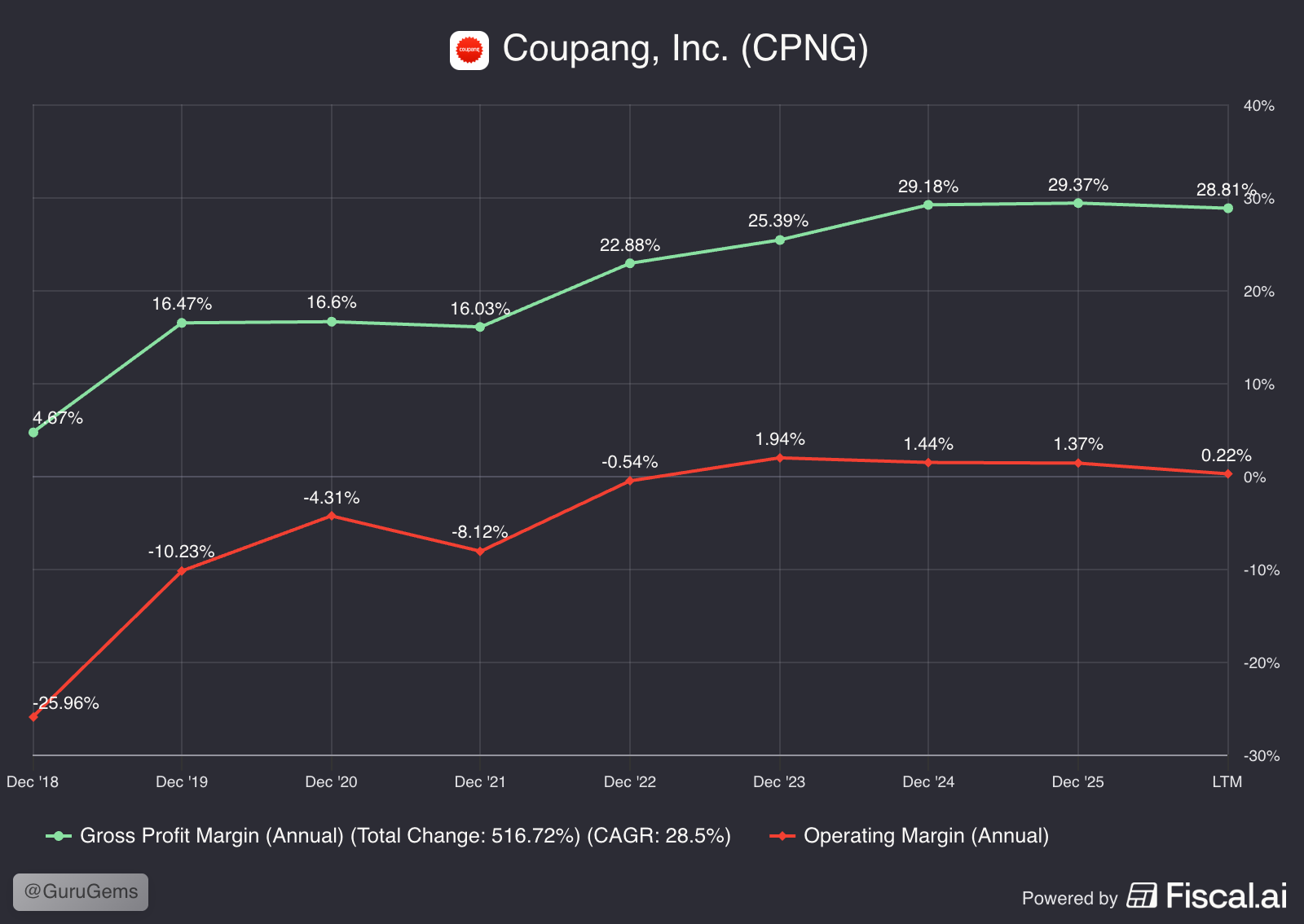

As of 2026, Coupang’s gross margin sits at just below 30% and has nearly doubled over the past 5 years. This shows that Coupang’s warehouse automation, AI demand forecasting, and scale are working to lower product costs.

However, Coupang’s operating margin is razor-thin, hovering near 0-1%.

Management is choosing to reinvest its gross profits immediately into capturing new markets

Building a massive delivery network (logistics moat)

High expansion costs into new markets (Taiwan, luxury platform Farfetch)

Heavy spending on its WOW membership ecosystem to maintain its dominant market share,

The recent data breach and massive $400m fine will also have an impact.

The investment thesis is that once Taiwan and other growth engines scale up and one-time legal issues fade, Coupang’s high gross profits should theoretically trickle down into a much stronger operating margin.

Is it ‘cheap’?

This is the part where I have done the least research on and therefore is a bit ‘too hard’ for me to assess right now.

When looking at some traditional metrics like EV/EBIT or P/FCF, Coupang may look very expensive.

However, Miller Value Partners writes that Coupang shares “trade at a forward (FY27) EV/Sales multiple of 0.6x, a ~71% discount to the stock’s peer group (AMZN, MELI, BABA, ETSY, EBAY, SE, Naver) average multiple”

Final decision

📌 Adding CPNG to the Guru Gems watchlist

Coupang ticks the Ecosystem and Optionality boxes, and the fact that it’s down nearly 40% over the past year means there is probably a lot of negative expectations already priced in.

But unlike a company like S&P Global, where the quality already converts to fat margins, Coupang’s profitability is still unproven.

So for now it goes on the Guru Gems watchlist rather than the portfolio. I do plan to study this business in more detail and will especially be looking for investment theses from other Gurus holding the stock (Oakmark, Chase Coleman).

That’s it for this week’s edition!

Thank you for reading and following along.

Until next week!